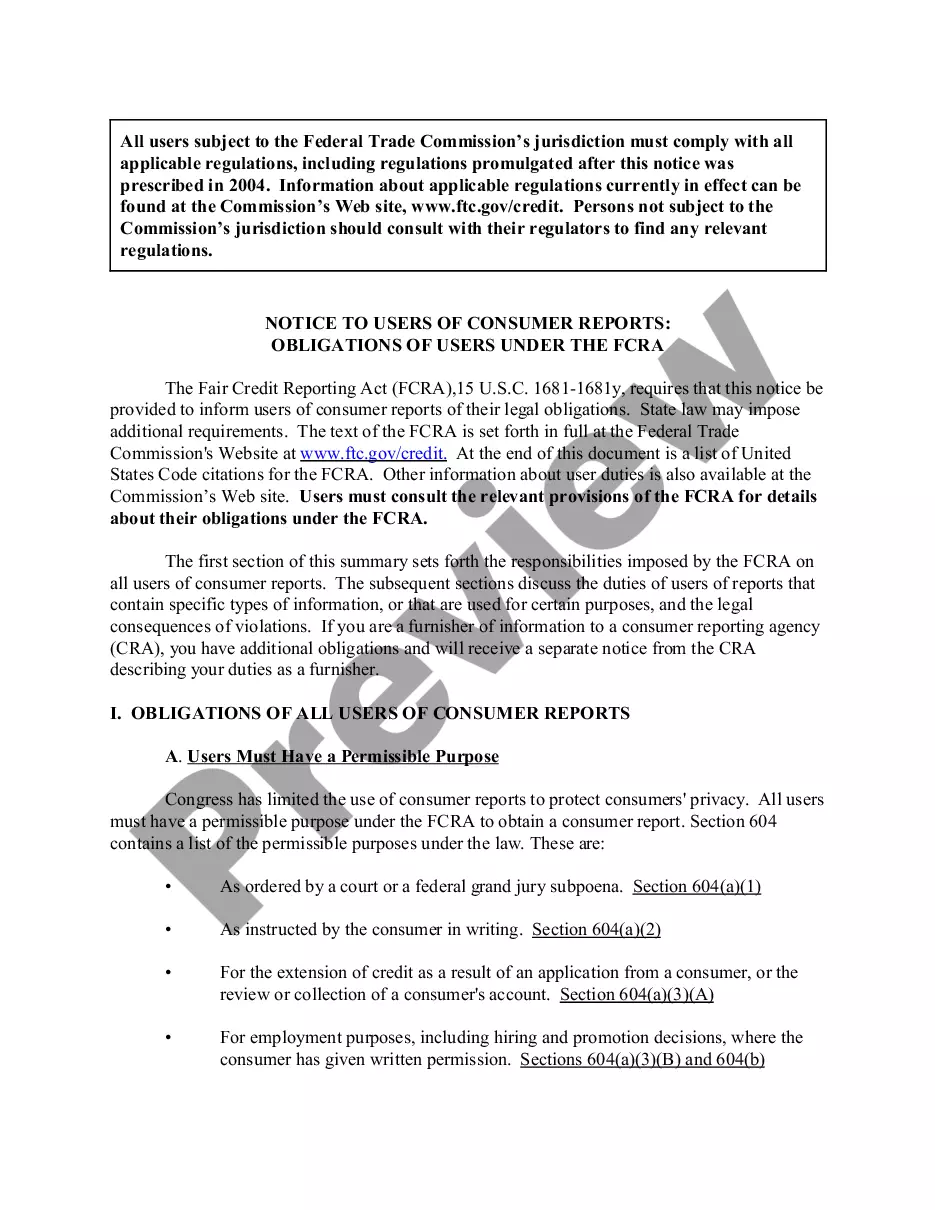

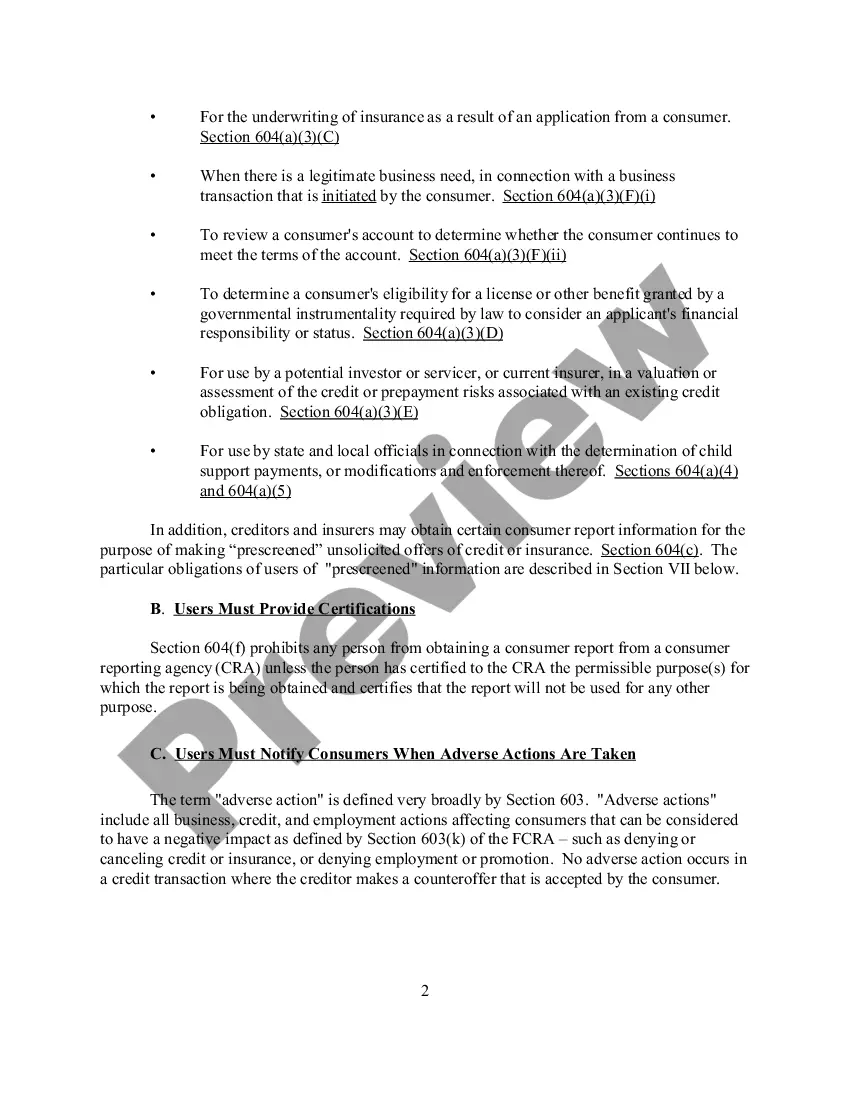

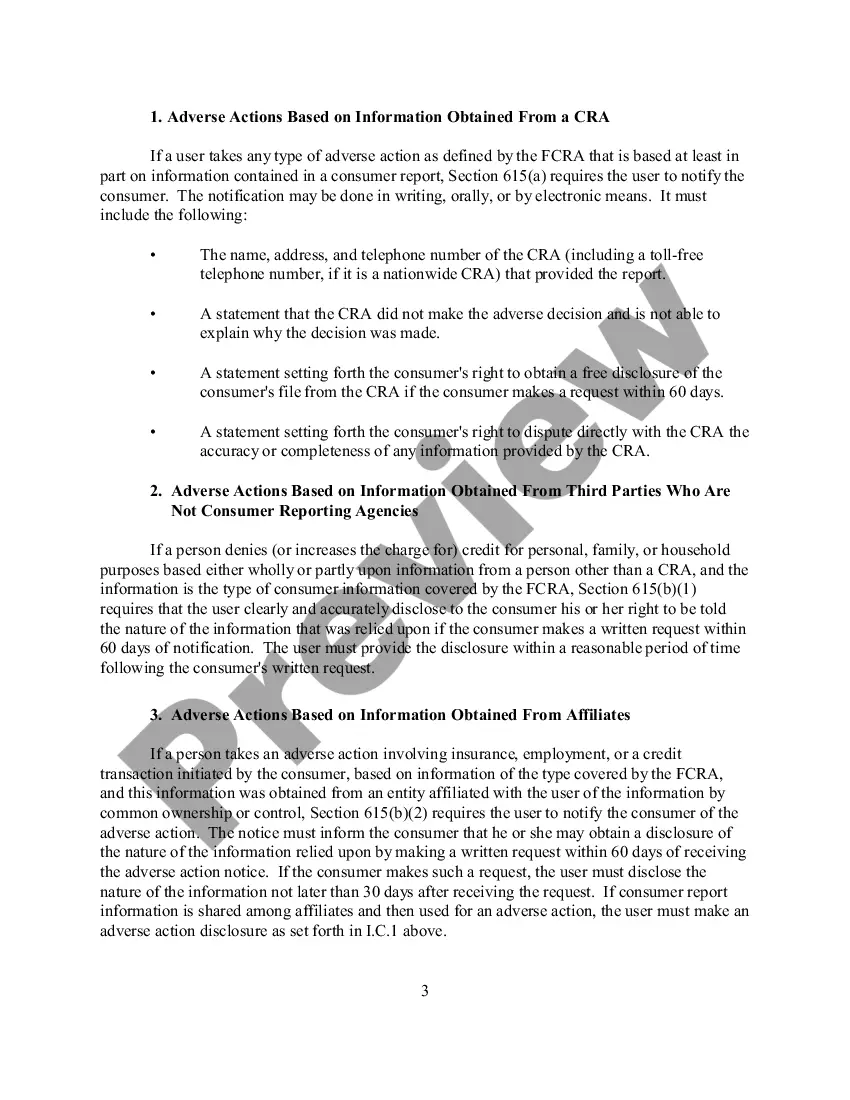

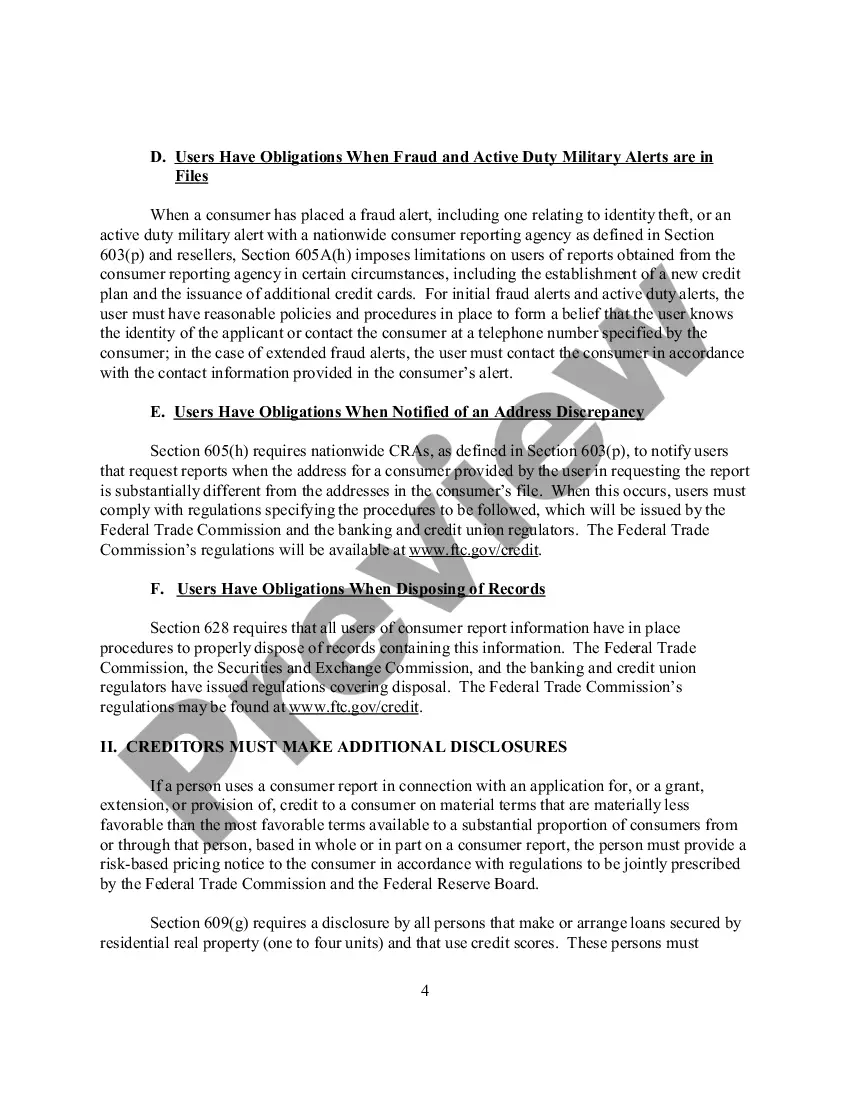

Connecticut Notice to Users of Consumer Reports — Obligations of Users under the FCRA: An Overview The Connecticut Notice to Users of Consumer Reports provides crucial information for individuals and businesses who use consumer reports in the state of Connecticut. This notice highlights the obligations and responsibilities of these users under the Fair Credit Reporting Act (FCRA), a federal law designed to protect consumer rights and promote accuracy, fairness, and privacy of information in consumer reports. Key Keywords: Connecticut, Notice to Users, Consumer Reports, Obligations, FCRA, Fair Credit Reporting Act, User Responsibilities. 1. General Overview of the Connecticut Notice to Users of Consumer Reports: The Connecticut Notice to Users of Consumer Reports aims to educate users about their obligations when obtaining and using consumer reports in compliance with the FCRA. It emphasizes the importance of maintaining the confidentiality of consumer information and ensuring fair and legitimate use of consumer reports. 2. Obligations of Users under the FCRA: The notice outlines the main obligations and responsibilities that users must adhere to when utilizing consumer reports. These obligations include obtaining proper consent, using reports for permissible purposes, notifying consumers about adverse actions, and properly disposing of consumer information to protect against unauthorized access. 3. Types of Users Covered by the Connecticut Notice: The Connecticut Notice applies to various entities that use consumer reports, including employers, landlords, financial institutions, insurance companies, and other businesses that rely on consumer information for decision-making purposes. Each user type has distinct obligations and responsibilities under the FCRA. 4. Employer Obligations: Employers using consumer reports for employment-related purposes must comply with specific guidelines, such as obtaining written consent from applicants and employees, providing pre-adverse action notifications, and offering individuals an opportunity to dispute inaccurate information. 5. Landlord Obligations: Landlords who utilize consumer reports for tenant screening must ensure they comply with the FCRA regulations. This includes obtaining proper consent, providing adverse action notices, and allowing tenants to dispute inaccurate information. 6. Financial Institution Obligations: Financial institutions, such as banks and credit unions, have obligations to protect consumer information they access for credit decisions. They must adhere to strict guidelines concerning consent, permissible purposes, and accurate reporting. 7. Insurance Company Obligations: Insurance companies utilizing consumer reports for underwriting, rating, or claims evaluation purposes need to comply with FCRA guidelines. This includes obtaining consent, providing adverse action notices, and ensuring the accuracy and privacy of consumer data. 8. Business Obligations: Businesses in various industries that use consumer reports for marketing, research, background checks, or other purposes should be aware of their obligations as outlined in the FCRA and the Connecticut Notice. In summary, the Connecticut Notice to Users of Consumer Reports provides a comprehensive overview of the obligations and responsibilities that users must follow under the FCRA. The notice covers different user types, including employers, landlords, financial institutions, insurance companies, and other businesses. By understanding and complying with these obligations, users can protect consumer rights, maintain data accuracy, and promote fair and ethical practices in the use of consumer reports.

Connecticut Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA

Description

How to fill out Connecticut Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA?

Choosing the right legal file format could be a have a problem. Obviously, there are tons of web templates available on the Internet, but how do you get the legal type you will need? Use the US Legal Forms internet site. The assistance provides 1000s of web templates, for example the Connecticut Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA, that you can use for business and private requires. All of the types are examined by experts and fulfill state and federal specifications.

When you are already authorized, log in in your profile and then click the Acquire option to get the Connecticut Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA. Use your profile to look throughout the legal types you have purchased earlier. Proceed to the My Forms tab of your profile and acquire yet another duplicate of your file you will need.

When you are a new user of US Legal Forms, allow me to share basic instructions that you can follow:

- Very first, be sure you have selected the right type for the city/county. You are able to look through the shape using the Preview option and look at the shape outline to make certain it is the best for you.

- In the event the type is not going to fulfill your needs, utilize the Seach industry to discover the appropriate type.

- Once you are positive that the shape is suitable, select the Buy now option to get the type.

- Opt for the prices strategy you want and type in the necessary info. Create your profile and buy an order utilizing your PayPal profile or charge card.

- Opt for the data file formatting and download the legal file format in your system.

- Complete, modify and print out and signal the attained Connecticut Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA.

US Legal Forms will be the largest local library of legal types in which you can find a variety of file web templates. Use the company to download expertly-manufactured papers that follow status specifications.