Connecticut Loan Agreement for Friends

Description

How to fill out Loan Agreement For Friends?

You are able to spend hours on-line attempting to find the lawful file design that meets the federal and state requirements you want. US Legal Forms offers thousands of lawful kinds which can be reviewed by professionals. It is simple to obtain or print out the Connecticut Loan Agreement for Friends from our service.

If you already possess a US Legal Forms bank account, you can log in and click the Download switch. Following that, you can complete, change, print out, or sign the Connecticut Loan Agreement for Friends. Every lawful file design you purchase is the one you have forever. To acquire yet another version for any purchased develop, visit the My Forms tab and click the related switch.

If you are using the US Legal Forms website the first time, keep to the easy directions listed below:

- Initially, make certain you have chosen the proper file design for the county/metropolis of your choosing. See the develop description to ensure you have selected the appropriate develop. If offered, use the Preview switch to check throughout the file design at the same time.

- If you would like get yet another variation of the develop, use the Search industry to obtain the design that meets your needs and requirements.

- Upon having located the design you want, simply click Purchase now to continue.

- Choose the costs plan you want, key in your qualifications, and register for a merchant account on US Legal Forms.

- Total the deal. You should use your Visa or Mastercard or PayPal bank account to purchase the lawful develop.

- Choose the structure of the file and obtain it in your system.

- Make modifications in your file if necessary. You are able to complete, change and sign and print out Connecticut Loan Agreement for Friends.

Download and print out thousands of file templates while using US Legal Forms web site, that provides the most important selection of lawful kinds. Use specialist and express-certain templates to take on your business or specific demands.

Form popularity

FAQ

A loan is a legal contract, and as such, it has potential tax consequences for both the borrower and the lender. Borrowers have to repay the debt as agreed or claim the canceled debt as income. Lenders who charge interest on a loan have to pay taxes on any interest earned from the borrower.

Typically, it is a good idea to create a contract for money loaned, money owed, or any personal property you lend. Other ways to show evidence can include emails, texts, money transfer receipts, bank account transfer history, etc.

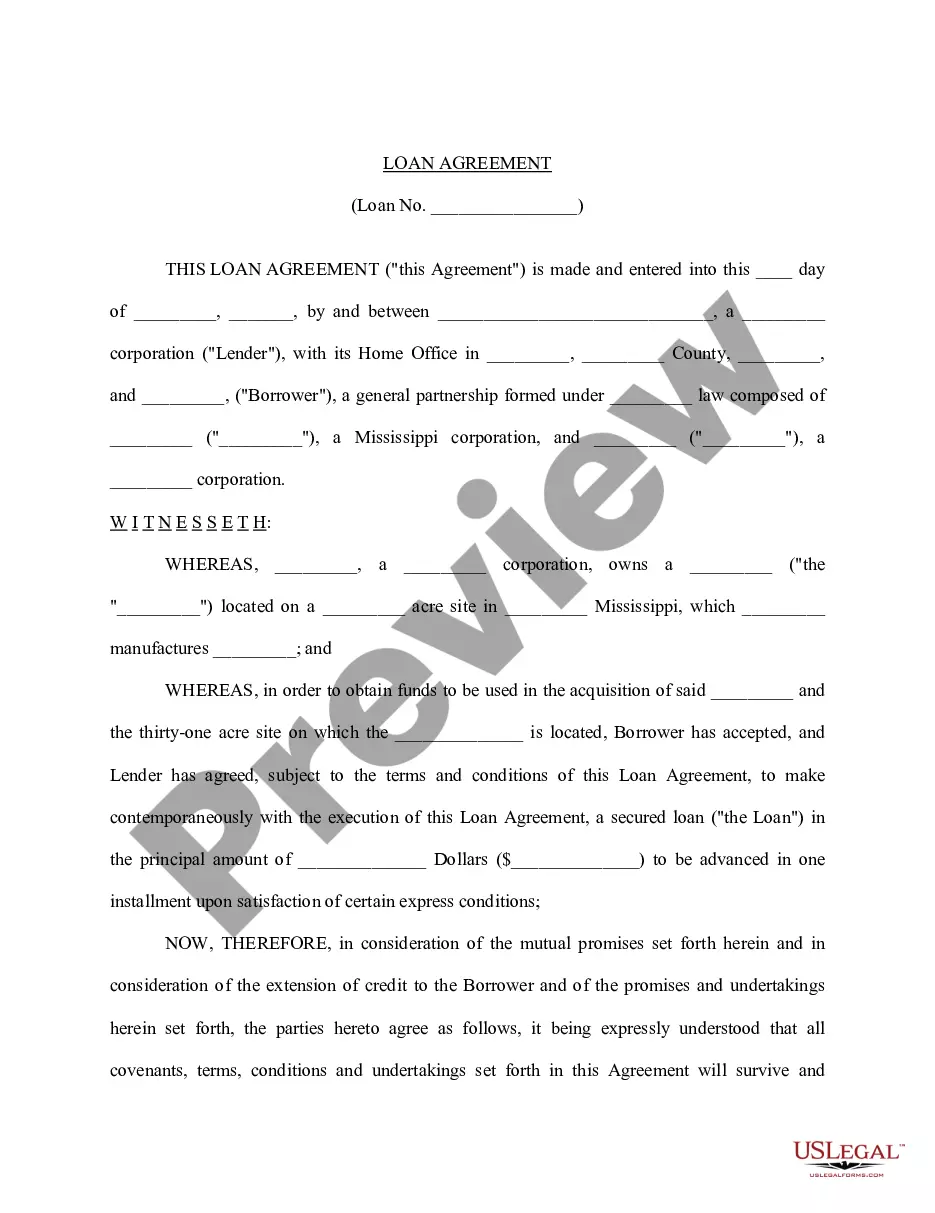

A loan agreement is any written document that memorializes the lending of money. Loan agreements can take several forms. The most basic loan agreement is commonly called an "IOU." These are typically used between friends or relatives for small amounts of money, and simply state the dollar amount that is owed.

Promissory Notes document financial transactions between two parties. Unlike an IOU that only records a loan amount, a Promissory Note details the consequences of failing to repay the loan. After finalizing the terms and conditions of a loan, the lender will issue a Promissory Note.

You can lend money at interest, provided that the interest rate falls within the appropriate legal guidelines. Most states have usury laws that limit the maximum amount of interest that a lender can charge. In addition, you should also consider the Applicable Funds Rate prescribed by the Internal Revenue Service (IRS).

What should be in a personal loan contract? Names and addresses of the lender and the borrower. Information about the loan co-borrower or cosigner, if it's a joint personal loan. Loan amount and the method for disbursement (lump sum, installments, etc.) Date the loan was provided. Expected repayment date.

It makes sense to write-up a formal loan agreement ? even for very small amounts. If you have something down in writing at the start that is signed, it can help with disputes later on. A written loan agreement can benefit both parties because you can use it as protection if one of you breaches the terms.

Common items in personal loan agreements. The name, address, and contact information of the borrower. The name, address, and contact information of the lender. A plan for loan payment, such as a monthly payment plan with start dates and due dates. The maturity date or the date that the final payment is due on the loan.