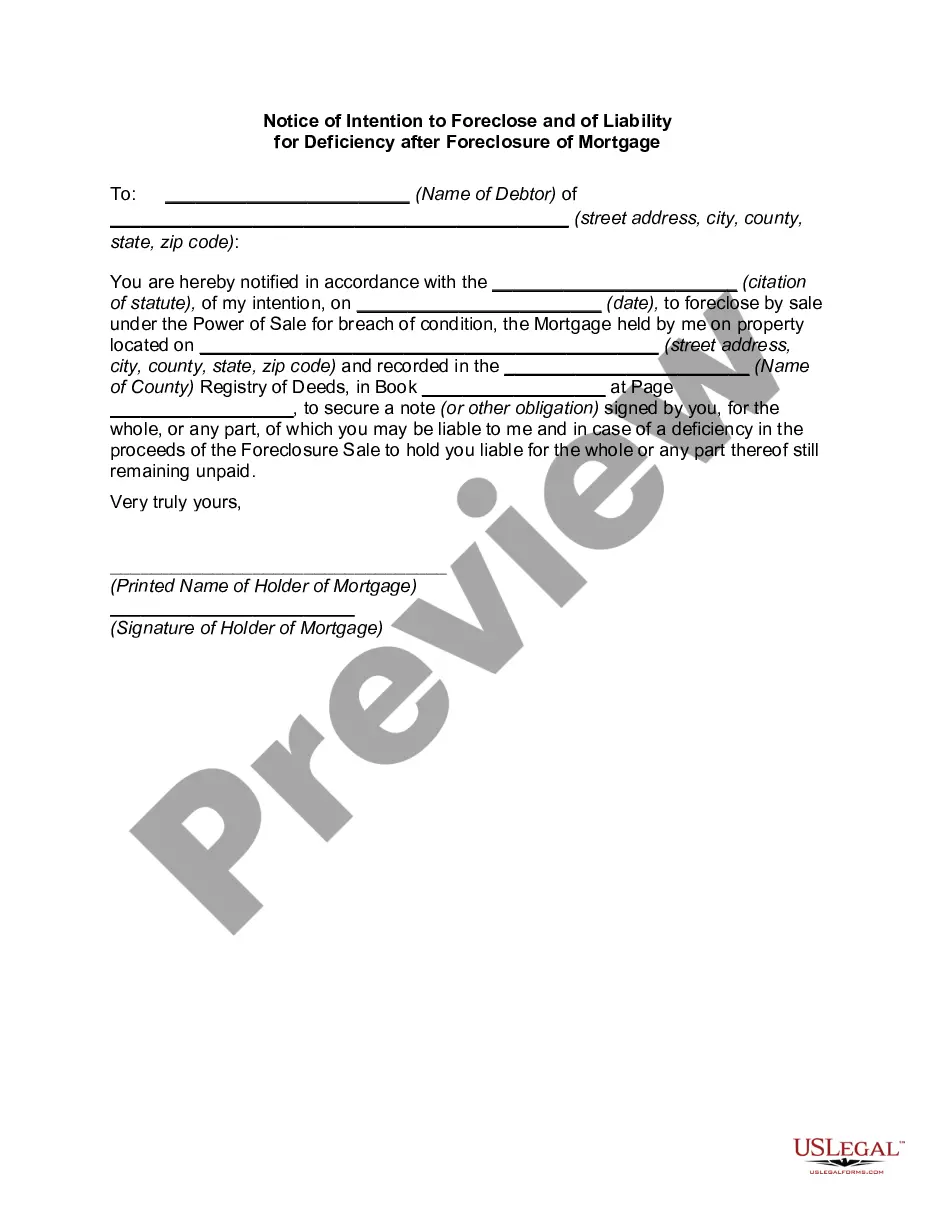

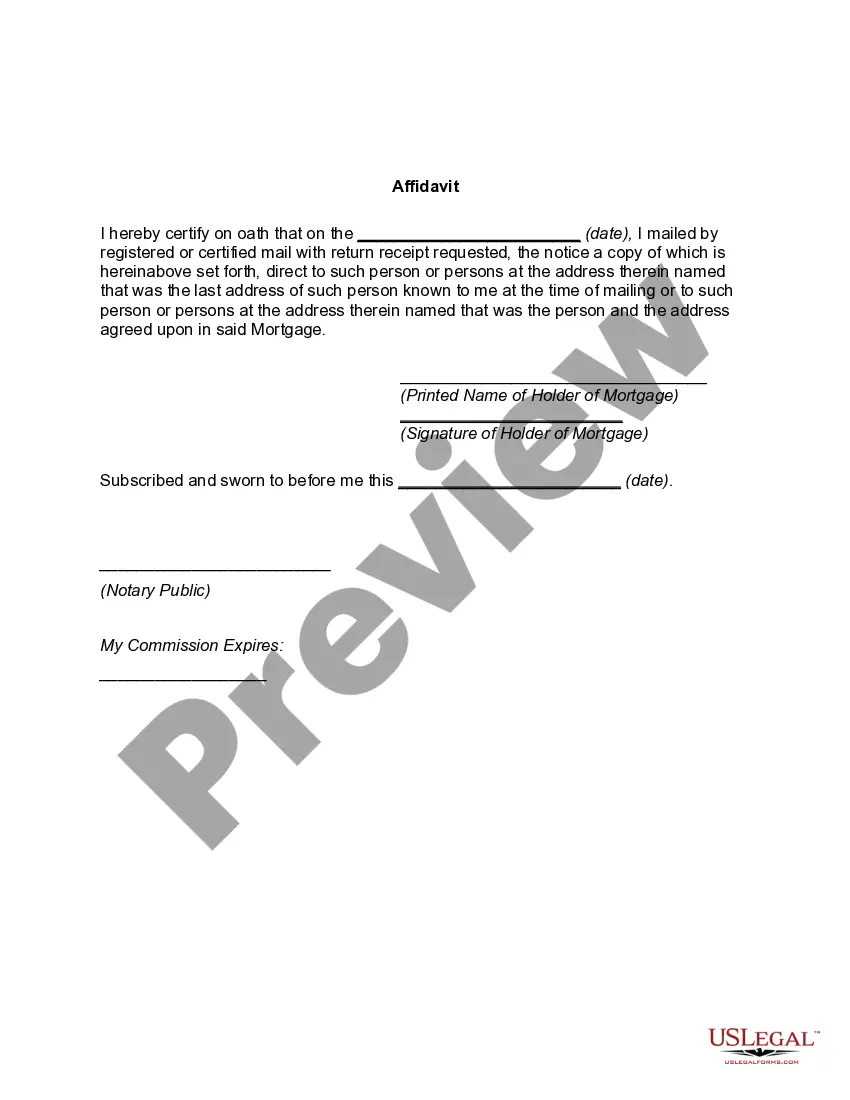

Connecticut Notice of Intention to Foreclose and Liability for Deficiency after Foreclosure of Mortgage In the state of Connecticut, a Notice of Intention to Foreclose and Liability for Deficiency after Foreclosure of Mortgage is a legal document that serves to inform borrowers of the lender's intent to initiate foreclosure proceedings on their property. This notice is a critical step in the foreclosure process and outlines the borrower's rights and potential legal liabilities following the foreclosure. The Notice of Intention to Foreclose is typically issued by the lending institution when the borrower fails to make timely mortgage payments for a significant duration, resulting in default. This notice is sent via certified mail and provides the borrower with a specified period to take necessary actions to prevent the foreclosure. The main purpose of the notice is to inform the borrower of the impending foreclosure, give them an opportunity to cure the default or work out a resolution with the lender, and inform them about potential consequences and liabilities if the foreclosure proceeds. Key topics addressed within the Notice of Intention to Foreclose include: 1. Foreclosure Intent: The notice explicitly states the lender's intent to foreclose on the property due to the borrower's default on mortgage payments. 2. Cure Period: It identifies a specific period (usually between 30 and 60 days) during which the borrower can remedy the default by paying the overdue amounts, including any associated fees and interest. 3. Notice of Liability for Deficiency: In Connecticut, if the foreclosure sale does not generate enough funds to cover the outstanding loan balance, the borrower may be liable for the deficiency — the difference between the outstanding balance and the sale proceeds. This notice alerts the borrower to the potential liability they may face after the foreclosure process, emphasizing the importance of taking timely action. 4. Right to Seek Legal Advice: The notice encourages the borrower to seek legal counsel to fully understand their rights, responsibilities, and potential options to mitigate the consequences of foreclosure. Different types of Connecticut Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage may exist based on variations in individual lender's policies or specific circumstances of the loan agreement. However, the general purpose and content outlined above are typically included in all notices. It is crucial for borrowers to carefully review the Notice of Intention to Foreclose and Liability for Deficiency after Foreclosure of Mortgage upon receipt. If they fail to take timely action or neglect seeking legal advice, they may face potentially severe financial consequences, including a foreclosure sale and the subsequent liability for any deficiency. Disclaimer: This content provides a general overview of a Connecticut Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage. It is not intended as legal advice. Borrowers should consult with legal professionals for guidance specific to their situation.

Connecticut Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage

Description

How to fill out Connecticut Notice Of Intention To Foreclose And Of Liability For Deficiency After Foreclosure Of Mortgage?

Discovering the right authorized papers format can be quite a have a problem. Obviously, there are a variety of templates available on the Internet, but how can you obtain the authorized kind you want? Take advantage of the US Legal Forms website. The support provides a huge number of templates, for example the Connecticut Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage, which you can use for business and personal requirements. All the kinds are checked by professionals and fulfill state and federal demands.

When you are currently listed, log in for your account and then click the Acquire option to obtain the Connecticut Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage. Utilize your account to look with the authorized kinds you might have bought previously. Visit the My Forms tab of your account and get an additional copy from the papers you want.

When you are a new end user of US Legal Forms, allow me to share straightforward guidelines that you can comply with:

- Initial, make sure you have chosen the right kind for your personal town/area. You are able to examine the shape making use of the Preview option and read the shape information to guarantee it will be the best for you.

- If the kind will not fulfill your needs, use the Seach industry to discover the proper kind.

- When you are certain the shape is suitable, go through the Buy now option to obtain the kind.

- Select the rates program you need and enter the essential details. Build your account and pay for the transaction utilizing your PayPal account or Visa or Mastercard.

- Pick the data file file format and down load the authorized papers format for your system.

- Complete, modify and produce and indication the attained Connecticut Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage.

US Legal Forms is the most significant library of authorized kinds that you can find a variety of papers templates. Take advantage of the company to down load skillfully-produced paperwork that comply with condition demands.

Form popularity

FAQ

If a foreclosure is nonjudicial, the foreclosing lender must file a lawsuit following the foreclosure to get a deficiency judgment. On the other hand, with a judicial foreclosure, most states allow the lender to seek a deficiency judgment as part of the underlying foreclosure lawsuit.

A deed in lieu of foreclosure is a document that transfers the title of a property from the property owner to their lender in exchange for relief from the mortgage debt. Choosing a deed in lieu of foreclosure can be less damaging financially than going through a full foreclosure proceeding.

T/F: When a deed is given in lieu of foreclosure of the mortgage, the mortgagor no longer has an obligation to pay the mortgage note. True.

A deed in lieu means you and your lender reach a mutual understanding that you're no longer able to make your mortgage loan payments. The lender agrees to avoid putting you into foreclosure when you hand the property over amicably. In exchange, the lender releases you from your obligations under the mortgage.

(3) Deed in Lieu of Foreclosure ? The borrower returns the property back to the lender in full satisfaction of the mortgaged outstanding debt balance upon an agreement by the lender.

In return for the lender having the power to sell the property, the Power of Sale clause protects the borrower by stating that when the lender sells the property, the lender may not hold the borrower liable for any cost not covered by the sale unless the lender is able to obtain a deficiency judgment in their favor, ...

Disadvantages of a deed in lieu of foreclosure You will have to surrender your home sooner. You may not pursue alternative mortgage relief options, like a loan modification, that could be a better option. You'll likely lose any equity in the property you might have.

In a strict foreclosure, the court sets the redemption period, which is the time between the judgment and the Law Day. The Law Day can be as soon as 21 days after the court enters a judgment of strict foreclosure, but it's typically between 45 and 90 days after the judgment.