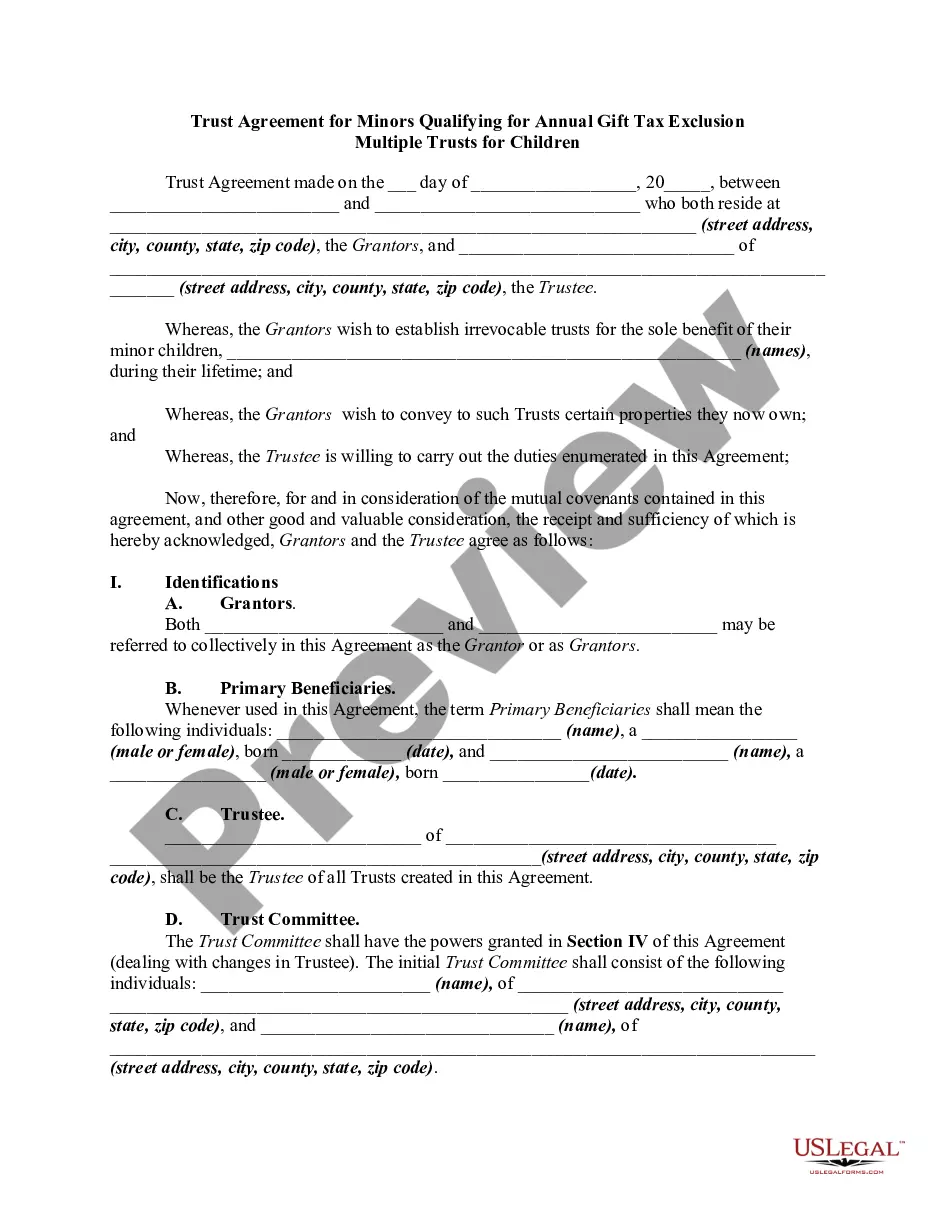

This form set up what is known as present interest trusts, with the intention of meeting the requirements of Section 2503(c) of the Internal Revenue Code.

The District of Columbia Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children is a legal document that allows individuals to establish separate trusts for multiple minor beneficiaries in order to take advantage of the annual gift tax exclusion. This arrangement provides a tax-efficient way of transferring assets to children or grandchildren while minimizing the tax burden. The primary purpose of the District of Columbia Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children is to create separate trusts for each child or grandchild, thereby allowing the granter to make annual gifts to each trust up to the maximum gift tax exclusion amount without incurring gift taxes. By setting up multiple trusts, the granter can distribute assets among beneficiaries while ensuring each trust remains within the annual gift tax exclusion limit. This trust agreement is particularly beneficial for families with multiple children or grandchildren, as it allows for the customization of each trust to suit the unique needs and circumstances of each beneficiary. It provides flexibility in appointing trustees, determining the distribution terms, and specifying the use of trust assets. There are different types of District of Columbia Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children, which include: 1. Individual Trusts: Each child or grandchild has their own individual trust established under the agreement. This provides the highest level of personalization and allows for tailoring the distribution terms to match the specific needs of each beneficiary. 2. Pooled Trusts: Instead of separate trusts for each beneficiary, multiple children or grandchildren can be grouped into a single trust. This option is suitable when the granter prefers a more streamlined approach and wishes to simplify the administration and management of the trusts. 3. Generation-Skipping Trusts: These trusts are designed to skip a generation, typically to benefit grandchildren. By using this type of trust, the assets can be transferred directly to grandchildren, avoiding potential estate taxes on the assets passing through the granter's children. In summary, the District of Columbia Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children is a versatile tool for individuals seeking to establish separate trusts for each minor beneficiary while utilizing the annual gift tax exclusion. This arrangement allows for customized planning and efficient wealth transfer to children or grandchildren. Whether through individual, pooled, or generation-skipping trusts, this trust agreement offers flexibility and tax benefits to families looking to preserve their wealth for future generations.The District of Columbia Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children is a legal document that allows individuals to establish separate trusts for multiple minor beneficiaries in order to take advantage of the annual gift tax exclusion. This arrangement provides a tax-efficient way of transferring assets to children or grandchildren while minimizing the tax burden. The primary purpose of the District of Columbia Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children is to create separate trusts for each child or grandchild, thereby allowing the granter to make annual gifts to each trust up to the maximum gift tax exclusion amount without incurring gift taxes. By setting up multiple trusts, the granter can distribute assets among beneficiaries while ensuring each trust remains within the annual gift tax exclusion limit. This trust agreement is particularly beneficial for families with multiple children or grandchildren, as it allows for the customization of each trust to suit the unique needs and circumstances of each beneficiary. It provides flexibility in appointing trustees, determining the distribution terms, and specifying the use of trust assets. There are different types of District of Columbia Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children, which include: 1. Individual Trusts: Each child or grandchild has their own individual trust established under the agreement. This provides the highest level of personalization and allows for tailoring the distribution terms to match the specific needs of each beneficiary. 2. Pooled Trusts: Instead of separate trusts for each beneficiary, multiple children or grandchildren can be grouped into a single trust. This option is suitable when the granter prefers a more streamlined approach and wishes to simplify the administration and management of the trusts. 3. Generation-Skipping Trusts: These trusts are designed to skip a generation, typically to benefit grandchildren. By using this type of trust, the assets can be transferred directly to grandchildren, avoiding potential estate taxes on the assets passing through the granter's children. In summary, the District of Columbia Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children is a versatile tool for individuals seeking to establish separate trusts for each minor beneficiary while utilizing the annual gift tax exclusion. This arrangement allows for customized planning and efficient wealth transfer to children or grandchildren. Whether through individual, pooled, or generation-skipping trusts, this trust agreement offers flexibility and tax benefits to families looking to preserve their wealth for future generations.