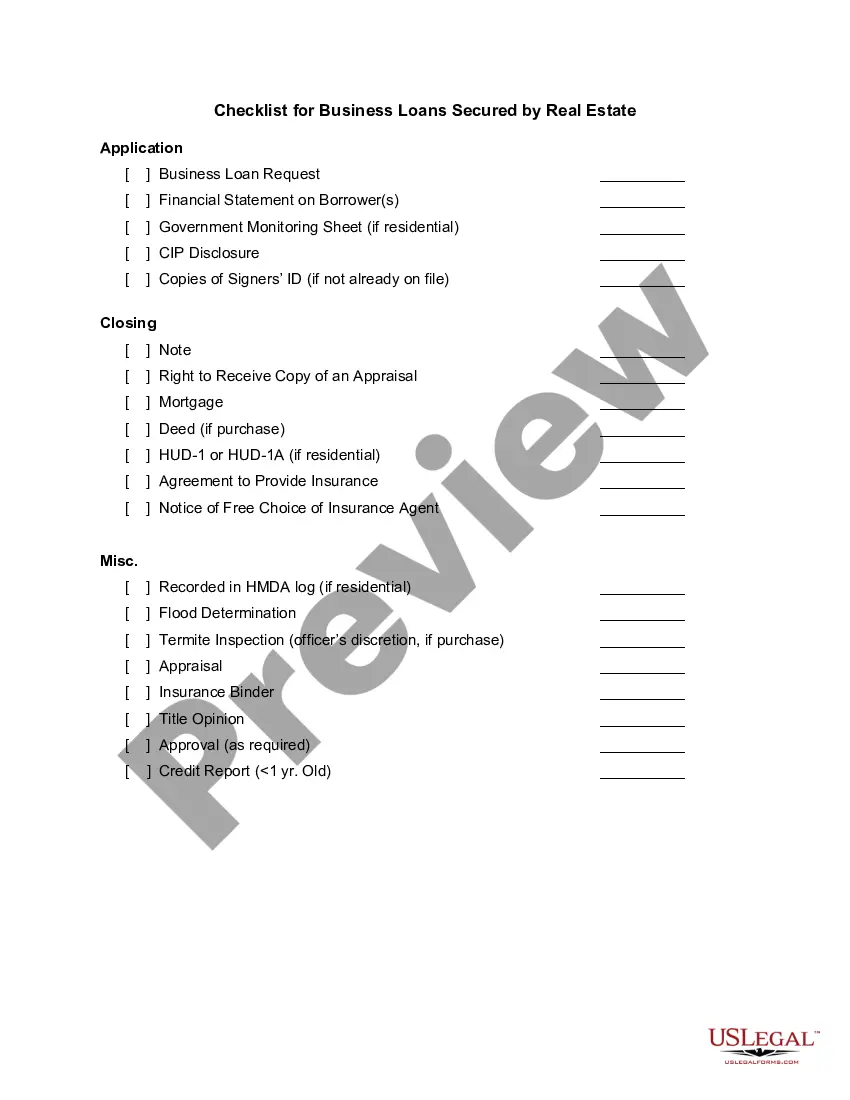

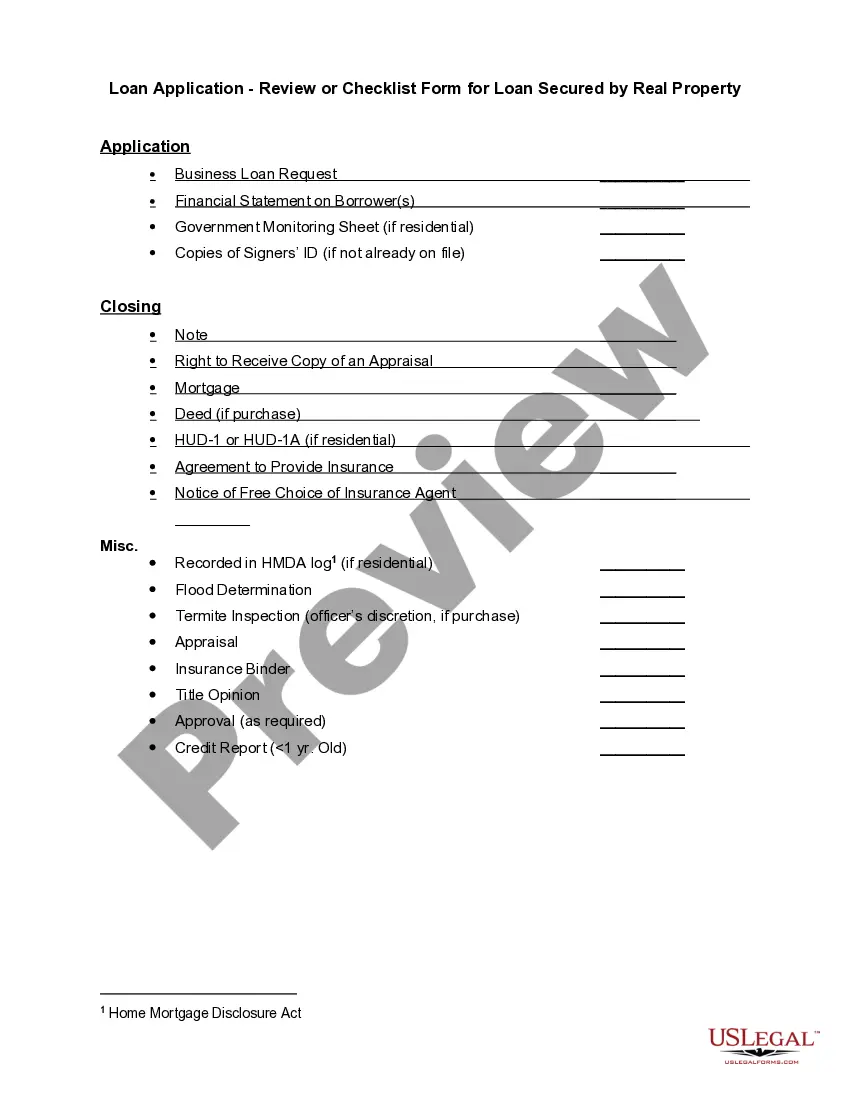

"Checklist for Real Estate Loans" is a American Lawyer Media form. This consist of many checklist that can be used for real estate loans.

Connecticut Checklist for Real Estate Loans

State:

Multi-State

Control #:

US-CRE897

Format:

Word;

PDF;

Rich Text

Instant download

Description

How to fill out Checklist For Real Estate Loans?

If you have to full, download, or printing lawful file layouts, use US Legal Forms, the biggest variety of lawful varieties, which can be found on-line. Make use of the site`s simple and easy hassle-free lookup to get the papers you will need. Various layouts for business and specific purposes are sorted by classes and states, or search phrases. Use US Legal Forms to get the Connecticut Checklist for Real Estate Loans within a handful of click throughs.

In case you are previously a US Legal Forms consumer, log in to your bank account and click the Acquire switch to get the Connecticut Checklist for Real Estate Loans. You may also entry varieties you formerly downloaded from the My Forms tab of the bank account.

If you work with US Legal Forms for the first time, follow the instructions beneath:

- Step 1. Ensure you have selected the shape for the appropriate area/land.

- Step 2. Utilize the Review option to check out the form`s articles. Don`t forget to learn the outline.

- Step 3. In case you are unsatisfied using the type, utilize the Research field at the top of the monitor to discover other types of your lawful type web template.

- Step 4. Upon having located the shape you will need, click the Buy now switch. Choose the pricing prepare you prefer and add your credentials to register on an bank account.

- Step 5. Method the transaction. You can utilize your bank card or PayPal bank account to finish the transaction.

- Step 6. Select the structure of your lawful type and download it on your own product.

- Step 7. Total, edit and printing or indication the Connecticut Checklist for Real Estate Loans.

Each lawful file web template you get is yours eternally. You may have acces to each type you downloaded in your acccount. Click on the My Forms portion and pick a type to printing or download again.

Compete and download, and printing the Connecticut Checklist for Real Estate Loans with US Legal Forms. There are thousands of professional and condition-certain varieties you can use to your business or specific requires.