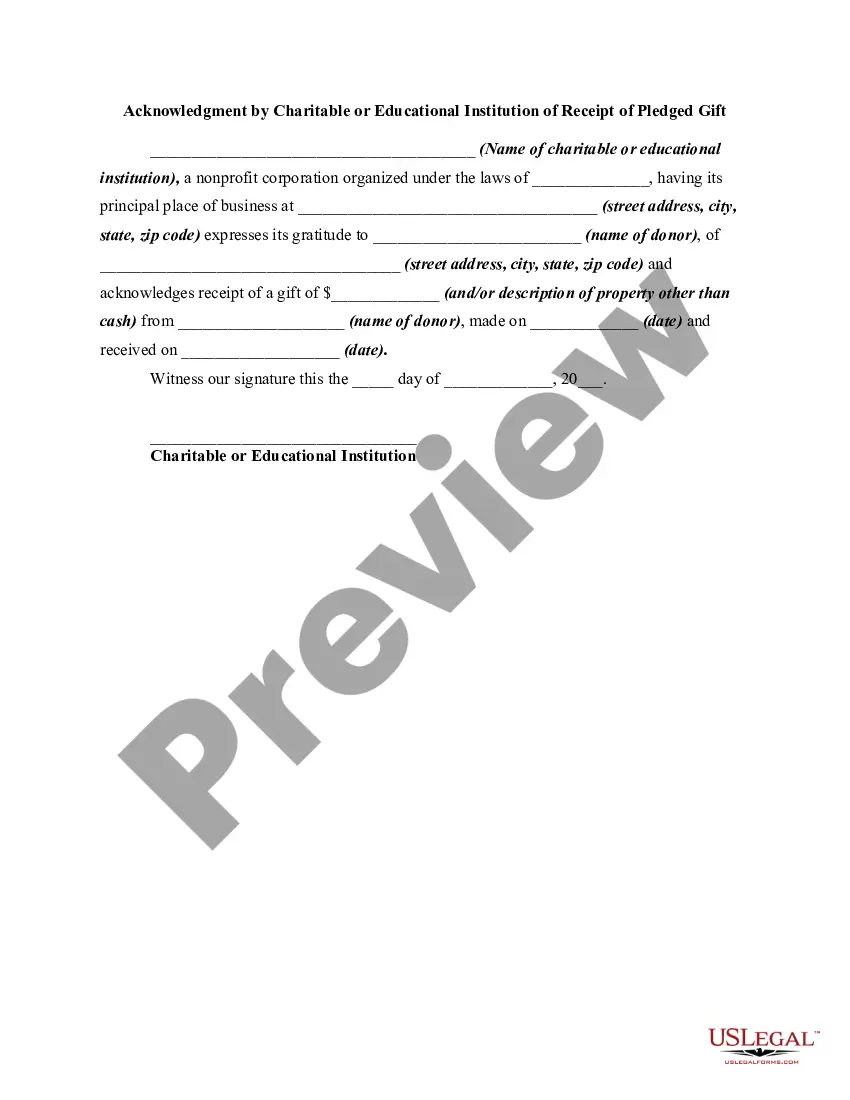

District of Columbia Acknowledgment by Charitable or Educational Institution of Receipt of Gift

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Acknowledgment By Charitable Or Educational Institution Of Receipt Of Gift?

You can spend hours online attempting to locate the legal document template that meets the state and federal requirements you desire. US Legal Forms offers a vast array of legal forms that are reviewed by experts.

You can obtain or print the District of Columbia Acknowledgment by Charitable or Educational Institution of Receipt of Gift from the service. If you already have a US Legal Forms account, you can Log In and click the Download button.

After that, you can complete, modify, print, or sign the District of Columbia Acknowledgment by Charitable or Educational Institution of Receipt of Gift. Every legal document template you purchase is yours indefinitely. To obtain an additional copy of the purchased form, go to the My documents tab and click the corresponding button.

Select the format of the document and download it to your device. Make adjustments to your document if necessary. You can complete, edit, sign, and print the District of Columbia Acknowledgment by Charitable or Educational Institution of Receipt of Gift. Download and print numerous document templates using the US Legal Forms website, which provides the largest selection of legal forms. Utilize professional and state-specific templates to address your business or personal needs.

- If you are using the US Legal Forms website for the first time, follow the simple instructions below.

- First, ensure that you have selected the correct document template for your desired region/city. Check the form description to confirm you have chosen the appropriate type.

- If available, utilize the Preview button to review the document template as well.

- If you want to find another variation of the form, make use of the Search field to locate the template that meets your needs.

- Once you have found the template you want, click Purchase now to proceed.

- Choose the pricing plan you prefer, enter your details, and register for an account on US Legal Forms.

- Complete the transaction. You can use your credit card or PayPal account to purchase the legal form.

Form popularity

FAQ

To write a receipt for a charitable donation, begin with your organization's name and contact information. Next, include the donor's name, the date of the donation, and a description of the gift. Make sure to state that no goods or services were exchanged, as this aligns with the District of Columbia Acknowledgment by Charitable or Educational Institution of Receipt of Gift guidelines. Our platform offers templates that simplify this process, ensuring you provide clear and compliant receipts.

To show proof of a charitable donation, you need a receipt from the charitable organization. This receipt must include the organization's name, date of the donation, and the amount donated. Additionally, a District of Columbia Acknowledgment by Charitable or Educational Institution of Receipt of Gift can serve as valid proof for tax purposes. Using our platform, you can easily generate the necessary documentation to ensure compliance and proper acknowledgment.

To acknowledge receipt of a donation, send a personalized letter or email to the donor, thanking them for their generosity. Include specific details about the donation, such as the amount and date, along with a note on how their contribution will be used. This practice not only complies with the District of Columbia Acknowledgment by Charitable or Educational Institution of Receipt of Gift but also fosters a strong relationship with your supporters. For seamless management of these acknowledgments, consider using the uslegalforms platform, which provides templates and guidance tailored to charitable institutions.

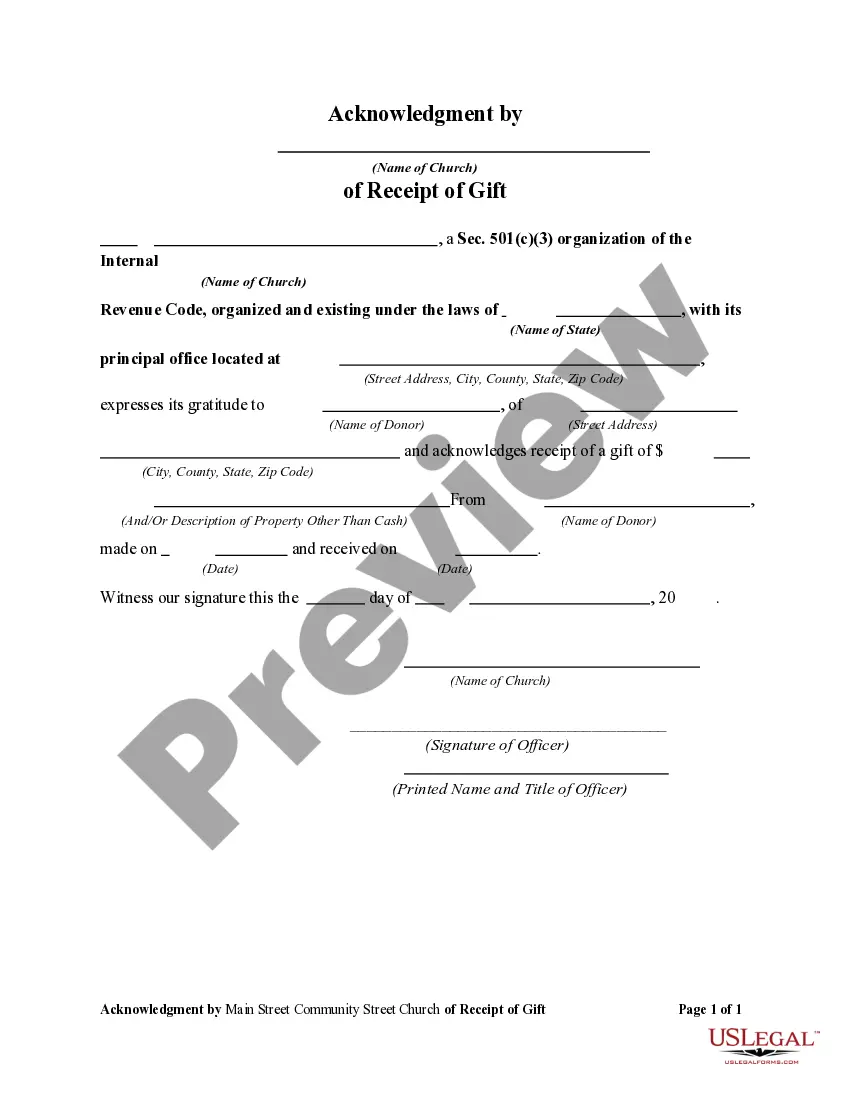

A contemporaneous written acknowledgment of a charitable gift must include the donor's name, the date of the contribution, and a detailed description of the gift. If goods or services were provided in exchange, this must also be stated. Adhering to the standards for District of Columbia Acknowledgment by Charitable or Educational Institution of Receipt of Gift helps maintain transparency and supports the donor's tax deduction claims.

An example of a written acknowledgment for a charitable contribution might include a letter stating, 'Thank you for your generous donation of $500 on March 1, 2023, to our educational program. No goods or services were exchanged for this donation.' Such a clear and concise acknowledgment aligns with the District of Columbia Acknowledgment by Charitable or Educational Institution of Receipt of Gift requirements, ensuring donors feel appreciated and informed.

To give a receipt for a charitable donation, ensure you provide a written acknowledgment that includes the donor's name, the date of the donation, and a description of the gift. This acknowledgment should clearly state whether the donor received any goods or services in exchange for their contribution. Following the guidelines for District of Columbia Acknowledgment by Charitable or Educational Institution of Receipt of Gift is essential for compliance and donor tax purposes.

It is rude to not thank the gift giver after receiving a gift, but it sounds like their children don't know this because they haven't been taught properly. If you stop giving the children gifts, they'll have no idea why you did it, which will defeat the purpose.

You can acknowledge their generosity in much the same way you thank your other donors?with just a few differences. Thank the donor who recommended the grant, not Fidelity Charitable. ... Eliminate all references to the gift being tax-deductible. ... Use a thank-you as an opportunity to drive future engagement.

Tip #1: Although the IRS doesn't require acknowledgment letters to be sent for gifts under $250, it's a good rule of thumb to express thanks for every gift, regardless of its size.

Some experts recommend that your acknowledgment read something like, ?Thank you for recommending the generous grant of $500.00 that we received on <date> through your donor advised fund at Fidelity Charitable.?