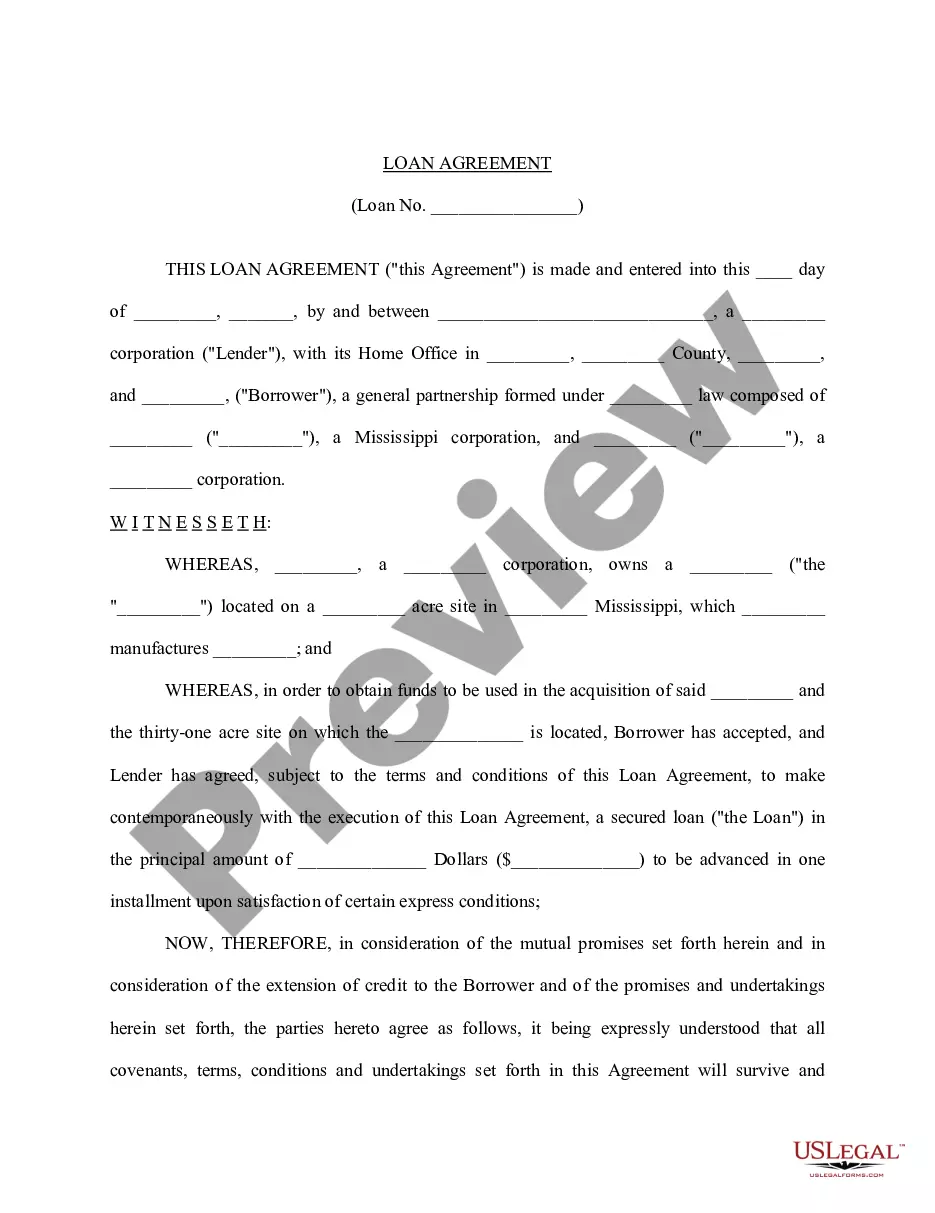

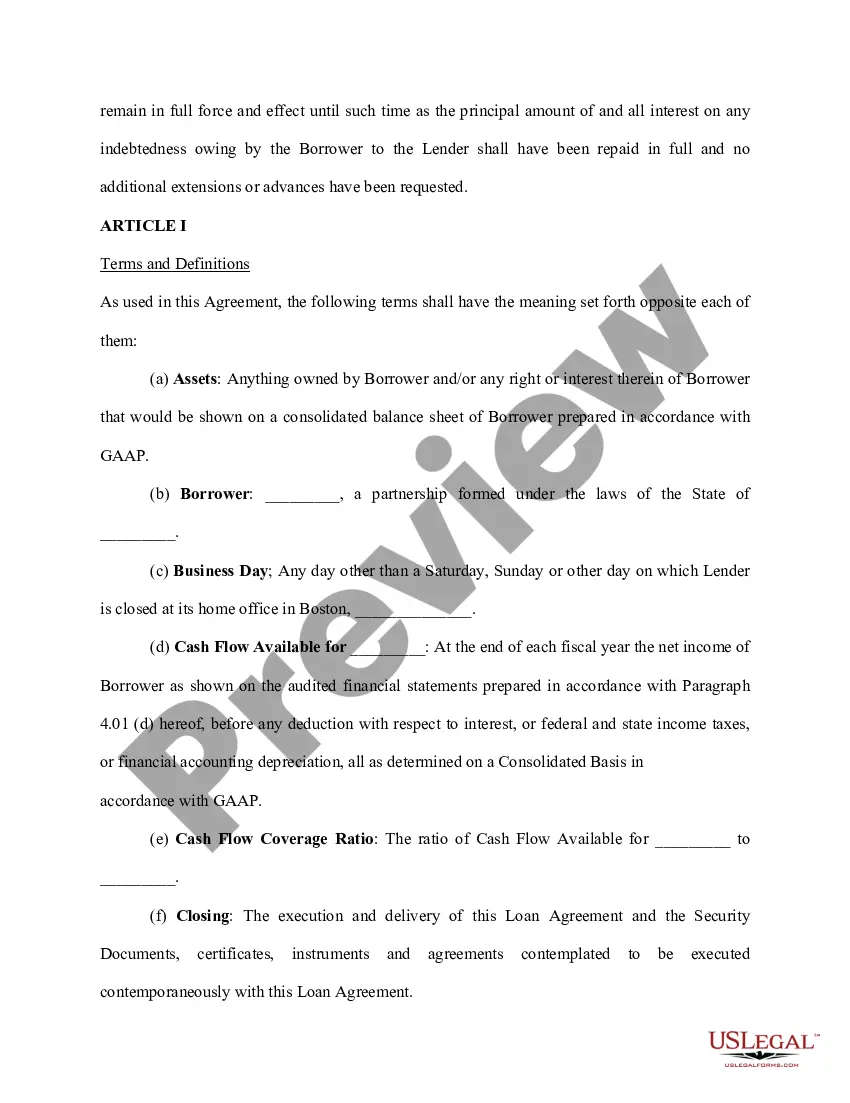

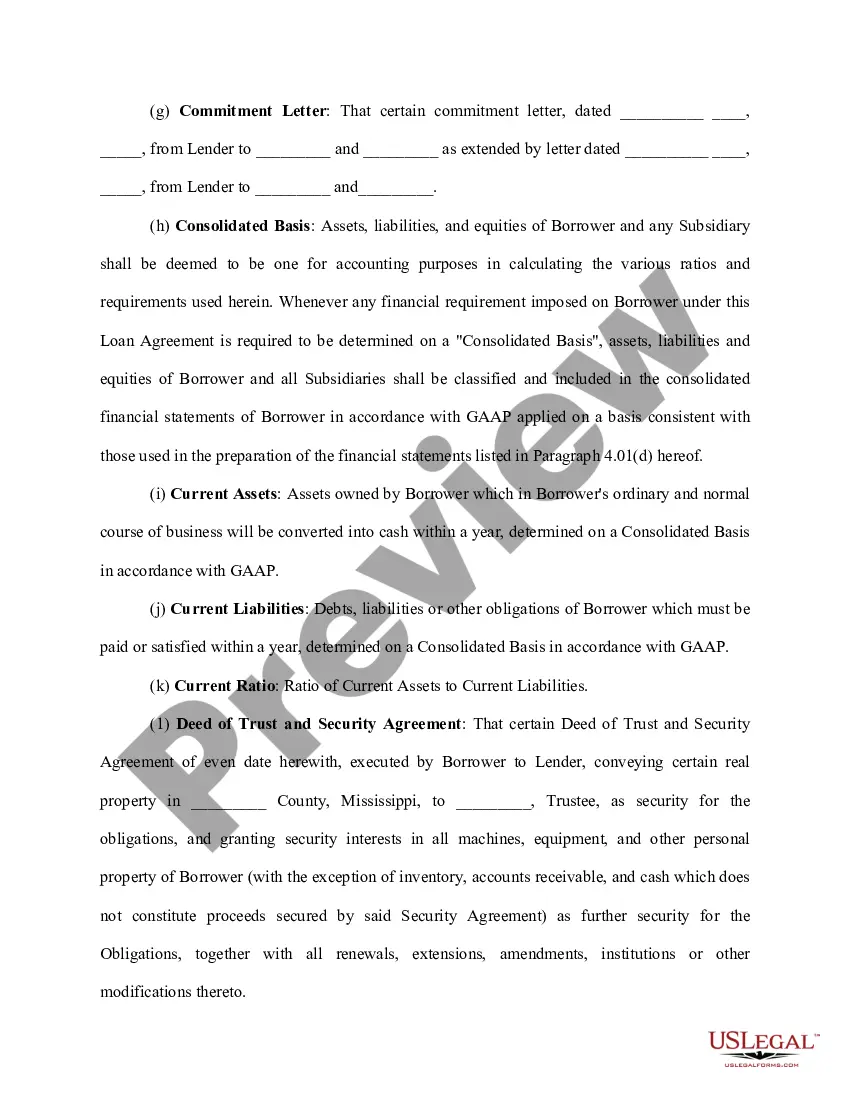

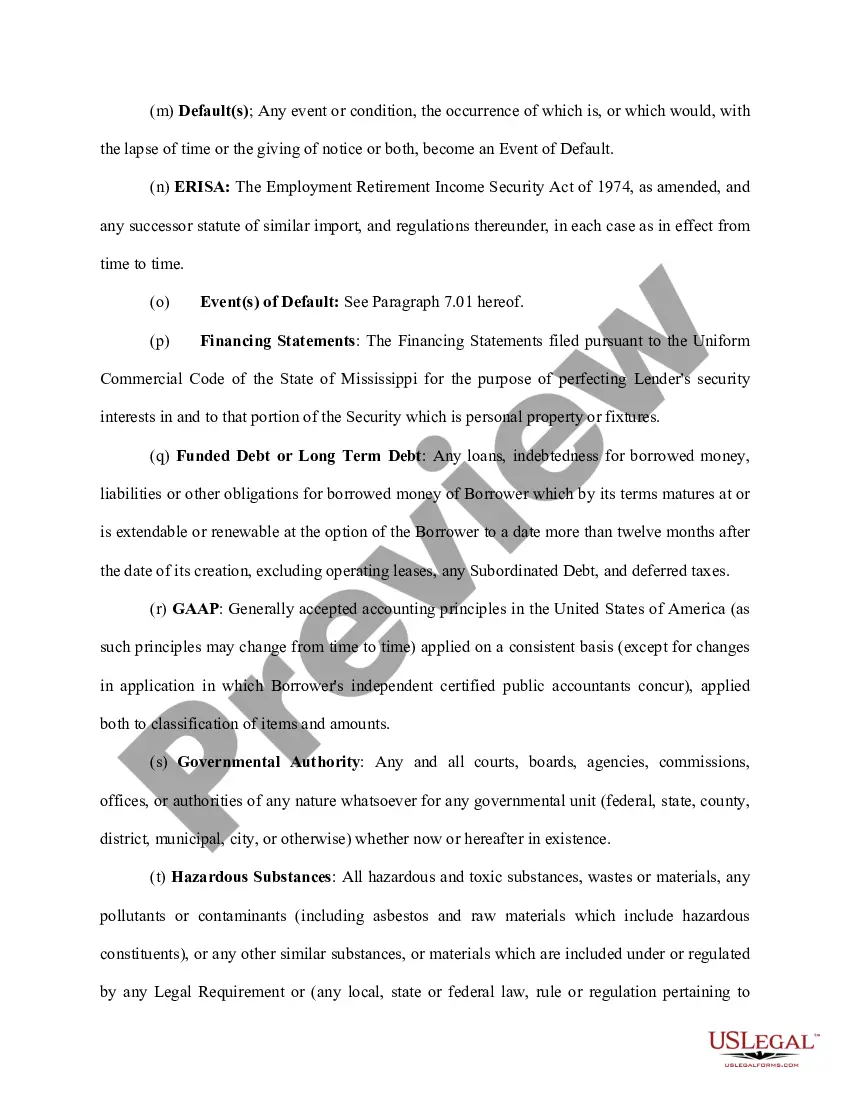

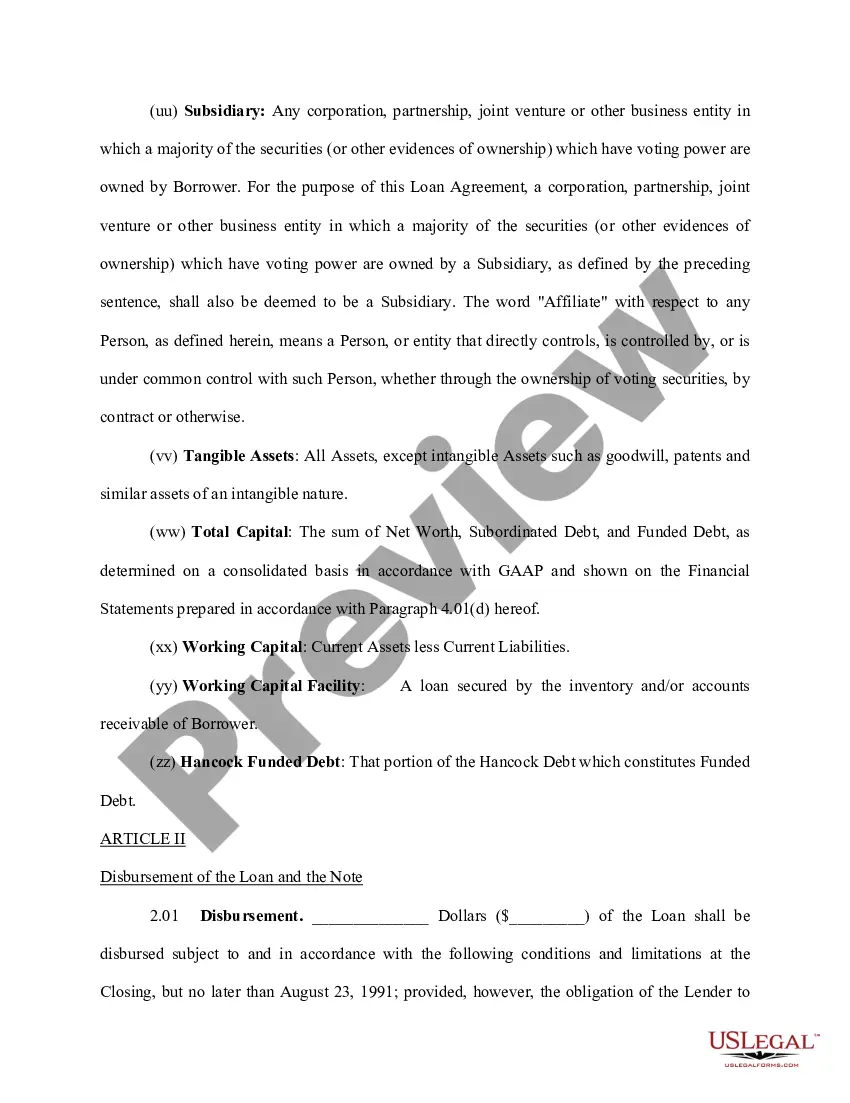

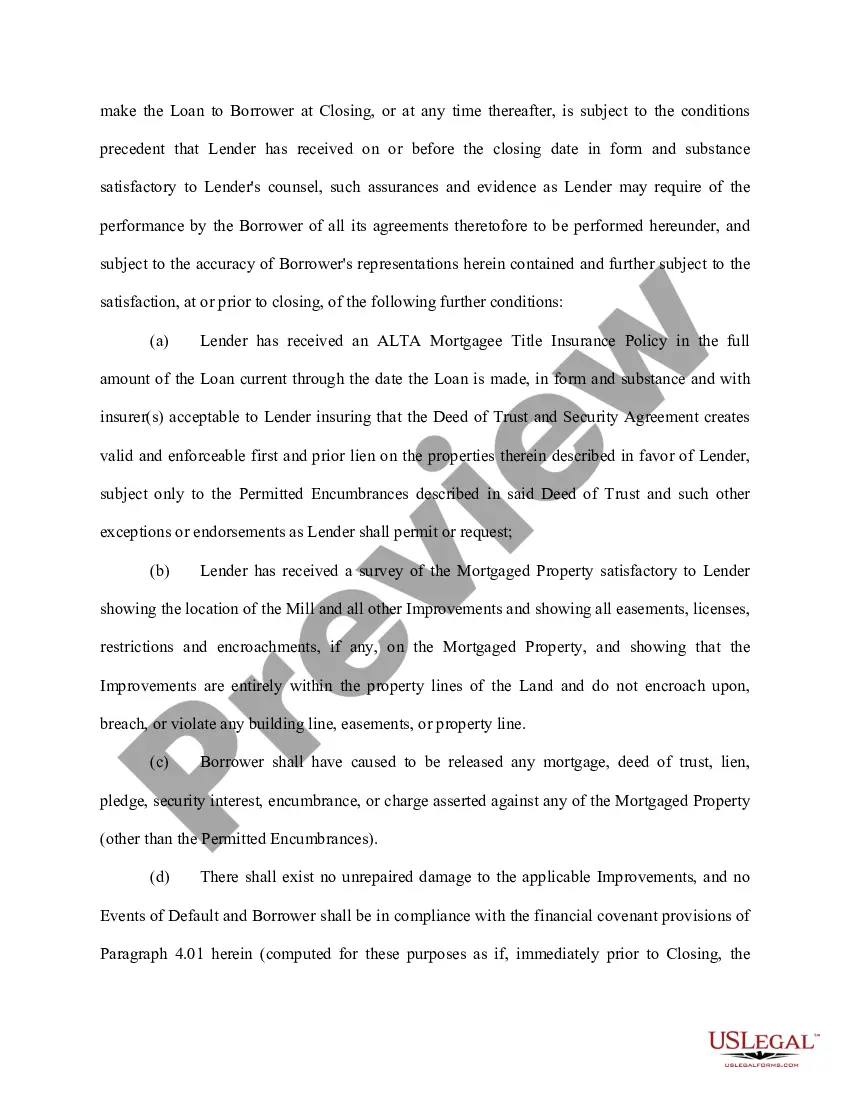

Connecticut Loan Agreement for Family Member is a legally binding contract between two parties, where one family member agrees to loan a specific amount of money to another family member. This document ensures that the loan terms and conditions are clearly defined, protecting the interests of both parties involved. In Connecticut, there are different types of Loan Agreements for Family Members, each serving a specific purpose and addressing unique circumstances. These variations may include: 1. Personal Loan Agreement: This agreement is used when a family member lends money to another family member for personal reasons, such as medical expenses, education, or to consolidate debts. It outlines the loan amount, interest rate (if applicable), repayment schedule, and any additional terms or conditions agreed upon. 2. Business Loan Agreement: If a family member requires financial assistance for business purposes, a Business Loan Agreement is used. This type of agreement specifies the loan amount, purpose, repayment terms, interest (if applicable), and any other relevant details pertaining to the loan and its use for business-related activities. 3. Mortgage Loan Agreement: In cases where a family member loans money for real estate purposes, a Mortgage Loan Agreement is utilized. This type of agreement includes details about the loan amount, interest rate, repayment schedule, collateral (the property to be mortgaged), and other terms specific to the mortgage loan process. 4. Vehicle Loan Agreement: When a family member lends money to another family member for purchasing a vehicle, a Vehicle Loan Agreement is employed. This agreement outlines the loan amount, repayment terms, interest (if applicable), vehicle details, and any other relevant conditions related to the loan and its use for buying a car or any other vehicle. Regardless of the type of Loan Agreement for Family Member used in Connecticut, it is essential to include certain crucial elements. These elements include the names and contact information of both parties involved, the loan amount, interest rate (if applicable), repayment terms, any additional fees or charges, the consequences of default on payments, and provisions for dispute resolution or arbitration if necessary. It is crucial to consult with a legal professional or attorney experienced in Connecticut law to ensure that the Loan Agreement for Family Member complies with all applicable regulations and protects the interests of both parties involved.

Connecticut Loan Agreement for Family Member

Description

How to fill out Connecticut Loan Agreement For Family Member?

You are able to invest several hours online looking for the legitimate papers template which fits the federal and state specifications you require. US Legal Forms offers a huge number of legitimate forms that are reviewed by specialists. You can actually down load or produce the Connecticut Loan Agreement for Family Member from your services.

If you already have a US Legal Forms bank account, it is possible to log in and click the Download button. Following that, it is possible to full, modify, produce, or indicator the Connecticut Loan Agreement for Family Member. Each legitimate papers template you get is your own for a long time. To obtain another duplicate associated with a acquired type, check out the My Forms tab and click the corresponding button.

Should you use the US Legal Forms web site the very first time, keep to the straightforward guidelines listed below:

- First, make certain you have chosen the best papers template for that state/area of your choice. Read the type information to ensure you have picked the appropriate type. If available, utilize the Review button to search throughout the papers template as well.

- If you wish to locate another version from the type, utilize the Search discipline to discover the template that meets your needs and specifications.

- After you have identified the template you desire, just click Buy now to carry on.

- Choose the pricing plan you desire, enter your credentials, and sign up for your account on US Legal Forms.

- Comprehensive the purchase. You may use your credit card or PayPal bank account to purchase the legitimate type.

- Choose the structure from the papers and down load it to the product.

- Make changes to the papers if possible. You are able to full, modify and indicator and produce Connecticut Loan Agreement for Family Member.

Download and produce a huge number of papers layouts using the US Legal Forms Internet site, which offers the largest collection of legitimate forms. Use professional and condition-particular layouts to handle your organization or specific needs.