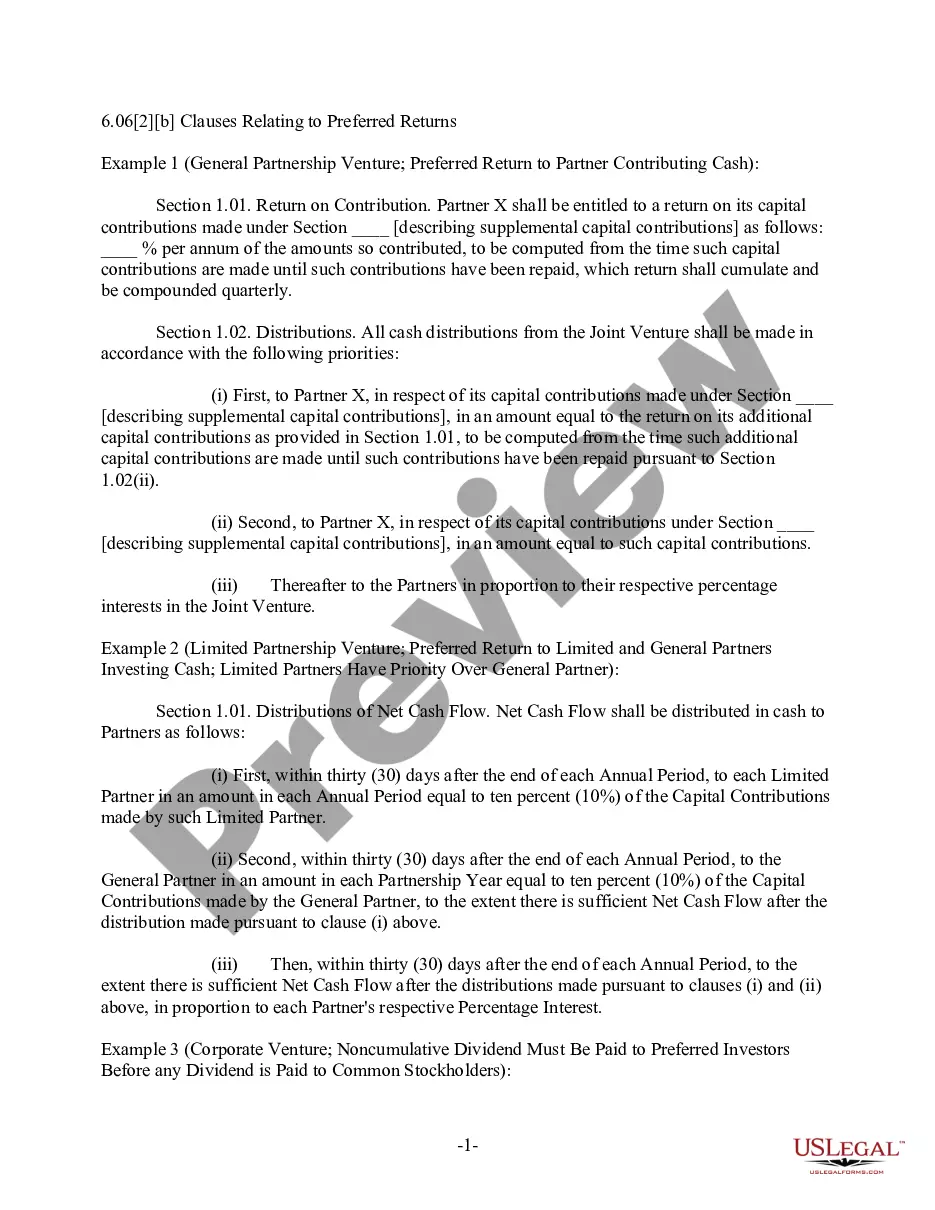

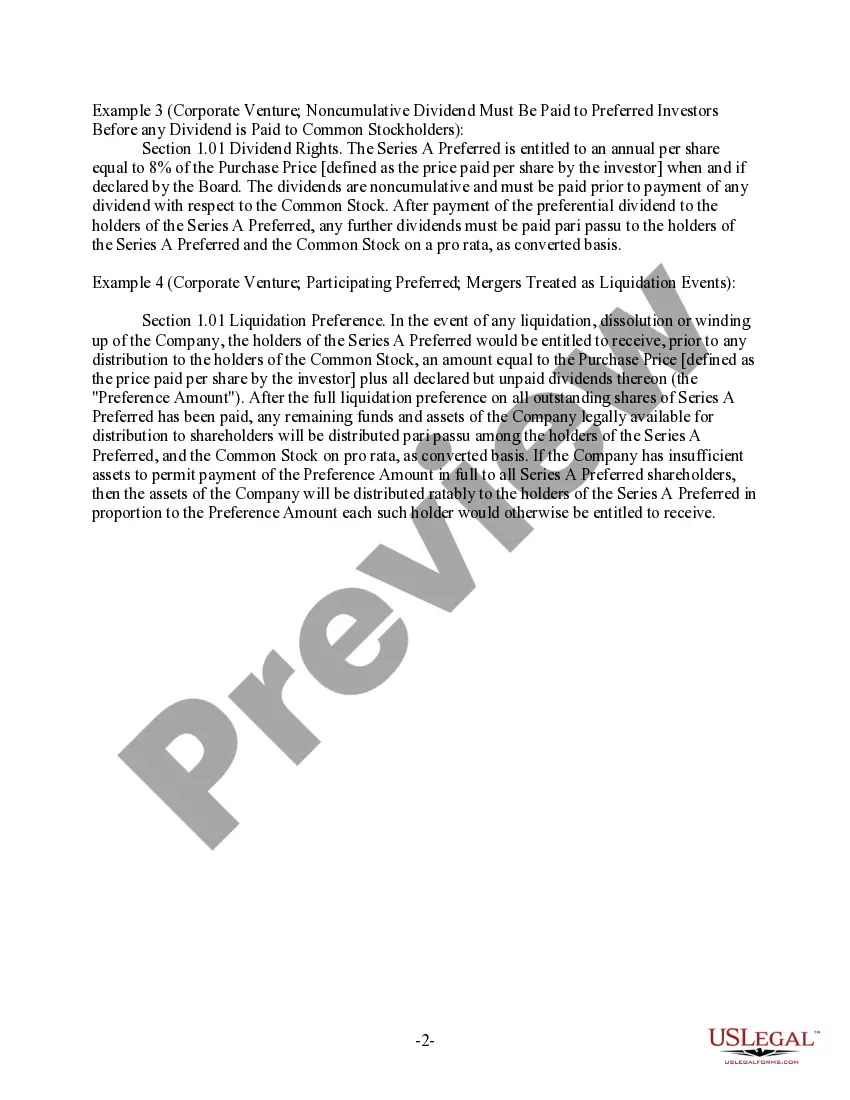

Connecticut Clauses Relating to Preferred Returns: A Detailed Description Preferred returns are an essential aspect of investment agreements, ensuring that certain investors receive their investment profits or returns before others. In Connecticut, the law has established specific clauses relating to preferred returns to protect the rights and interests of investors. These clauses provide clarity on how preferred returns should be calculated, distributed, and prioritized in various investment scenarios. Connecticut has various types of clauses relating to preferred returns, including: 1. Fixed Preferred Return Clause: This type of clause sets a specific percentage rate of return that must be distributed to preferred investors. For example, if the fixed preferred return is set at 8%, investors with this priority will receive the calculated percentage return on their investments before others receive any profits. 2. Cumulative Preferred Return Clause: Under this clause, preferred investors are entitled to receive their returns cumulatively over multiple periods. If the investment does not yield the preferred return in a particular period, it will accumulate and be paid out in subsequent periods until the cumulative amount is fulfilled. 3. Non-Cumulative Preferred Return Clause: In contrast to the cumulative preferred return clause, this clause does not accumulate unpaid returns over multiple periods. If the preferred return is not met in a specific period, it is not carried forward, and the preferred investors will only be entitled to the return amount for that period. 4. Preferred Return Clawback Clause: This type of clause allows the general partners or fund managers to reclaim previously distributed preferred returns in certain situations, such as when performance fees have been overpaid or when a project's overall returns fail to meet predefined benchmarks. The Connecticut clauses relating to preferred returns outline the rights and obligations of both investors and fund managers, ensuring a fair and transparent distribution of investment profits. Investors can rely on these clauses to ascertain their preferred status, prioritize returns, and protect their interests from potential risks or unfavorable circumstances. By incorporating these preferred return clauses into investment agreements, Connecticut aims to provide legal clarity, minimize disputes, and foster a more secure investment environment. It is crucial for investors and asset managers to consult legal experts and thoroughly understand these clauses to effectively structure investment deals and maximize returns while adhering to Connecticut laws and regulations. Keywords: Connecticut, clauses, preferred returns, fixed preferred return, cumulative preferred return, non-cumulative preferred return, preferred return clawback, investment agreements, investors, rights, interests, distribution, prioritization, legal clarity, disputes, investment environment, asset managers, laws, regulations.

Connecticut Clauses Relating to Preferred Returns

Description

How to fill out Connecticut Clauses Relating To Preferred Returns?

Are you presently in the position where you require papers for possibly company or personal uses almost every time? There are tons of authorized document layouts accessible on the Internet, but getting ones you can rely is not simple. US Legal Forms offers thousands of type layouts, much like the Connecticut Clauses Relating to Preferred Returns, which are composed to satisfy state and federal demands.

Should you be already knowledgeable about US Legal Forms web site and possess a free account, merely log in. Following that, it is possible to obtain the Connecticut Clauses Relating to Preferred Returns template.

Should you not have an bank account and need to begin using US Legal Forms, adopt these measures:

- Obtain the type you want and make sure it is for the proper town/state.

- Make use of the Review option to analyze the form.

- Look at the outline to actually have selected the appropriate type.

- In the event the type is not what you are looking for, take advantage of the Search discipline to obtain the type that suits you and demands.

- Once you find the proper type, simply click Get now.

- Opt for the prices program you need, complete the required information to generate your bank account, and pay money for the transaction utilizing your PayPal or charge card.

- Choose a hassle-free paper structure and obtain your copy.

Get all of the document layouts you possess bought in the My Forms menus. You can obtain a extra copy of Connecticut Clauses Relating to Preferred Returns anytime, if necessary. Just go through the essential type to obtain or print out the document template.

Use US Legal Forms, probably the most considerable variety of authorized varieties, to save some time and stay away from mistakes. The service offers skillfully made authorized document layouts that can be used for a selection of uses. Generate a free account on US Legal Forms and begin generating your daily life easier.