A nonprofit corporation is one that is organized for charitable or benevolent purposes. These corporations include certain hospitals, universities, churches, and other religious organizations. A nonprofit entity does not have to be a nonprofit corporation, however. Nonprofit corporations do not have shareholders, but have members or a perpetual board of directors or board of trustees.

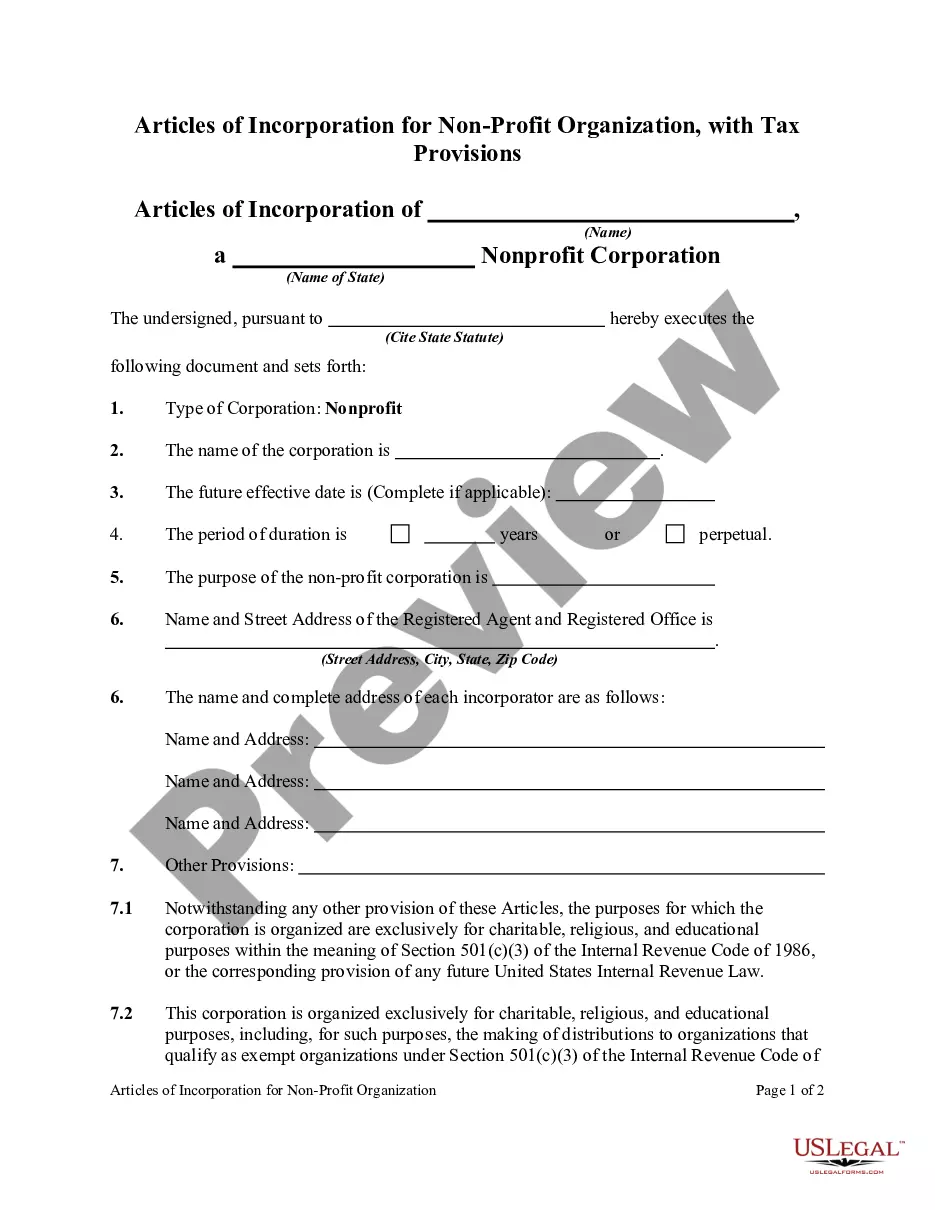

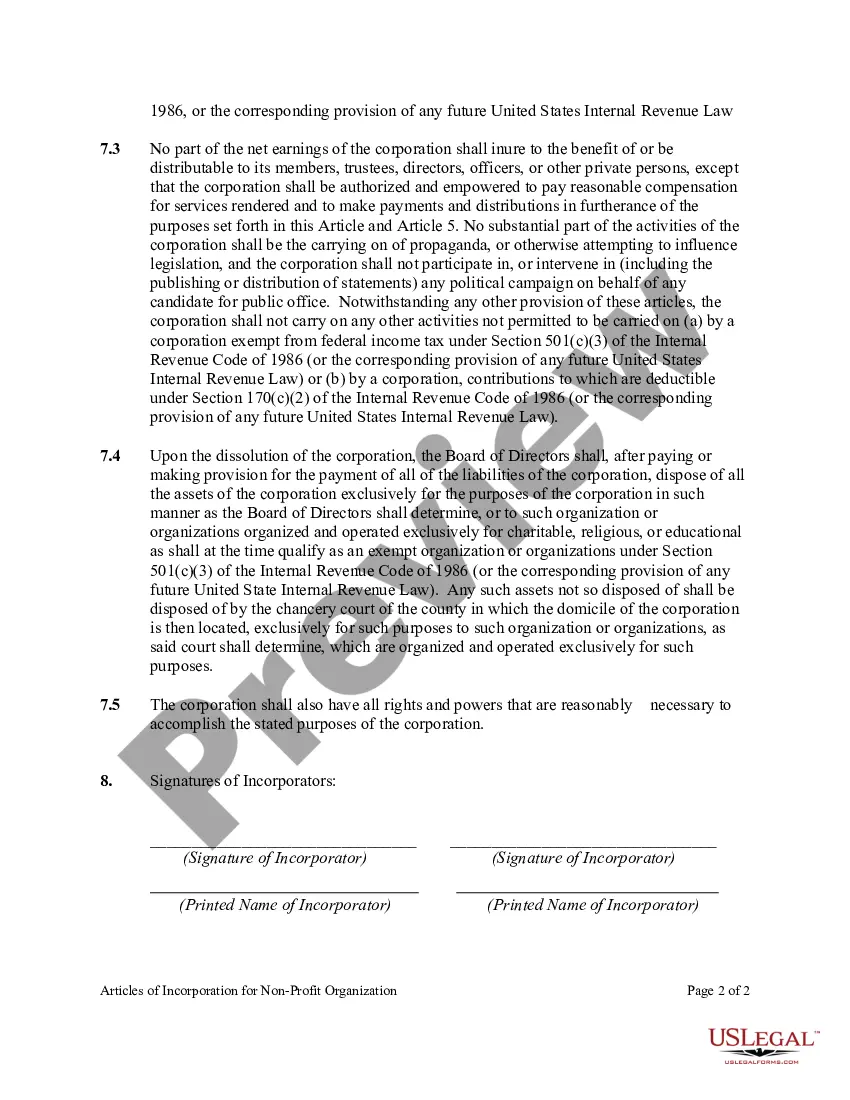

Connecticut Articles of Incorporation for Non-Profit Organization, with Tax Provisions Keywords: Connecticut, Articles of Incorporation, non-profit organization, tax provisions, types Introduction: In Connecticut, non-profit organizations looking to establish themselves legally must file Articles of Incorporation with the Secretary of the State. The Articles of Incorporation outline important details about the organization, including its purpose, structure, and tax provisions. This detailed description provides an overview of the Connecticut Articles of Incorporation for Non-Profit Organization, with a focus on tax provisions and potential variations. 1. Purpose: The Articles of Incorporation define the primary purpose of the non-profit organization. It should clearly state the mission, objectives, and activities the organization aims to undertake for the betterment of society. 2. Name and Registered Agent: The document requires the organization to provide its unique name, ensuring it does not conflict with any existing entities in Connecticut. An organization must also designate a registered agent, an individual or entity responsible for receiving important legal documents on behalf of the non-profit. 3. Membership: Some non-profit organizations have a formal membership structure, where individuals or organizations become members by fulfilling certain criteria. The Articles of Incorporation can outline the rights, responsibilities, and privileges of these members if applicable. 4. Board of Directors: The Articles of Incorporation specify the initial board of directors or trustees responsible for the organization's governance. It should include the minimum and maximum number of board members, their qualifications, terms, and procedures for their election or removal. 5. Tax Provisions: Connecticut recognizes tax-exempt non-profit organizations under the Internal Revenue Code section 501(c)(3). Non-profit organizations seeking this status will have specific tax provisions included in their Articles of Incorporation. These provisions typically include the organization's commitment to operate exclusively for charitable, educational, religious, scientific, or other exempt purposes. 6. Dissolution Clause: The Articles of Incorporation must outline what happens to the organization's assets if it decides to dissolve. Connecticut's law mandates that these assets must be distributed in a manner consistent with the non-profit organization's tax-exempt status. Types of Connecticut Articles of Incorporation for Non-Profit Organization with Tax Provisions: 1. Standard Articles of Incorporation: These are the most common type of Articles of Incorporation filed by non-profit organizations. They include detailed provisions related to the organization's purpose, structure, tax provisions, and dissolution instructions. 2. Articles of Incorporation with Specific Tax Provisions: Certain non-profit organizations, such as churches or religious institutions, have unique tax provisions based on their exempt purposes and activities. These Articles of Incorporation may contain additional clauses specific to the organization's religious or spiritual nature. 3. Restated Articles of Incorporation: If changes need to be made to an existing non-profit organization's Articles of Incorporation, a restated version can be filed. Restated Articles consolidate all previous amendments and modifications into a single document, ensuring clarity and coherence. Conclusion: Filing Connecticut Articles of Incorporation for a non-profit organization with tax provisions is a crucial step to ensure legal recognition and tax-exempt status. The document serves to define the purpose, structure, tax provisions, and potential dissolution instructions of the organization. By complying with the relevant regulations and utilizing the appropriate type of Articles of Incorporation, non-profit organizations can establish a solid legal foundation in Connecticut.Connecticut Articles of Incorporation for Non-Profit Organization, with Tax Provisions Keywords: Connecticut, Articles of Incorporation, non-profit organization, tax provisions, types Introduction: In Connecticut, non-profit organizations looking to establish themselves legally must file Articles of Incorporation with the Secretary of the State. The Articles of Incorporation outline important details about the organization, including its purpose, structure, and tax provisions. This detailed description provides an overview of the Connecticut Articles of Incorporation for Non-Profit Organization, with a focus on tax provisions and potential variations. 1. Purpose: The Articles of Incorporation define the primary purpose of the non-profit organization. It should clearly state the mission, objectives, and activities the organization aims to undertake for the betterment of society. 2. Name and Registered Agent: The document requires the organization to provide its unique name, ensuring it does not conflict with any existing entities in Connecticut. An organization must also designate a registered agent, an individual or entity responsible for receiving important legal documents on behalf of the non-profit. 3. Membership: Some non-profit organizations have a formal membership structure, where individuals or organizations become members by fulfilling certain criteria. The Articles of Incorporation can outline the rights, responsibilities, and privileges of these members if applicable. 4. Board of Directors: The Articles of Incorporation specify the initial board of directors or trustees responsible for the organization's governance. It should include the minimum and maximum number of board members, their qualifications, terms, and procedures for their election or removal. 5. Tax Provisions: Connecticut recognizes tax-exempt non-profit organizations under the Internal Revenue Code section 501(c)(3). Non-profit organizations seeking this status will have specific tax provisions included in their Articles of Incorporation. These provisions typically include the organization's commitment to operate exclusively for charitable, educational, religious, scientific, or other exempt purposes. 6. Dissolution Clause: The Articles of Incorporation must outline what happens to the organization's assets if it decides to dissolve. Connecticut's law mandates that these assets must be distributed in a manner consistent with the non-profit organization's tax-exempt status. Types of Connecticut Articles of Incorporation for Non-Profit Organization with Tax Provisions: 1. Standard Articles of Incorporation: These are the most common type of Articles of Incorporation filed by non-profit organizations. They include detailed provisions related to the organization's purpose, structure, tax provisions, and dissolution instructions. 2. Articles of Incorporation with Specific Tax Provisions: Certain non-profit organizations, such as churches or religious institutions, have unique tax provisions based on their exempt purposes and activities. These Articles of Incorporation may contain additional clauses specific to the organization's religious or spiritual nature. 3. Restated Articles of Incorporation: If changes need to be made to an existing non-profit organization's Articles of Incorporation, a restated version can be filed. Restated Articles consolidate all previous amendments and modifications into a single document, ensuring clarity and coherence. Conclusion: Filing Connecticut Articles of Incorporation for a non-profit organization with tax provisions is a crucial step to ensure legal recognition and tax-exempt status. The document serves to define the purpose, structure, tax provisions, and potential dissolution instructions of the organization. By complying with the relevant regulations and utilizing the appropriate type of Articles of Incorporation, non-profit organizations can establish a solid legal foundation in Connecticut.