This form is a business type form that is formatted to allow you to complete the form using Adobe Acrobat or Word. The word files have been formatted to allow completion by entry into fields. Some of the forms under this category are rather simple while others are more complex. The formatting is worth the small cost.

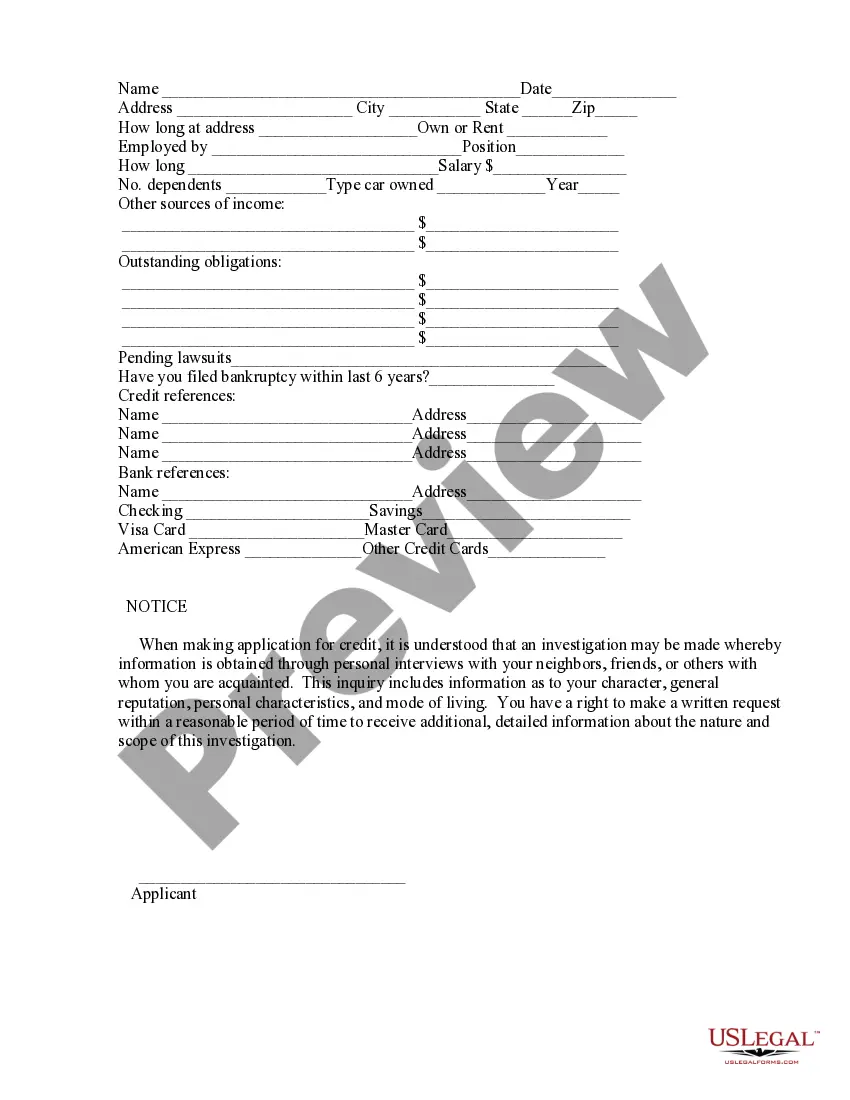

Connecticut Credit Inquiry

Category:

State:

Multi-State

Control #:

US-135-AZ

Format:

Word;

PDF;

Rich Text

Instant download

Description

How to fill out Credit Inquiry?

If you want to be thorough, acquire, or print out sanctioned document templates, utilize US Legal Forms, the top variety of legal forms available online.

Employ the site’s straightforward and user-friendly search to find the documents you need.

Various templates for business and personal purposes are categorized by type and region, or keywords.

Step 4. Once you've found the form you need, click the Buy now button. Choose your pricing plan and enter your details to create an account.

Step 5. Process the payment. You can use your credit card or PayPal account for the transaction.

- Utilize US Legal Forms to acquire the Connecticut Credit Inquiry with just a few clicks.

- If you are already a US Legal Forms user, Log In to your account and then click the Download button to obtain the Connecticut Credit Inquiry.

- You can also reach forms you previously downloaded in the My documents section of your account.

- If this is your first time using US Legal Forms, follow the steps below.

- Step 1. Ensure you have selected the form for the appropriate city/state.

- Step 2. Use the Preview option to view the form's content. Remember to read the details.

- Step 3. If you are not satisfied with the form, utilize the Search field at the top of the screen to find other versions of the legal form template.

Form popularity

FAQ

Though prospective employers don't see your credit score in a credit check, they do see your open lines of credit (such as mortgages), outstanding balances, auto or student loans, foreclosures, late or missed payments, any bankruptcies and collection accounts.

The idea of removing hard inquiries from your credit report to improve your credit score may sound appealing. But disputing a genuine hard inquiry on your credit report will likely not result in any change to your scores. You can, however, dispute ones that are a result of fraud.

Filing a dispute has no impact on your score, however, if information on your credit report changes after your dispute is processed, your credit scores could change.

If you find an unauthorized or inaccurate hard inquiry, you can file a dispute letter and request that the bureau remove it from your report. The consumer credit bureaus must investigate dispute requests unless they determine your dispute is frivolous. Still, not all disputes are accepted after investigation.

This information is reported to Equifax by your lenders and creditors and includes the types of accounts (for example, a credit card, mortgage, student loan, or vehicle loan), the date those accounts were opened, your credit limit or loan amount, account balances, and your payment history.

If you spot a hard credit inquiry on your credit report and it's legitimate (i.e., you knew you were applying for credit), there's nothing you can do to remove it besides wait. It won't impact your score after 12 months and will fall off your credit report after two years.

Consumer reporting agencies have 5 business days after completing an investigation to notify you of the results. Generally, they must investigate the dispute within 30 days of receiving it. However, it has 45 days to investigate if you dispute after receiving your free annual credit report.

The period of time may vary depending on the credit scoring model used, but it's typically from 14 to 45 days.

All new auto or mortgage loan or utility inquiries will show on your credit report; however, only one of the inquiries within a specified window of time will impact your credit score. This exception generally does not apply to other types of loans, such as credit cards.

If you file a dispute to correct what you believe is an inaccuracy on your credit report, the credit bureau you notify must complete an investigation within 30 days (or 45 days in certain circumstances), according to the U.S. Fair Credit Reporting Act. But most disputes are resolved more quickly than that.