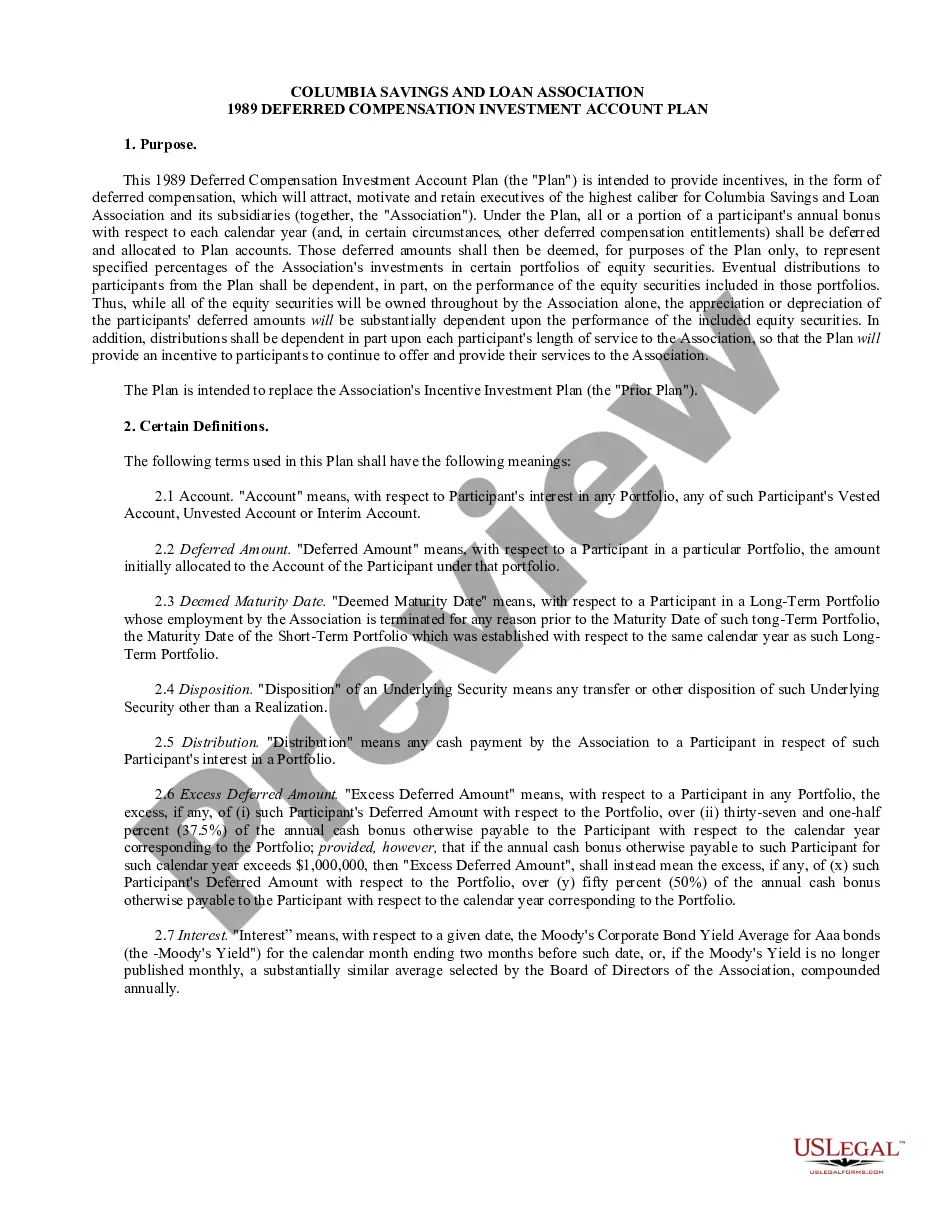

Connecticut Approval of deferred compensation investment account plan

Description

How to fill out Approval Of Deferred Compensation Investment Account Plan?

Are you presently within a place in which you will need files for possibly enterprise or individual purposes almost every time? There are plenty of lawful papers themes available on the net, but finding versions you can rely on is not easy. US Legal Forms delivers a huge number of type themes, such as the Connecticut Approval of deferred compensation investment account plan, that happen to be composed in order to meet state and federal specifications.

When you are previously acquainted with US Legal Forms web site and have an account, merely log in. Next, you are able to acquire the Connecticut Approval of deferred compensation investment account plan template.

Should you not have an account and want to begin to use US Legal Forms, adopt these measures:

- Discover the type you require and ensure it is for your correct city/region.

- Use the Review button to check the form.

- See the explanation to actually have selected the right type.

- When the type is not what you are seeking, make use of the Lookup area to find the type that meets your needs and specifications.

- Whenever you get the correct type, simply click Purchase now.

- Select the prices strategy you want, fill in the specified details to generate your bank account, and pay money for an order using your PayPal or Visa or Mastercard.

- Choose a hassle-free file file format and acquire your backup.

Discover all the papers themes you have bought in the My Forms food selection. You can get a extra backup of Connecticut Approval of deferred compensation investment account plan at any time, if required. Just go through the needed type to acquire or printing the papers template.

Use US Legal Forms, one of the most considerable selection of lawful forms, to conserve efforts and avoid errors. The support delivers expertly produced lawful papers themes that can be used for a range of purposes. Produce an account on US Legal Forms and commence generating your lifestyle a little easier.

Form popularity

FAQ

Investing your deferred compensation Your plan might offer you several options for the benchmark?often, major stock and bond indexes, the 10-year US Treasury note, the company's stock price, or the mutual fund choices in the company 401(k) plan.

What is the CT Retirement Security Program? MyCTSavings is a state-sponsored retirement savings program that provides a convenient way for employers to help their employees reach their financial goals. There's minimal administrative work necessary and the plan easily integrates with existing payroll systems.

Your plan may allow you to schedule ?in-service? withdrawals or distributions so you can access your deferred income prior to retirement to meet other financial goals or obligations. For example, at different points over the years, you may want to buy a new home or pay your child's college expenses.

If you take your deferred compensation payments over a period of 10 years or more, those payments will be taxed in the state where you reside, rather than in the state in which you earned the compensation, possibly reducing your state income taxes.

Deferred compensation plans are an incentive that employers use to hold onto key employees. Deferred compensation can be structured as either qualified or non-qualified under federal regulations. Some deferred compensation is made available only to top executives.

The amount you can defer (including pre-tax and Roth contributions) to all your plans (not including 457(b) plans) is $22,500 in 2023 ($20,500 in 2022; $19,500 in 2020 and 2021; $19,000 in 2021).

Depending on your plan provisions, the payment of the deferred compensation can also be structured to reduce your tax liability based on a series of installment payments or lump sum payments based on a specified time. By spreading out the payments, you potentially could reduce your income for each applicable year.

There are two types of deferred compensation plans: non-qualified and qualified. Non-qualified deferred compensation plans are also referred to as Section 409A or NQDC plans. Deferred compensation plans are not required for all employees.