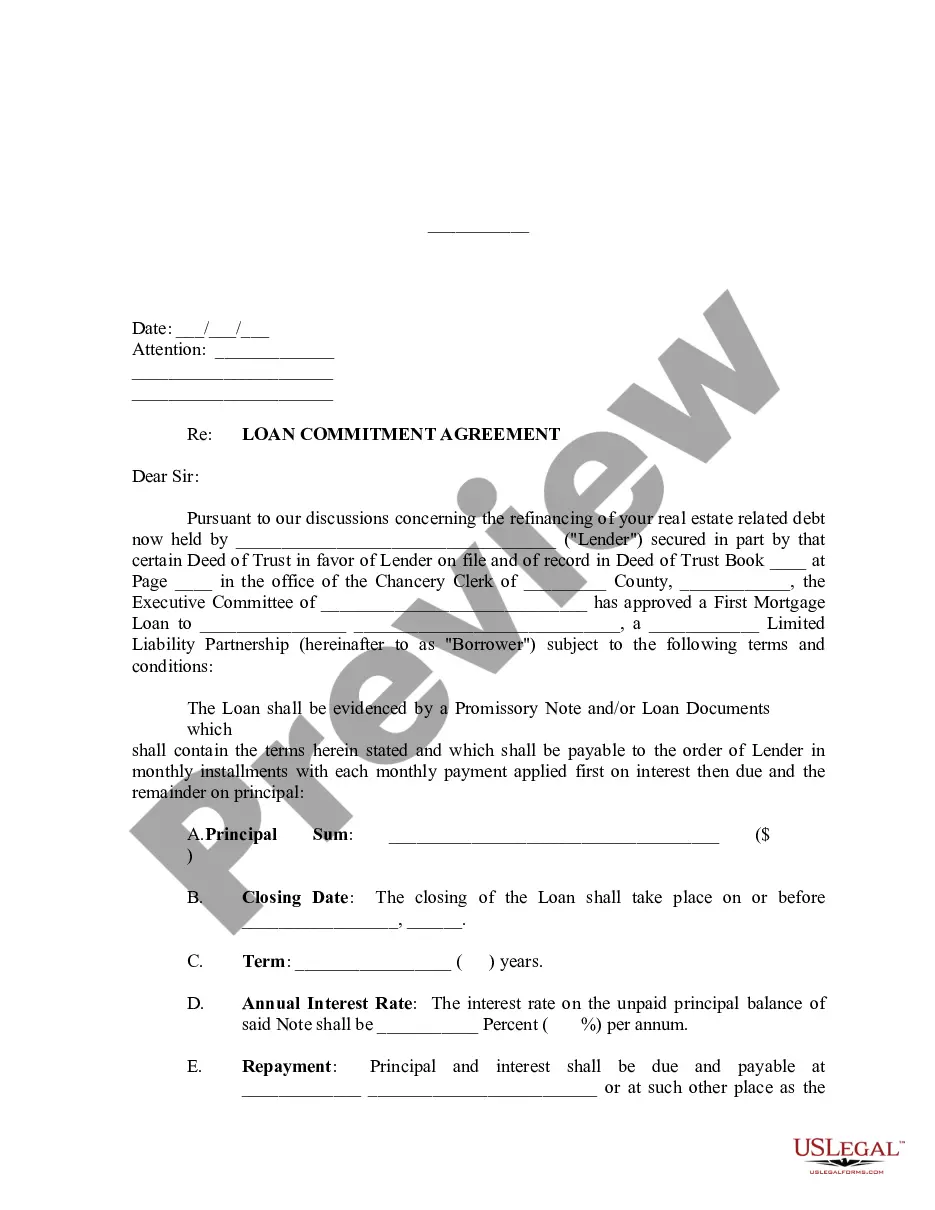

Connecticut Loan Commitment Agreement

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Loan Commitment Agreement?

Are you currently in the placement in which you need paperwork for sometimes organization or personal functions nearly every day? There are tons of legal file layouts available on the Internet, but getting kinds you can rely is not effortless. US Legal Forms provides 1000s of form layouts, such as the Connecticut Loan Commitment Agreement, which can be composed to meet federal and state demands.

If you are currently informed about US Legal Forms internet site and have a free account, basically log in. Afterward, you are able to acquire the Connecticut Loan Commitment Agreement format.

Should you not offer an bank account and need to begin to use US Legal Forms, follow these steps:

- Find the form you need and make sure it is for that appropriate town/area.

- Make use of the Preview button to examine the form.

- See the outline to actually have selected the correct form.

- When the form is not what you`re looking for, make use of the Lookup industry to find the form that meets your requirements and demands.

- When you find the appropriate form, just click Purchase now.

- Pick the costs strategy you need, fill in the desired information and facts to make your bank account, and purchase the order with your PayPal or Visa or Mastercard.

- Select a convenient file formatting and acquire your copy.

Find every one of the file layouts you may have bought in the My Forms menu. You can aquire a more copy of Connecticut Loan Commitment Agreement whenever, if needed. Just click on the essential form to acquire or print out the file format.

Use US Legal Forms, by far the most comprehensive variety of legal forms, to save lots of time and avoid errors. The services provides professionally produced legal file layouts which can be used for an array of functions. Create a free account on US Legal Forms and initiate producing your life easier.

Form popularity

FAQ

We can define a commitment letter as a formal and legally binding document that a lender issues to a loan applicant. The commitment letter indicates that a loan applicant has passed the various underwriting guidelines and that their loan agreement or mortgage note has been approved.

Does A Loan Commitment Letter Mean I'm Approved? After you're preapproved, you'll receive a conditional mortgage commitment letter. That does not mean you're approved for the loan. With this conditional approval, you'll still have steps to take in the mortgage application process.

As mentioned above, mortgage commitment letters have expiration dates specified by the lender, after which your approval and any rate lock you had are rendered void. The length of commitment can vary between lenders, but a mortgage commitment letter typically expires after 30 days.

The must-have details in your loan commitment letter are the lender's and borrower's information, loan type and amount, repayment agreement, and loan expiration.

It's important to note that just because your mortgage company created the commitment letter, doesn't mean you shouldn't be able to still back out. Nothing is final for the borrower until the loan is funded and all the closing documents are signed.

A mortgage commitment letter includes the amount being borrowed, the interest rate, and the length of the loan. There will also be conditions attached, such as the requirement to carry homeowner's insurance. A lender can still deny a loan at closing if these conditions have not been met.

The qualification of the loan is dependent on the borrower's income and credit history. A loan commitment is when a financial institution makes an agreement to lend a certain amount of cash to an individual or business.

A loan commitment is an agreement by a commercial bank or other financial institution to lend a business or individual a specified sum of money. A loan commitment is useful for consumers looking to buy a home or a business planning to make a major purchase.