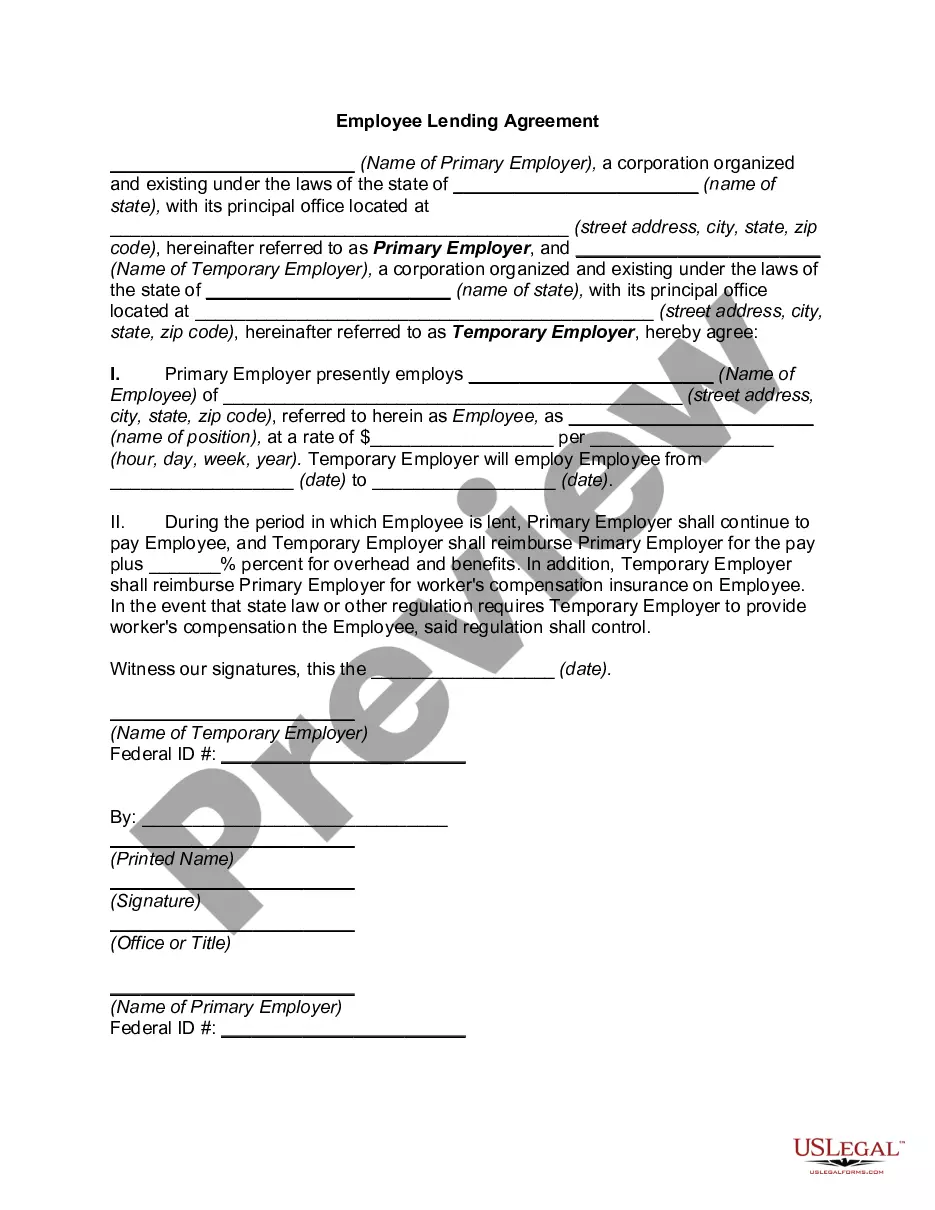

Connecticut Loan Agreement for Employees

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Loan Agreement For Employees?

Finding the right legal papers template could be a battle. Obviously, there are a lot of web templates accessible on the Internet, but how do you get the legal type you require? Utilize the US Legal Forms internet site. The support delivers a huge number of web templates, such as the Connecticut Loan Agreement for Employees, which can be used for business and private requires. Every one of the varieties are checked by specialists and satisfy state and federal requirements.

Should you be presently listed, log in for your accounts and then click the Obtain option to get the Connecticut Loan Agreement for Employees. Make use of accounts to search through the legal varieties you might have acquired in the past. Visit the My Forms tab of your respective accounts and get yet another duplicate of your papers you require.

Should you be a whole new consumer of US Legal Forms, listed below are straightforward recommendations that you should comply with:

- Very first, make certain you have selected the proper type for the metropolis/area. You are able to examine the shape making use of the Review option and read the shape explanation to ensure it is the best for you.

- When the type will not satisfy your preferences, use the Seach area to discover the proper type.

- Once you are sure that the shape is proper, click on the Acquire now option to get the type.

- Select the costs prepare you desire and enter the needed information. Design your accounts and pay for the transaction utilizing your PayPal accounts or credit card.

- Pick the data file format and obtain the legal papers template for your device.

- Comprehensive, revise and produce and indicator the obtained Connecticut Loan Agreement for Employees.

US Legal Forms is the most significant library of legal varieties in which you can see different papers web templates. Utilize the service to obtain professionally-produced documents that comply with state requirements.

Form popularity

FAQ

There are 10 basic provisions that should be in a loan agreement. Identity of the parties. The names of the lender and borrower need to be stated. ... Date of the agreement. ... Interest rate. ... Repayment terms. ... Default provisions. ... Signatures. ... Choice of law. ... Severability.

Here's some of the critical information you should ensure is included in every business loan agreement: Step 1 ? Set an Effective Date. ... Step 2 ? Identify the Parties. ... Step 3 ? Include the Loan Amount. ... Step 4 ? Create a Repayment Schedule. ... Step 5 ? Define Security Interests or Collateral. ... Step 6 ? Set an Interest Rate.

A loan agreement should be structured to include information about the borrower and the lender, the loan amount, and repayment terms, including interest charges and a timeline for repaying the loan. It should also spell out penalties for late payments or default and should be clear about expectations between parties.

However, the do-it-yourself approach is perfectly acceptable and just as legally enforceable. Once you have both agreed on the terms, you may want to have the personal loan contract notarized or ask a third party to act as a witness during the signing.

Here's some of the critical information you should ensure is included in every business loan agreement: Step 1 ? Set an Effective Date. ... Step 2 ? Identify the Parties. ... Step 3 ? Include the Loan Amount. ... Step 4 ? Create a Repayment Schedule. ... Step 5 ? Define Security Interests or Collateral. ... Step 6 ? Set an Interest Rate.

What should be in a personal loan contract? Names and addresses of the lender and the borrower. Information about the loan co-borrower or cosigner, if it's a joint personal loan. Loan amount and the method for disbursement (lump sum, installments, etc.) Date the loan was provided. Expected repayment date.

Include key terms of the loan, such as the lender and borrower's contact information, the reason for the loan, what is being loaned, the interest rate, the repayment plan, what would happen if the borrower can't make the payments, and more. The amount of the loan, also known as the principal amount.

What a personal loan agreement should include Legal names and address of both parties. Names and address of the loan cosigner (if applicable). Amount to be borrowed. Date the loan is to be provided. Repayment date. Interest rate to be charged (if applicable). Annual percentage rate (if applicable).