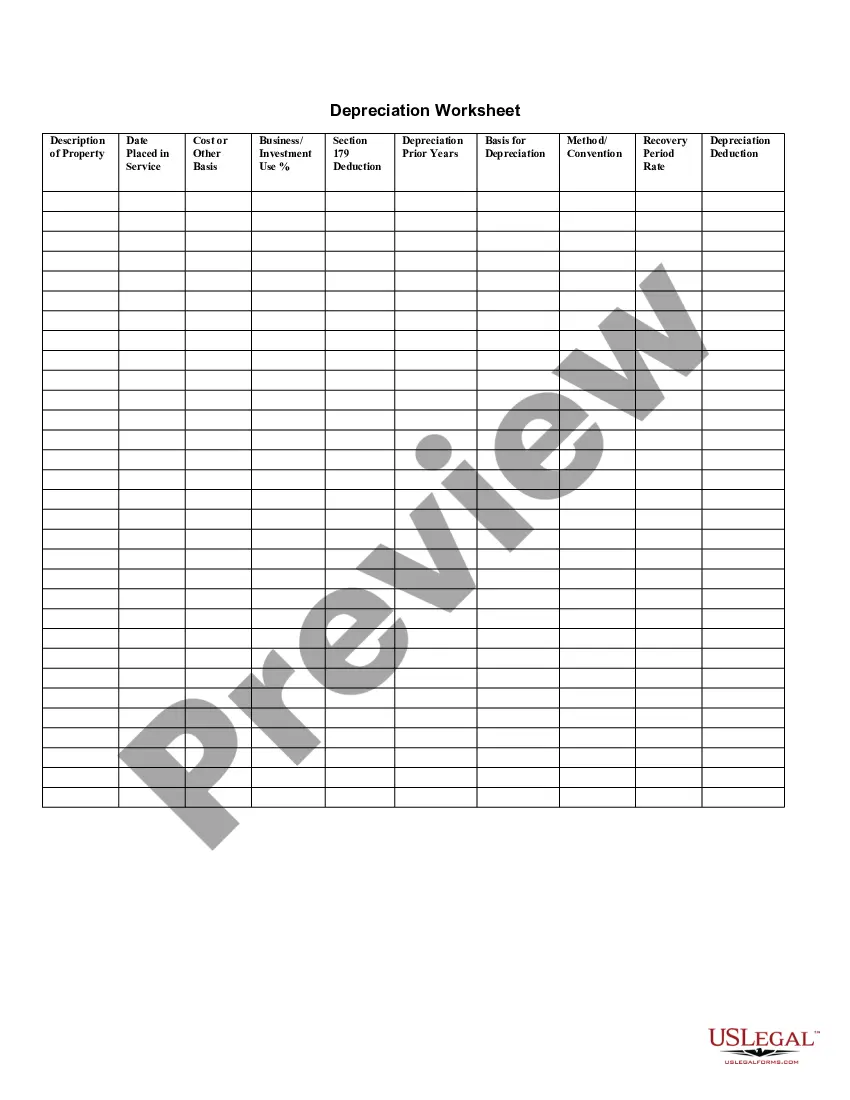

Connecticut Depreciation Schedule

Description

How to fill out Depreciation Schedule?

Selecting the finest approved document template can be challenging.

Of course, there are numerous templates accessible online, but how can you acquire the legal document you require.

Utilize the US Legal Forms website.

If you are a new user of US Legal Forms, here are simple instructions you should follow: First, ensure you have chosen the correct form for your city/region. You can view the form using the Preview button and read the form description to confirm it is suitable for you. If the form does not meet your requirements, use the Search field to locate the appropriate form. Once you are confident that the form is suitable, select the Buy now button to acquire the form. Choose the pricing plan you prefer and enter the required information. Set up your account and process the order using your PayPal account or credit card. Select the file format and download the legal document template to your device. Finally, complete, modify, print, and sign the received Connecticut Depreciation Schedule. US Legal Forms is the largest repository of legal documents where you can find a variety of document templates. Use the service to obtain properly crafted files that adhere to state specifications.

- The service offers thousands of templates, such as the Connecticut Depreciation Schedule, suitable for both business and personal purposes.

- All documents are vetted by professionals and comply with state and federal regulations.

- If you are already registered, sign in to your account and click on the Download button to obtain the Connecticut Depreciation Schedule.

- Use your account to search through the legal documents you have previously ordered.

- Navigate to the My documents tab of your account to get an additional copy of the document you need.

Form popularity

FAQ

2. Depreciation limitations have been put into place. Effective 1/1/18 for individuals and corporations, 80% of Section 179 expense is disallowed. 25% of the disallowed portion will be taken as an expense in the next four years (in effect 20% over 5 years).

For income years beginning on or after January 1, 2018, Connecticut has decoupled from federal changes affecting the business interest deduction under I.R.C. § 163(j).

The total section 179 deduction and depreciation you can deduct for a passenger automobile, including a truck or van, you use in your business and first placed in service in 2021 is $18,200, if the special depreciation allowance applies, or $10,200, if the special depreciation allowance does not apply.

The states listed as conforming to the TCJA bonus depreciation rules allow for the 100% deduction of qualified property....States that have adopted the new bonus depreciation rules:Alabama.Alaska.Colorado.Delaware.Illinois.Kansas.Louisiana.Michigan.More items...

27, 2017, and placed in service during calendar year 2020, the depreciation limit under Sec. 280F(d)(7) is $18,100 for the first tax year; $16,100 for the second tax year; $9,700 for the third tax year; and $5,760 for each succeeding year, all unchanged from 2019. Under Sec.

Corporate: Connecticut does not conform to the federal treatment of bonus depreciation, because Connecticut has passed legislation decoupling from I.R.C. § 168(k).

The portion of the business standard mileage rate that is treated as depreciation will be 27 cents per mile for 2020, 1 cent more than 2019, one of the few amounts that is increasing.

For tax years 2015 through 2017, first-year bonus depreciation was set at 50%. It was scheduled to go down to 40% in 2018 and 30% in 2019, and then not be available in 2020 and beyond. The Tax Cuts and Jobs Act, enacted at the end of 2018, increases first-year bonus depreciation to 100%.

Business Interest Expense For income years beginning on or after January 1, 2018, Connecticut has decoupled from federal changes affecting the business interest deduction under I.R.C. § 163(j).