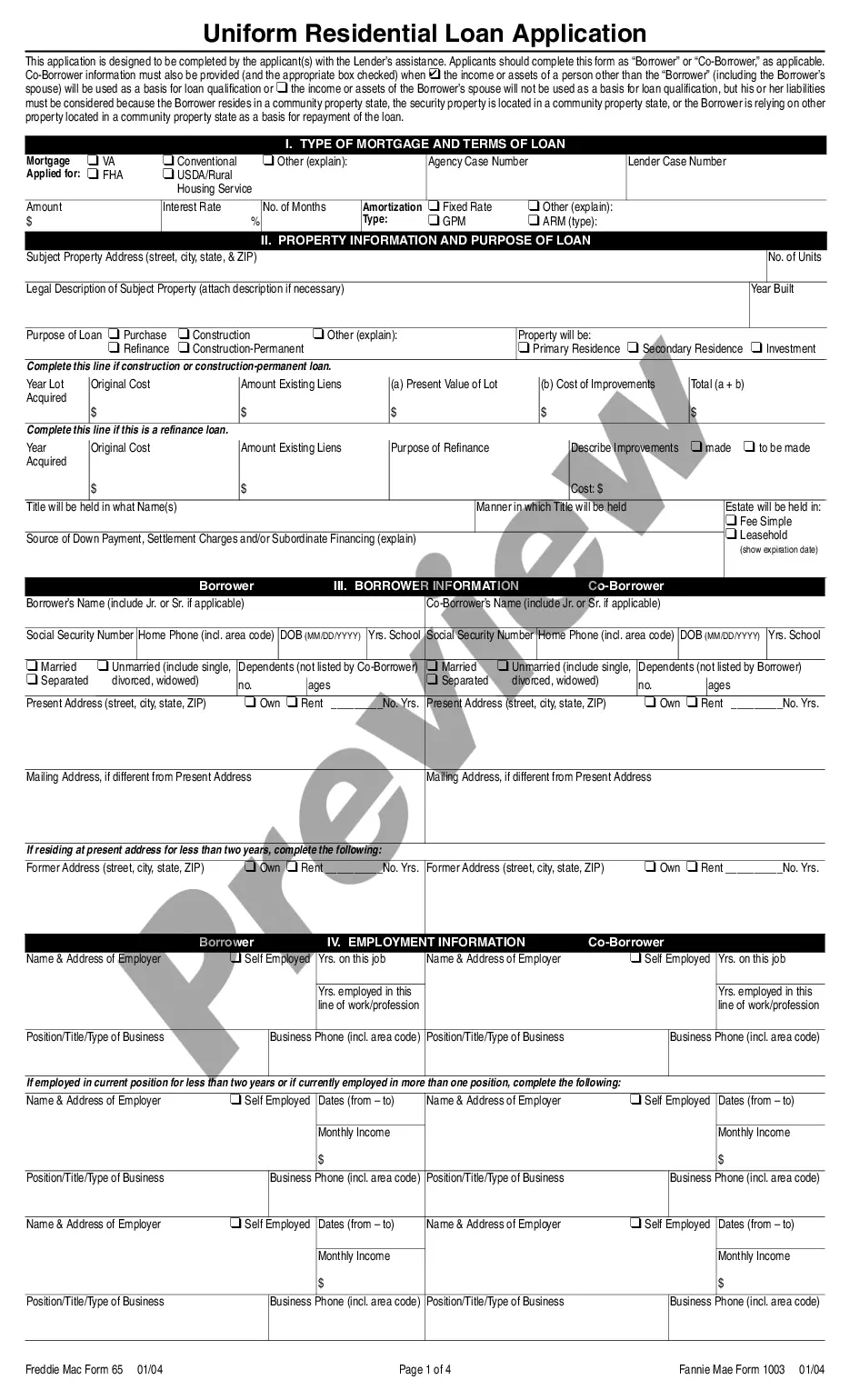

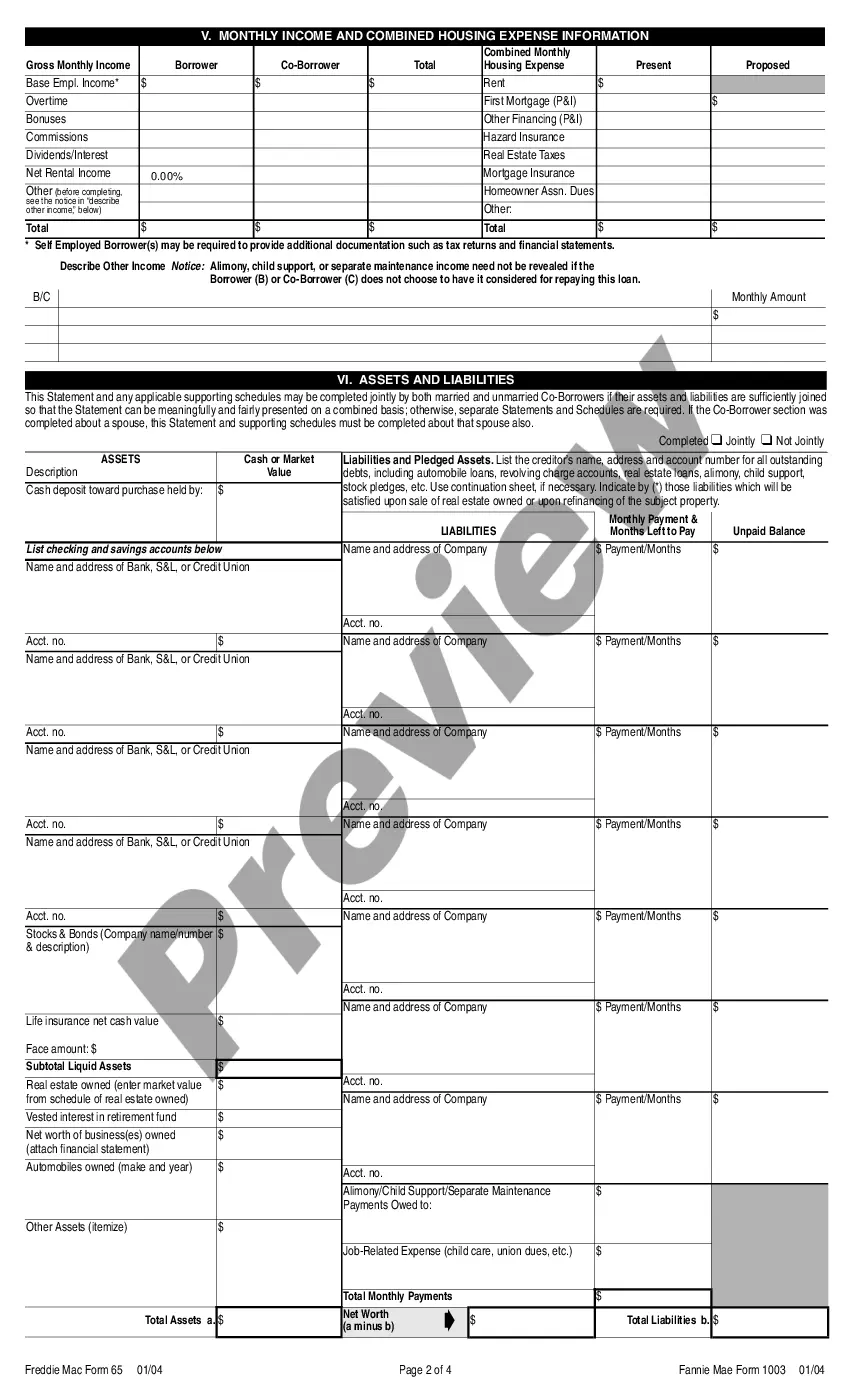

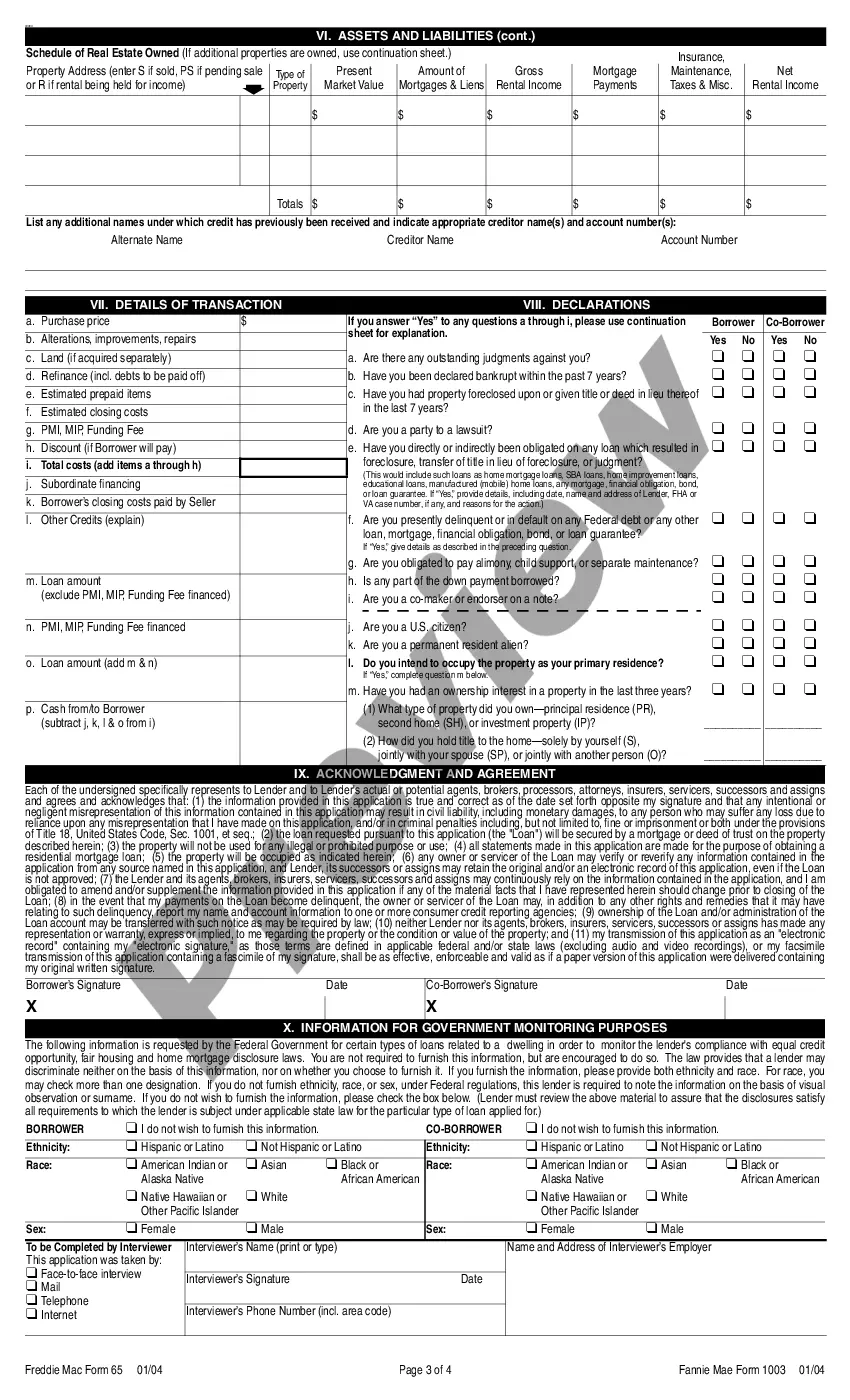

The Connecticut Uniform Residential Loan Application (also known as Form 1003) is a standardized mortgage loan application form used in the state of Connecticut. This application form is created by the Federal National Mortgage Association (Fannie Mae) and is widely utilized by lenders and borrowers during the loan origination process. The Connecticut Uniform Residential Loan Application is a comprehensive document that gathers all the necessary information from potential borrowers when applying for a residential mortgage loan. It provides lenders with a holistic view of the borrower's financial status, creditworthiness, employment history, and property details. This application assists lenders in evaluating the borrower's eligibility for a mortgage loan and determining the appropriate terms and conditions. The form collects crucial information, including the borrower's personal details, such as name, address, social security number, and marital status. It also delves into the borrower's employment history, income, assets, liabilities, and details about the property being financed, such as its address, purchase price, and purpose (primary residence, secondary residence, or investment property). Additionally, the Connecticut Uniform Residential Loan Application requires borrowers to disclose their existing debts, such as credit cards, student loans, car loans, and other outstanding obligations. This information assists lenders in assessing the borrower's overall debt-to-income ratio, a crucial factor in determining loan affordability and repayment ability. Furthermore, this loan application prompts borrowers to provide authorization for lenders to pull their credit reports from various credit bureaus. This enables lenders to review the borrower's creditworthiness, payment history, and credit scores, which play a significant role in the loan approval process. It's important to note that the Connecticut Uniform Residential Loan Application may have specific variations or supplemental forms based on the lender or loan program being utilized. For instance, there may be additional forms specific to government-backed loan programs like FHA (Federal Housing Administration) loans or VA (Department of Veterans Affairs) loans. These supplemental forms capture additional details needed to comply with the specific program requirements and eligibility criteria. In conclusion, the Connecticut Uniform Residential Loan Application is a crucial document used in the mortgage lending process. It serves as a standardized platform for borrowers to provide comprehensive information to lenders, allowing them to make informed decisions about loan approvals and terms. By supplying accurate and thorough data on this application, borrowers increase their chances of securing a favorable mortgage loan in the state of Connecticut.

Connecticut Uniform Residential Loan Application

Description

How to fill out Connecticut Uniform Residential Loan Application?

Finding the right lawful document design could be a have a problem. Obviously, there are tons of web templates accessible on the Internet, but how can you find the lawful type you need? Make use of the US Legal Forms website. The support provides a huge number of web templates, including the Connecticut Uniform Residential Loan Application, which can be used for organization and private needs. Every one of the types are checked out by pros and fulfill state and federal needs.

When you are previously listed, log in for your bank account and click the Down load option to obtain the Connecticut Uniform Residential Loan Application. Use your bank account to check with the lawful types you may have acquired in the past. Check out the My Forms tab of your bank account and acquire an additional backup of your document you need.

When you are a fresh consumer of US Legal Forms, listed here are basic guidelines that you can follow:

- Initially, make certain you have selected the correct type for your personal area/area. You are able to look over the form utilizing the Preview option and browse the form description to ensure this is basically the best for you.

- When the type fails to fulfill your preferences, take advantage of the Seach area to obtain the right type.

- When you are sure that the form would work, select the Get now option to obtain the type.

- Opt for the costs plan you want and type in the necessary information. Build your bank account and buy an order using your PayPal bank account or charge card.

- Choose the document file format and down load the lawful document design for your product.

- Full, modify and produce and sign the obtained Connecticut Uniform Residential Loan Application.

US Legal Forms may be the biggest collection of lawful types that you can see numerous document web templates. Make use of the company to down load appropriately-manufactured paperwork that follow express needs.