Connecticut Partnership Agreement for Startup

Description

How to fill out Partnership Agreement For Startup?

Selecting the optimal authorized document format may be a struggle. Of course, there are numerous templates accessible online, but how do you acquire the legal form you require.

Utilize the US Legal Forms website. The service offers thousands of templates, including the Connecticut Partnership Agreement for Startup, which you can use for business and personal purposes.

All the forms are reviewed by experts and comply with state and federal requirements.

Once you are sure the form is accurate, click the Acquire now button to obtain the form. Choose the payment plan you desire and enter the necessary information. Create your account and pay for the transaction using your PayPal account or credit card. Select the file format and download the legal document format to your device. Complete, modify, print, and sign the acquired Connecticut Partnership Agreement for Startup. US Legal Forms is the largest repository of legal forms where you can find numerous document templates. Utilize the service to obtain professionally created paperwork that adheres to state specifications.

- If you are currently registered, Log In to your account and then click the Obtain button to access the Connecticut Partnership Agreement for Startup.

- Use your account to search for the legal forms you have purchased previously.

- Visit the My documents tab of your account to retrieve another copy of the document you need.

- If you are a new user of US Legal Forms, here are simple steps for you to follow.

- First, ensure that you have selected the correct form for your city/state. You can preview the form using the Review button and check the form details to confirm this is the right one for you.

- If the form does not meet your needs, use the Search field to find the appropriate form.

Form popularity

FAQ

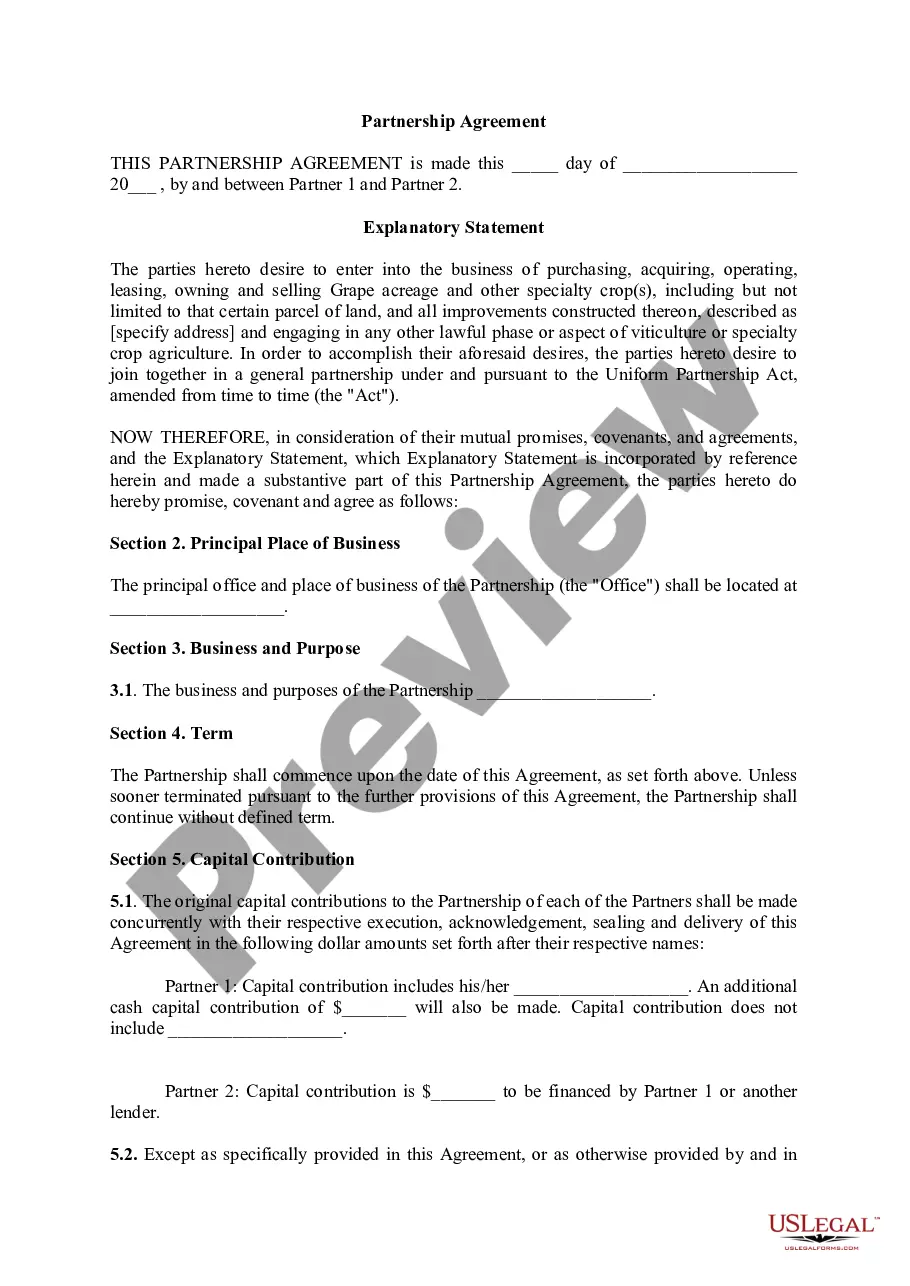

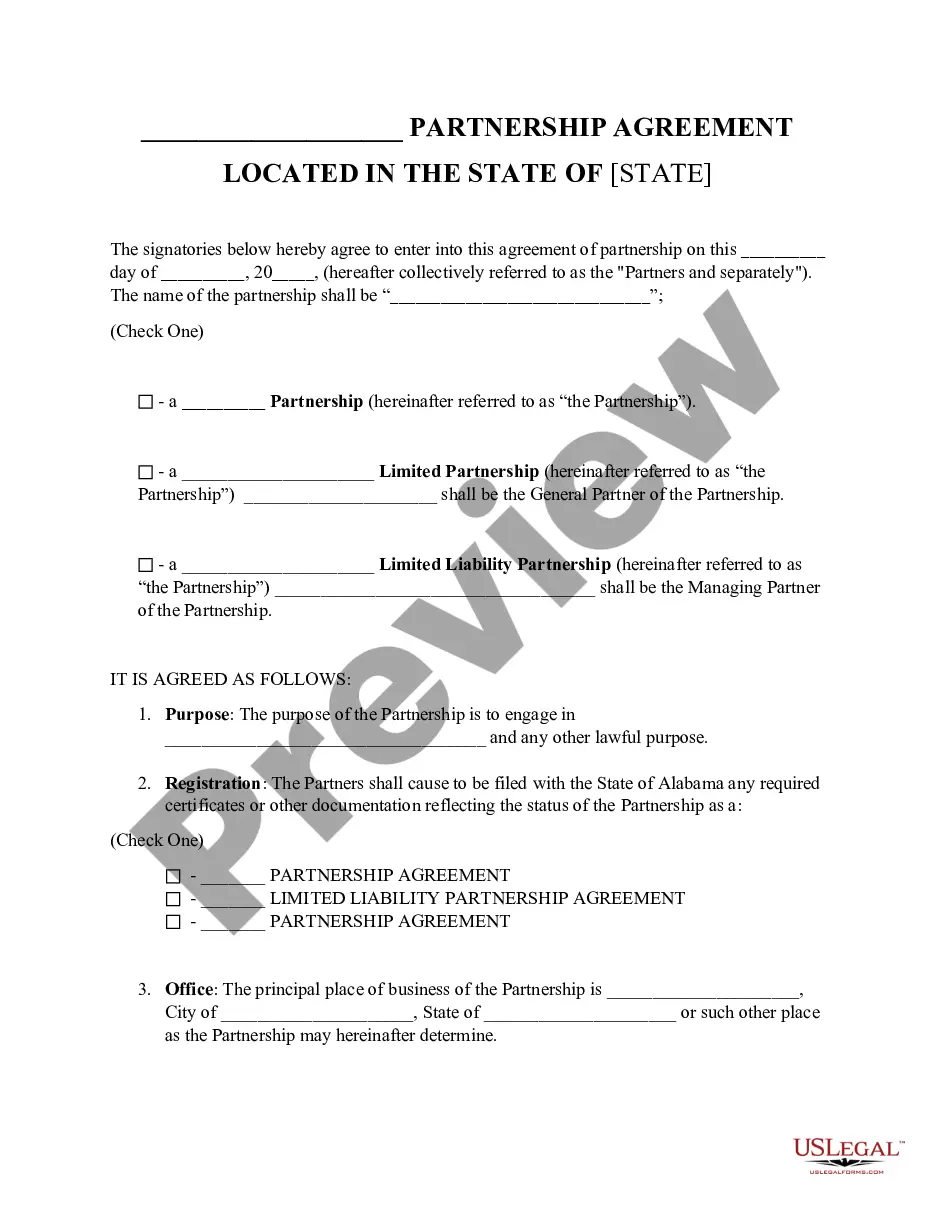

Setting up a partnership agreement involves discussing key topics with your partners, such as profit sharing, decision-making processes, and partner roles. Use the Connecticut Partnership Agreement for Startup as a guideline to ensure all necessary elements are included. Draft the agreement in clear language, and consider legal assistance for compliance with state laws. Finally, ensure all partners review, sign, and retain a copy of the agreement.

Based on ContractsCounsel's marketplace data, the average cost of a project involving a partnership agreement is $603.89 . Partnership agreement cost depends on many variables, which includes the service requested, number of partners, and the number of custom terms needed to be included in the document.

Create a General Partnership in ConnecticutDetermine if you should start a general partnership.Choose a business name.File a DBA name (if needed)Draft and sign partnership agreement.Obtain licenses, permits, and clearances.Get an Employer Identification Number (EIN)Get Connecticut state tax identification numbers.

Individuals who are committed to a business venture can be business partners. Likewise, together you can choose from a number of different structures to establish the business, such as a: partnership; company; or.

Step 1: Register the business name (Department of Trade Industry). Step 2: Have the partnership agreement (Articles of Partnership) notarized and registered with the SEC. Step 3: Obtain a Tax Identification Number for the partnership from the BIR. Step 4: Obtain pertinent municipal licenses from the local government.

It's ultimately up to you and the partners to decide how to create the partnership agreement. It's a legal contract, so it should be worded as such, and signed by all parties. You can choose an online template, create one yourself or speak to an attorney to draw up the contract.

A partnership agreement should outline how the partners intend to manage and operate the business. Then, you will need to register as a partnership. This will include tax registration and obtaining the necessary licences and registrations. You will also need a separate bank account for your partnership.

Going it alone will certainly give you full autonomy and control of your business, but a partner may allow you to expand into a more dynamic approach.

In this way, a partnership agreement is similar to corporate bylaws or a limited liability company's (LLC) operating agreement. There's no state that requires a partnership agreement, and it's possible to start a business without one.

Here are the basic steps to forming a partnership:Choose a business name.Register a fictitious business name.Draft and sign a partnership agreement.Comply with tax and regulatory requirements.Obtain Insurance.