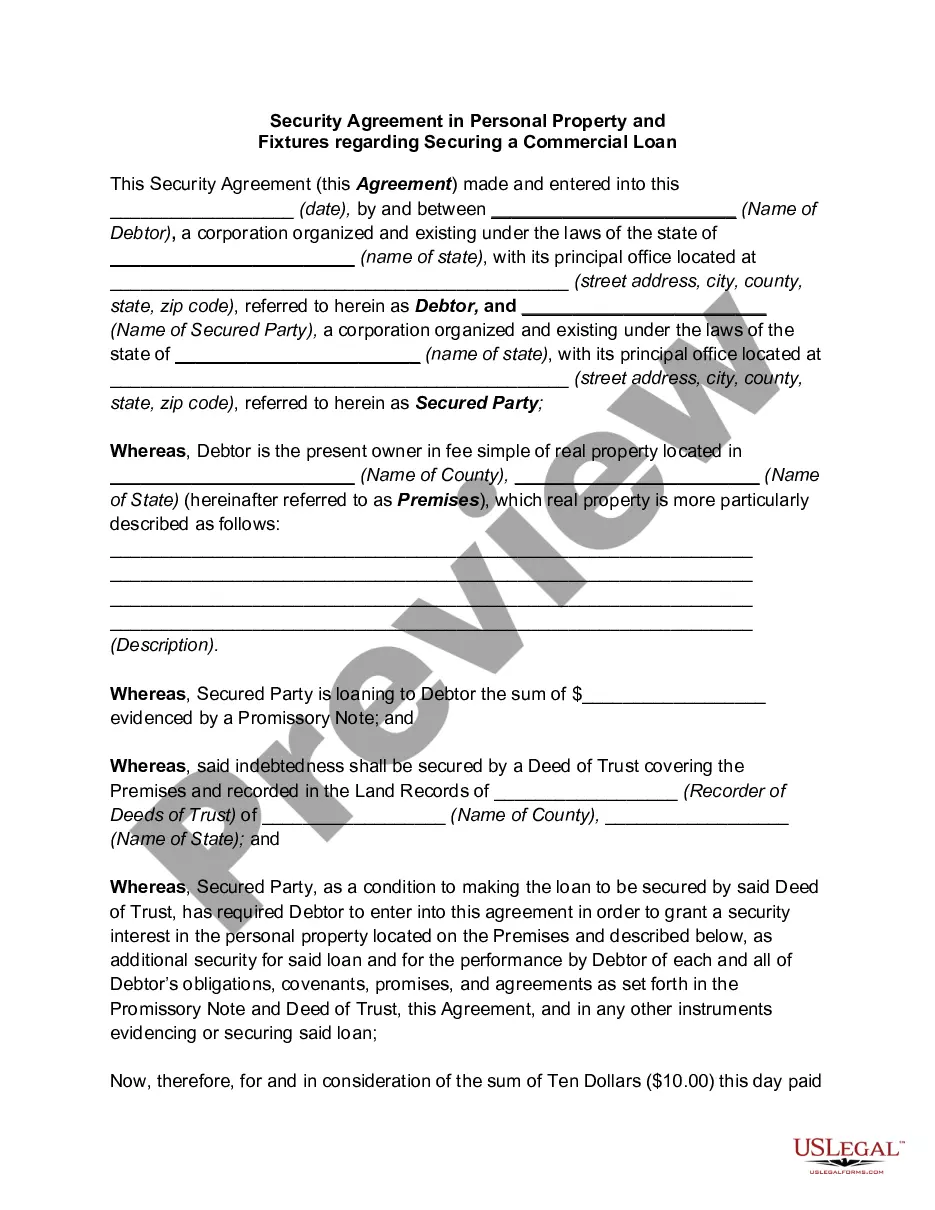

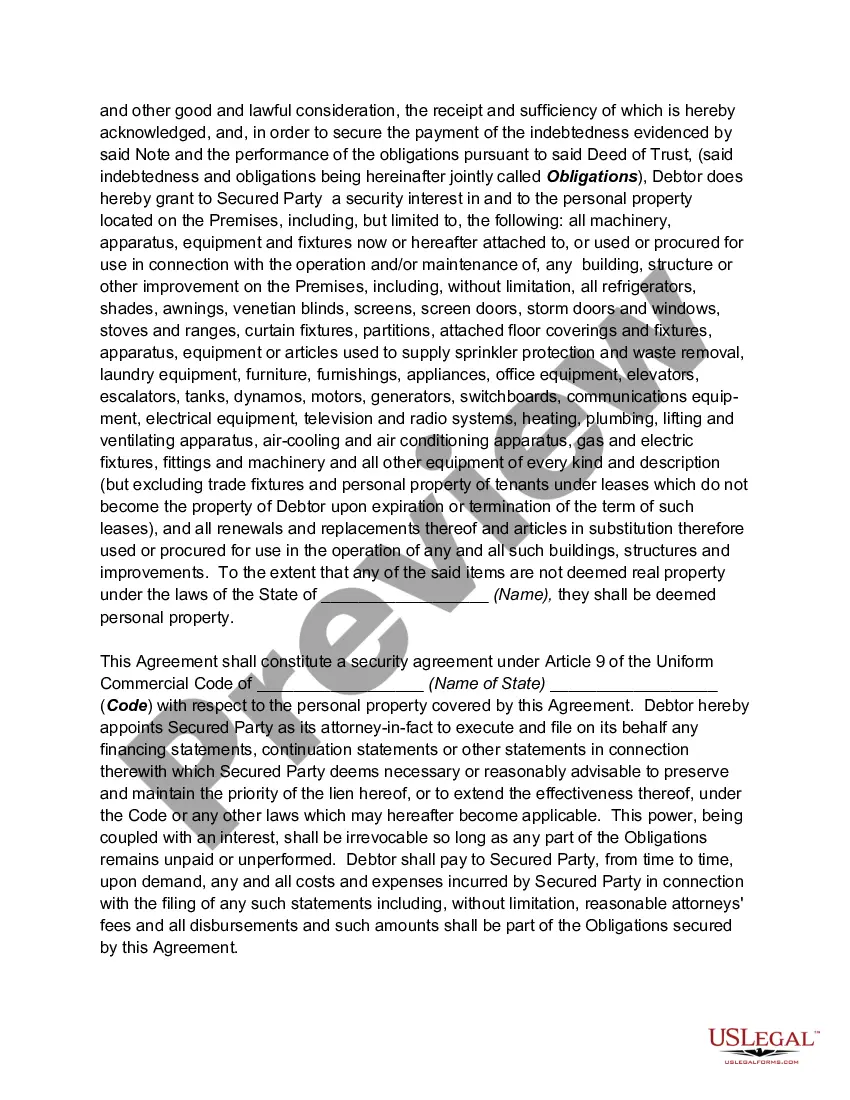

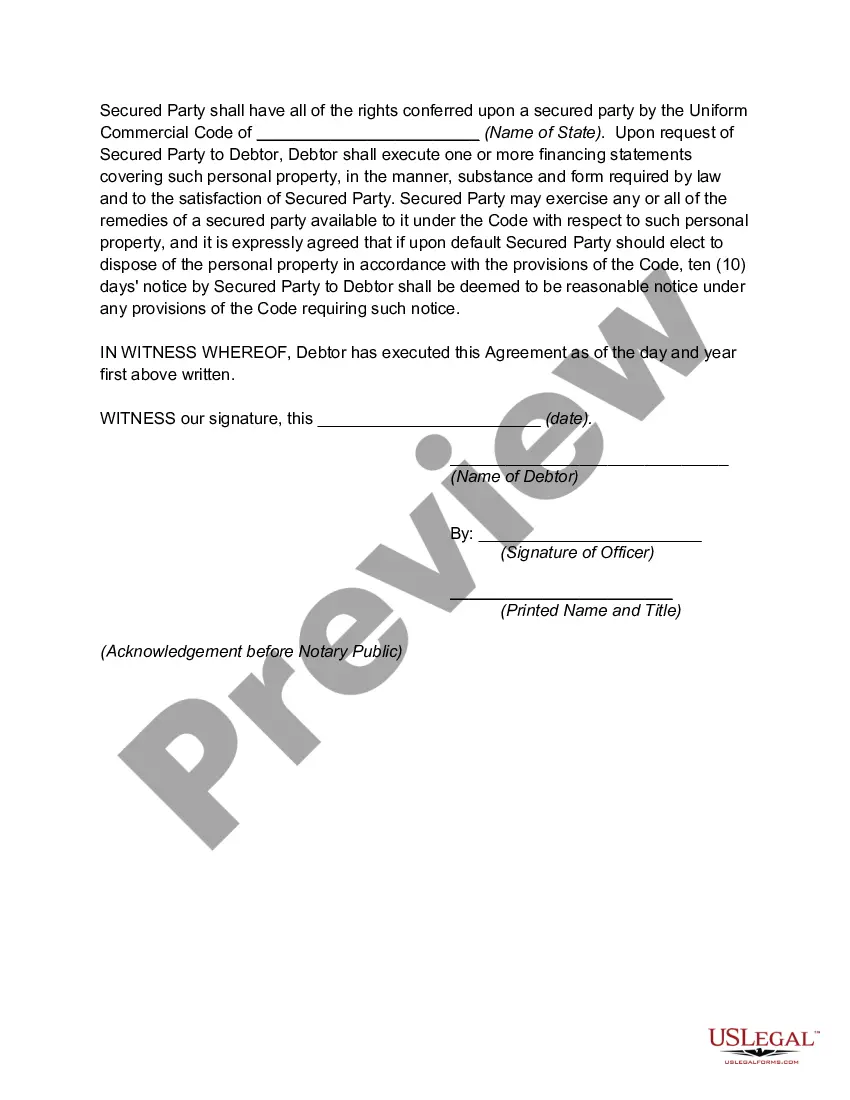

Connecticut Security Agreement in Personal Property Fixtures plays a crucial role in securing commercial loans within the state. This legally binding agreement serves to protect lenders by providing collateral in the form of personal property fixtures owned by the borrower. Understanding the intricacies of this agreement is essential for both lenders and borrowers involved in commercial loan transactions. A Connecticut Security Agreement in Personal Property Fixtures creates a lien on certain fixed assets owned by the borrower, serving as security for the lender in case of default. Personal property fixtures refer to items attached to the real property that are considered personal property, such as machinery, equipment, furniture, and certain improvements. These fixtures are often essential for the operations of a commercial enterprise. By entering into this agreement, the borrower grants the lender a security interest in the personal property fixtures listed in the document. This means that the lender has the legal right to seize and sell these assets to recover the outstanding debt in the event of default or non-payment. The agreement establishes the terms and conditions under which the lender can exercise this right, ensuring transparency and fairness for both parties involved. Connecticut's law recognizes different types of Security Agreements in Personal Property Fixtures, depending on the nature of the property and the loan being secured: 1. General Security Agreement: This agreement covers a variety of personal property fixtures, allowing the lender to claim a security interest in all the borrower's personal property fixtures, present, and future. 2. Specific Security Agreement: In this type of agreement, the lender has a security interest in specific personal property fixtures designated and listed within the agreement. This type of agreement is often used when financing a specific asset or equipment. 3. After-Acquired Property Agreement: This agreement allows the lender to claim a security interest in personal property fixtures acquired by the borrower after the agreement has been executed. It provides the lender with additional protection by covering any new assets purchased by the borrower during the loan term. It is essential for both lenders and borrowers to consult legal professionals experienced in Connecticut commercial lending laws to ensure the correct type of Security Agreement in Personal Property Fixtures is utilized for each transaction. Complying with the requirements of the agreement, including proper descriptions of the personal property fixtures, is crucial to enforceability and the overall success of the commercial loan.

Connecticut Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan

Description

How to fill out Connecticut Security Agreement In Personal Property Fixtures Regarding Securing A Commercial Loan?

US Legal Forms - one of the greatest libraries of legal forms in the United States - delivers a wide range of legal record themes you can down load or printing. Utilizing the site, you will get a large number of forms for organization and specific uses, categorized by groups, claims, or keywords.You will find the most up-to-date types of forms such as the Connecticut Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan in seconds.

If you currently have a subscription, log in and down load Connecticut Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan through the US Legal Forms collection. The Down load button will show up on each kind you look at. You have accessibility to all in the past downloaded forms within the My Forms tab of the accounts.

If you wish to use US Legal Forms the first time, allow me to share basic instructions to get you started:

- Make sure you have picked the correct kind for your personal area/state. Select the Review button to review the form`s content material. Look at the kind outline to actually have selected the right kind.

- If the kind doesn`t satisfy your specifications, use the Research industry at the top of the screen to get the one that does.

- In case you are happy with the shape, affirm your choice by clicking the Purchase now button. Then, choose the rates strategy you like and offer your qualifications to sign up for the accounts.

- Approach the transaction. Utilize your Visa or Mastercard or PayPal accounts to accomplish the transaction.

- Find the structure and down load the shape on your own product.

- Make changes. Complete, revise and printing and indicator the downloaded Connecticut Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan.

Every single design you added to your bank account does not have an expiry particular date which is the one you have forever. So, in order to down load or printing an additional version, just check out the My Forms portion and click on on the kind you will need.

Obtain access to the Connecticut Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan with US Legal Forms, the most comprehensive collection of legal record themes. Use a large number of specialist and status-distinct themes that fulfill your business or specific requirements and specifications.

Form popularity

FAQ

Security Interest: An interest in personal property or fixtures -- i.e., improvements to real property -- which secures payment or performance of an obligation. Security Agreement: An agreement creating or memorializing a security interest granted by a debtor to a secured party.

ATTACHMENT AND ENFORCEABILITY OF SECURITY INTEREST; PROCEEDS; SUPPORTING OBLIGATIONS; FORMAL REQUISITES. (a) [Attachment.] A security interest attaches to collateral when it becomes enforceable against the debtor with respect to the collateral, unless an agreement expressly postpones the time of attachment.

A secured transaction is an agreement between two parties in which one of the parties gives property (other than real estate) as collateral, or security, for a loan. There are two types of secured transactions.

Signature Required A signature of the debtor, and the owner of the collateral if the owner is different party, must sign the security agreement in order for the security agreement to be effective. This is obviously important, and it is a strict rule.

Let's consider an example. Credit transactions involving large ticket items, such as cars, homes or appliances, are usually secured. When I bought my new car, I borrowed money from my bank for my car loan. My loan is a secured transaction.

Security interest is an interest in personal property or fixtures that secures payment or performance of an obligation. Secured party is a lender, seller, or other person in whose favor a security interest exists.

Security Interest: An interest in personal property or fixtures -- i.e., improvements to real property -- which secures payment or performance of an obligation. Security Agreement: An agreement creating or memorializing a security interest granted by a debtor to a secured party.

A lien is a claim or legal right against assets that are typically used as collateral to satisfy a debt. A creditor or a legal judgment could establish a lien. A lien serves to guarantee an underlying obligation, such as the repayment of a loan.