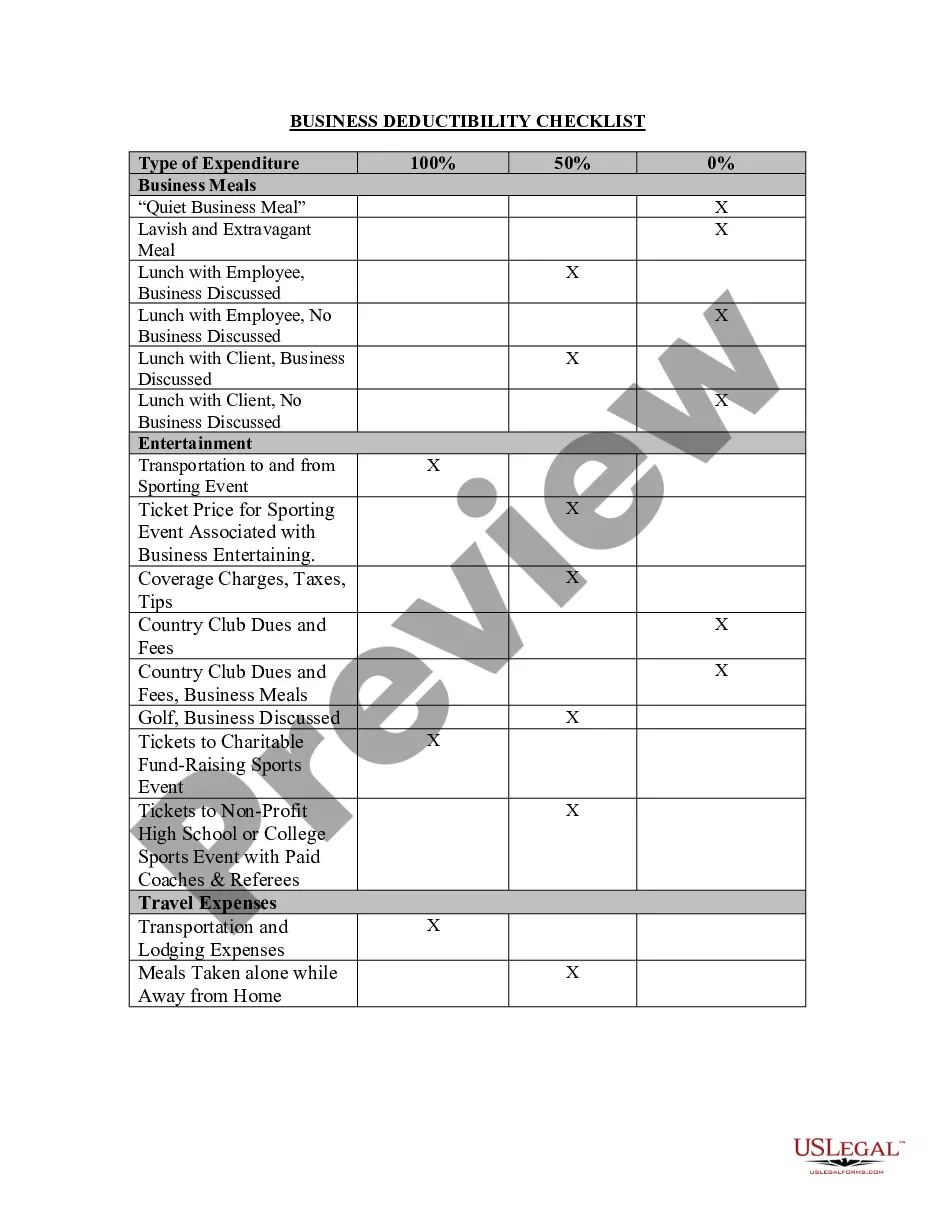

Statutory Guidelines [Appendix A(6) Revenue Procedure 93-34] regarding rules under which a designated settlement fund described in section 468B(d)(2) of the Internal Revenue Code or a qualified settlement fund described in section 1.468B-1 of the Income Tax Regulations will be considered "a party to the suit or agreement" for purposes of section 130.

Connecticut Revenue Procedure 93-34 is an important document that provides guidance and instructions regarding various tax matters in the state of Connecticut. This revenue procedure outlines specific rules and procedures that taxpayers must follow when it comes to taxation, ensuring compliance and fair treatment for both businesses and individuals. By understanding the key aspects of Connecticut Revenue Procedure 93-34, taxpayers can avoid penalties, make accurate tax filings, and stay in compliance with state tax laws. Some relevant keywords associated with Connecticut Revenue Procedure 93-34 include tax guidance, tax regulations, state tax laws, Connecticut taxation, taxpayer compliance, tax filings, and tax penalties. This revenue procedure may cover various areas of taxation, including income tax, sales tax, property tax, and other relevant taxes imposed by the state of Connecticut. There might be different types or specific sections within Connecticut Revenue Procedure 93-34 that address particular tax issues or provide instructions for specific types of taxpayers. While specific types of this revenue procedure may vary, they could include sections on income tax deductions, tax credits, tax exemptions, corporate tax regulations, individual tax regulations, or even specific guidance for certain industries or professions. It is crucial for taxpayers to consult the most recent version of Connecticut Revenue Procedure 93-34 to ensure they have the latest information and comply with the most updated regulations. By doing so, individuals and businesses can accurately determine their tax obligations, take advantage of available tax benefits, and fulfill their responsibilities as taxpayers in the state of Connecticut.

Connecticut Revenue Procedure 93-34 is an important document that provides guidance and instructions regarding various tax matters in the state of Connecticut. This revenue procedure outlines specific rules and procedures that taxpayers must follow when it comes to taxation, ensuring compliance and fair treatment for both businesses and individuals. By understanding the key aspects of Connecticut Revenue Procedure 93-34, taxpayers can avoid penalties, make accurate tax filings, and stay in compliance with state tax laws. Some relevant keywords associated with Connecticut Revenue Procedure 93-34 include tax guidance, tax regulations, state tax laws, Connecticut taxation, taxpayer compliance, tax filings, and tax penalties. This revenue procedure may cover various areas of taxation, including income tax, sales tax, property tax, and other relevant taxes imposed by the state of Connecticut. There might be different types or specific sections within Connecticut Revenue Procedure 93-34 that address particular tax issues or provide instructions for specific types of taxpayers. While specific types of this revenue procedure may vary, they could include sections on income tax deductions, tax credits, tax exemptions, corporate tax regulations, individual tax regulations, or even specific guidance for certain industries or professions. It is crucial for taxpayers to consult the most recent version of Connecticut Revenue Procedure 93-34 to ensure they have the latest information and comply with the most updated regulations. By doing so, individuals and businesses can accurately determine their tax obligations, take advantage of available tax benefits, and fulfill their responsibilities as taxpayers in the state of Connecticut.