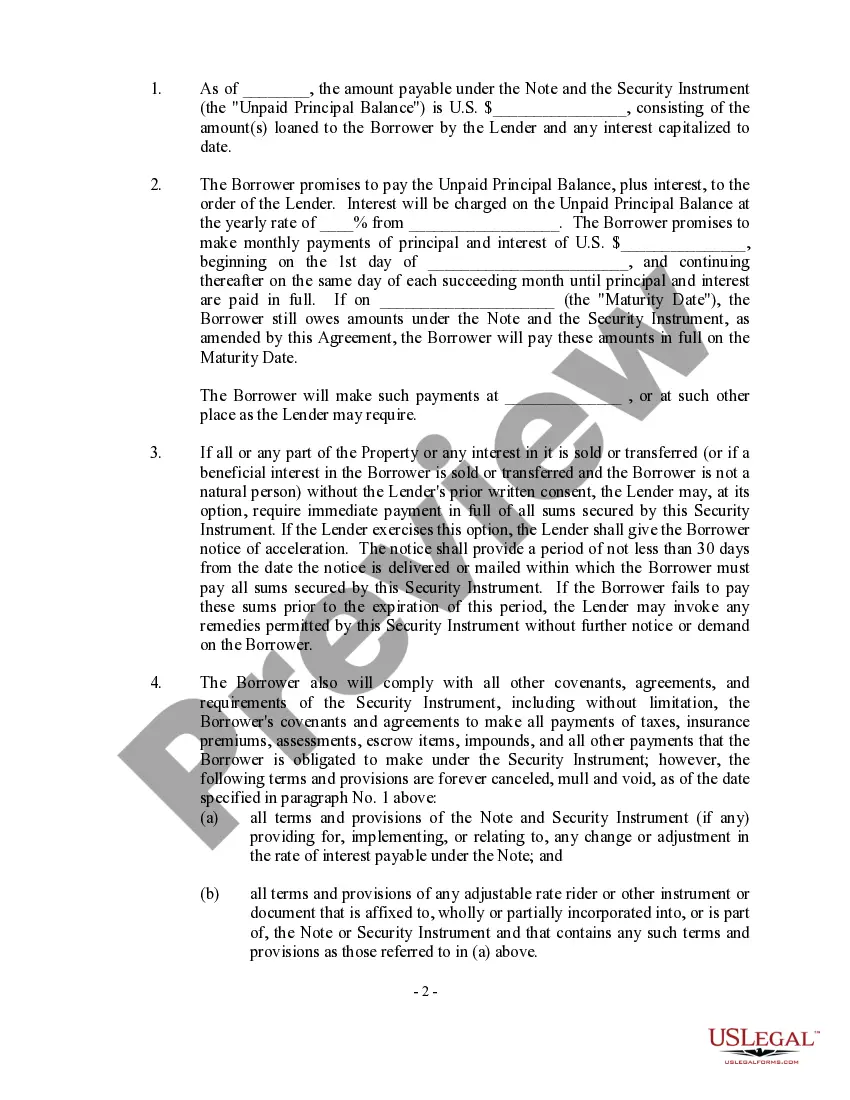

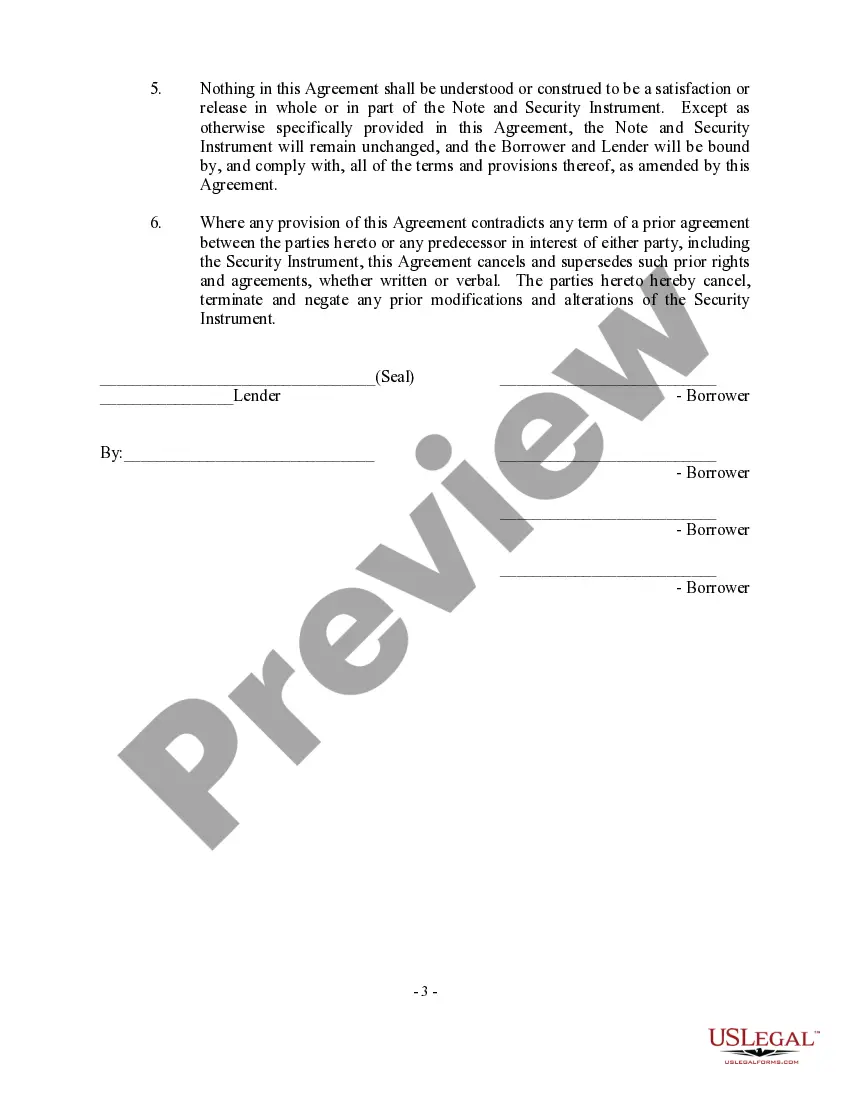

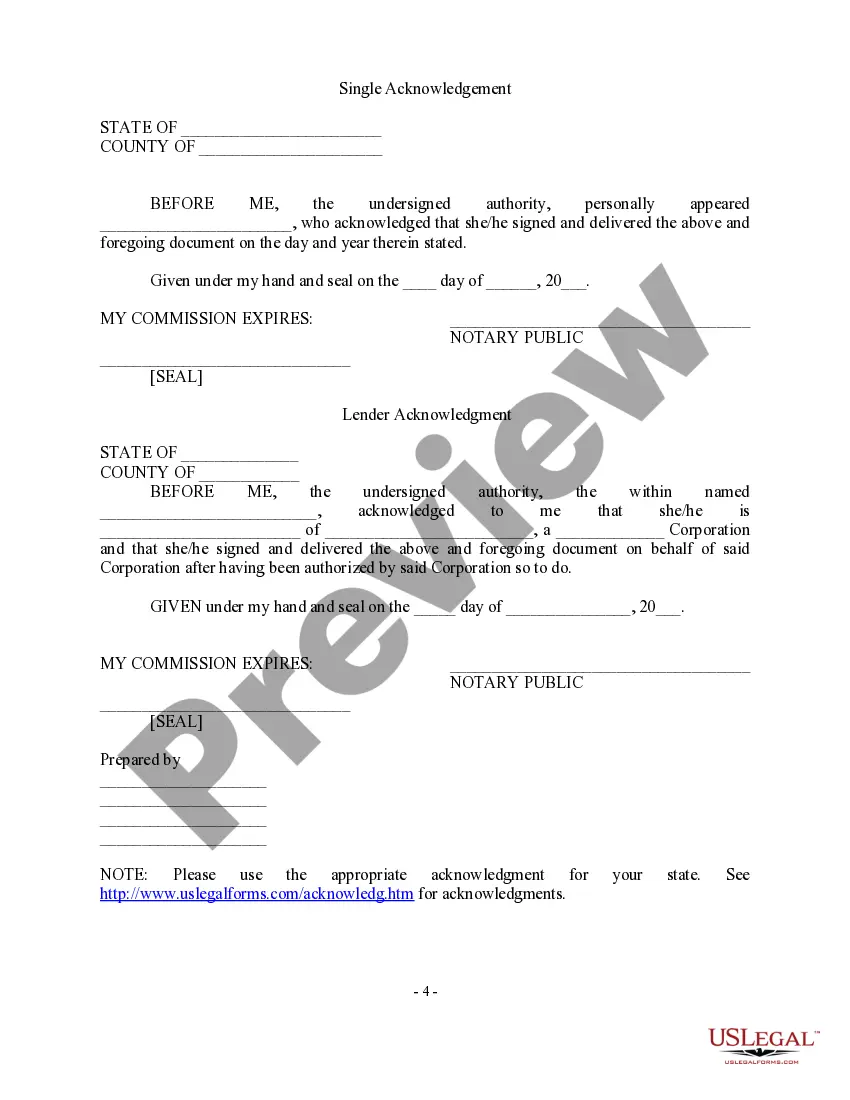

Connecticut Loan Modification Agreement — Multistate is a legal document used in the state of Connecticut to modify the terms of an existing loan agreement between a lender and a borrower. This agreement is designed to help borrowers facing financial difficulties to avoid foreclosure by restructuring their loan to make it more affordable. A Connecticut Loan Modification Agreement — Multistate typically includes various terms and conditions that allow borrowers to change certain aspects of the original loan agreement, such as the interest rate, monthly payments, loan term, or even the principal amount owed. This can help borrowers reduce their financial burden and make their mortgage payments more manageable. There are several types of Connecticut Loan Modification Agreements — Multistate that borrowers can consider based on their specific needs and circumstances: 1. Interest Rate Modification: This type of loan modification agreement allows borrowers to negotiate a lower interest rate, resulting in reduced monthly payments. Lower interest rates can help borrowers save money in the long run. 2. Payment Reduction Agreement: This modification agreement focuses on decreasing the monthly payments by extending the loan term or reducing the principal amount owed. It provides immediate relief to borrowers struggling to meet their current payment obligations. 3. Forbearance Agreement: Temporary financial hardship may be relieved using a forbearance agreement. It allows borrowers to temporarily suspend or reduce their mortgage payments for a specific period, giving them time to recover their financial stability. 4. Principal Reduction Agreement: This type of loan modification involves a reduction in the principal balance owed on the loan. Lenders may agree to forgive a portion of the outstanding amount, which can significantly reduce the borrower's overall debt burden. 5. Combination Modification Agreement: In certain cases, a combination of various modification agreements may be used to provide borrowers with the most suitable solution. This can involve a combination of interest rate reduction, payment reduction, or principal reduction, to create a manageable and customized loan modification plan. It is important to note that each loan modification agreement is unique and tailored to the borrower's specific financial situation. These agreements often require detailed financial information, including income, expenses, and proof of hardship, to support the borrower's request for modification. Overall, a Connecticut Loan Modification Agreement — Multistate aims to provide struggling borrowers with the opportunity to restructure their loan terms and avoid foreclosure. It is advisable for borrowers to consult with legal or financial professionals to ensure they fully understand the terms and implications of the loan modification agreement before entering into one.

Connecticut Loan Modification Agreement - Multistate

Description

How to fill out Connecticut Loan Modification Agreement - Multistate?

Are you within a placement where you need paperwork for either business or specific reasons nearly every day time? There are a lot of legitimate file web templates available online, but getting ones you can trust is not easy. US Legal Forms delivers thousands of form web templates, much like the Connecticut Loan Modification Agreement - Multistate, that happen to be created to fulfill federal and state requirements.

Should you be previously acquainted with US Legal Forms web site and get a free account, simply log in. Afterward, you can acquire the Connecticut Loan Modification Agreement - Multistate format.

Unless you have an account and would like to begin to use US Legal Forms, adopt these measures:

- Find the form you require and ensure it is to the appropriate town/state.

- Take advantage of the Review key to check the shape.

- Read the information to ensure that you have selected the right form.

- If the form is not what you are seeking, take advantage of the Lookup discipline to obtain the form that meets your needs and requirements.

- If you obtain the appropriate form, just click Buy now.

- Choose the costs plan you desire, fill out the desired information to make your bank account, and pay money for the order with your PayPal or credit card.

- Select a hassle-free document structure and acquire your duplicate.

Find every one of the file web templates you may have purchased in the My Forms food list. You can aquire a additional duplicate of Connecticut Loan Modification Agreement - Multistate any time, if needed. Just click the needed form to acquire or produce the file format.

Use US Legal Forms, probably the most substantial collection of legitimate varieties, to save lots of some time and avoid blunders. The assistance delivers appropriately produced legitimate file web templates that you can use for a range of reasons. Create a free account on US Legal Forms and begin generating your way of life a little easier.