Connecticut Challenge to Credit Report of Experian, TransUnion, and/or Equifax

Description

How to fill out Challenge To Credit Report Of Experian, TransUnion, And/or Equifax?

Are you inside a situation that you require documents for possibly organization or specific purposes just about every day time? There are plenty of authorized file templates available online, but getting ones you can rely is not straightforward. US Legal Forms gives a large number of form templates, just like the Connecticut Challenge to Credit Report of Experian, TransUnion, and/or Equifax, that happen to be created to fulfill state and federal requirements.

In case you are currently acquainted with US Legal Forms site and possess an account, just log in. Afterward, it is possible to acquire the Connecticut Challenge to Credit Report of Experian, TransUnion, and/or Equifax design.

Should you not offer an bank account and want to begin to use US Legal Forms, follow these steps:

- Get the form you require and ensure it is to the appropriate area/county.

- Use the Preview option to check the shape.

- See the information to ensure that you have selected the appropriate form.

- If the form is not what you are seeking, make use of the Search field to get the form that meets your requirements and requirements.

- When you discover the appropriate form, simply click Buy now.

- Select the pricing prepare you would like, submit the required details to generate your money, and purchase the order using your PayPal or Visa or Mastercard.

- Pick a convenient document formatting and acquire your version.

Locate each of the file templates you possess bought in the My Forms food list. You can aquire a more version of Connecticut Challenge to Credit Report of Experian, TransUnion, and/or Equifax whenever, if possible. Just click on the essential form to acquire or print the file design.

Use US Legal Forms, the most extensive collection of authorized forms, to save lots of time as well as prevent mistakes. The service gives skillfully made authorized file templates which you can use for an array of purposes. Create an account on US Legal Forms and commence creating your life a little easier.

Form popularity

FAQ

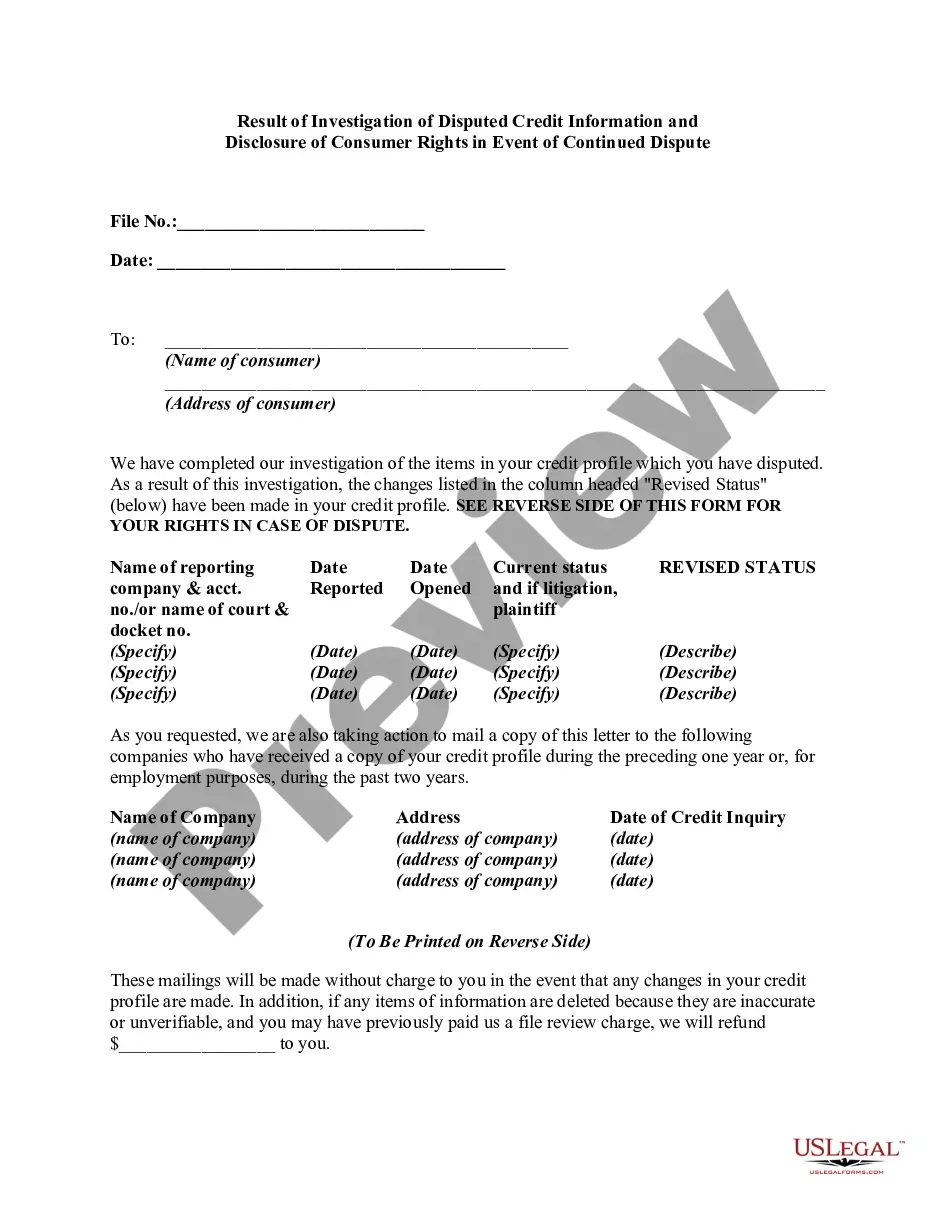

If you discover information on your credit report that shouldn't be there, you can request to have it removed in a process known as a dispute. To dispute credit report information, you'll need to contact the credit bureau in whose report you found the error.

You cannot initiate a rapid rescore on your own. Instead, you'll need to rely on a creditor that provides these services, such as a credit card company or another type of lender.

What do I do if I see an inquiry I don't recognize on my credit report? Contact the lender directly to ask them about the inquiry. If they find it was made in error, ask them to inform the credit reporting agencies. If the lender finds the inquiry was made fraudulently, report it to the FTC.

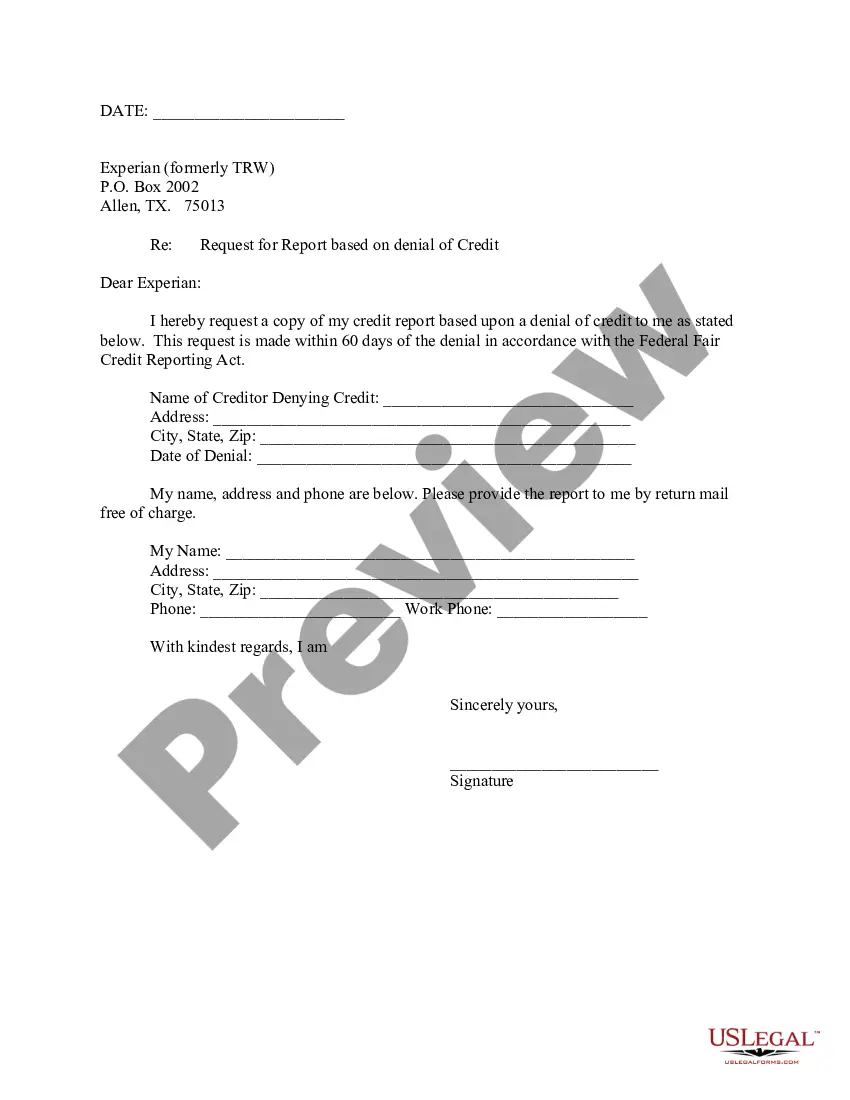

The credit bureaus also accept disputes online or by phone: Experian (888) 397-3742. Transunion (800) 916-8800. Equifax (866) 349-5191.

If you identify an error on your credit report, you should start by disputing that information with the credit reporting company (Experian, Equifax, and/or Transunion). You should explain in writing what you think is wrong, why, and include copies of documents that support your dispute.

Dispute mistakes with the credit bureaus. You should dispute with each credit bureau that has the mistake. Explain in writing what you think is wrong, include the credit bureau's dispute form (if they have one), copies of documents that support your dispute, and keep records of everything you send.

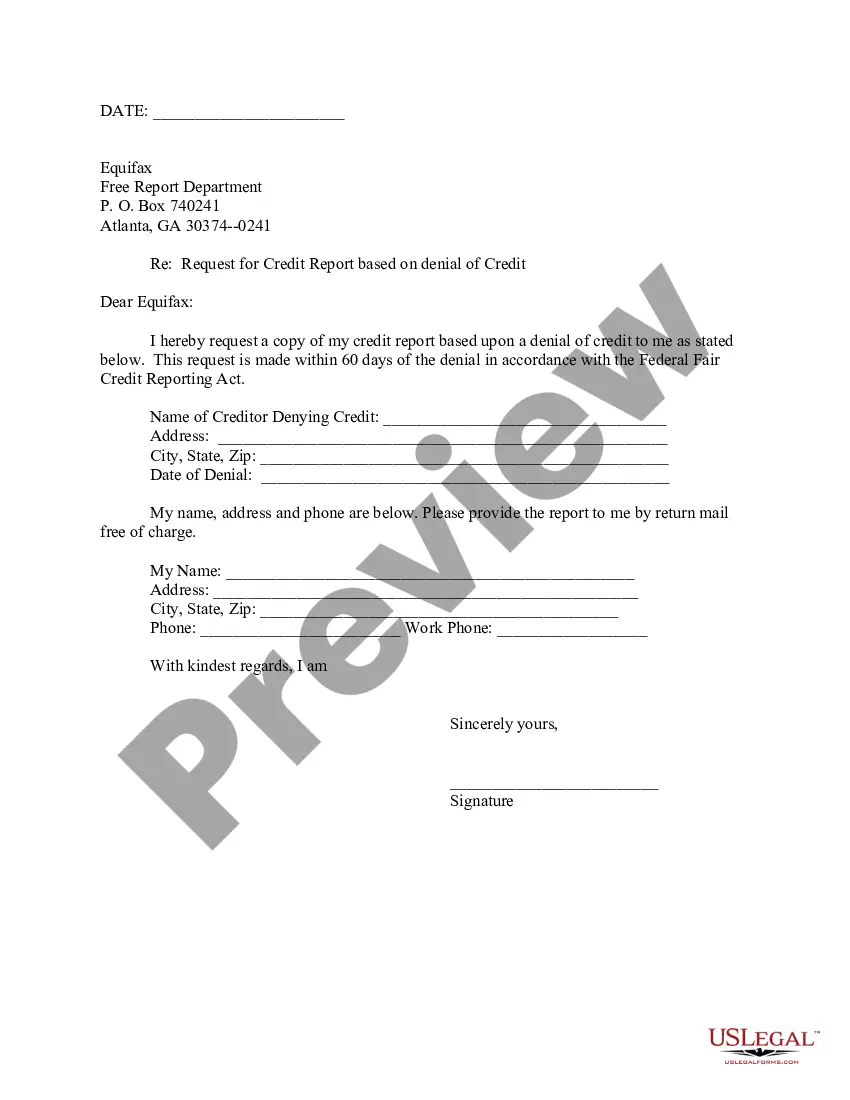

A dispute with additional relevant information can also be submitted by mail to Experian at P.O. Box 4500, Allen, TX 75013.