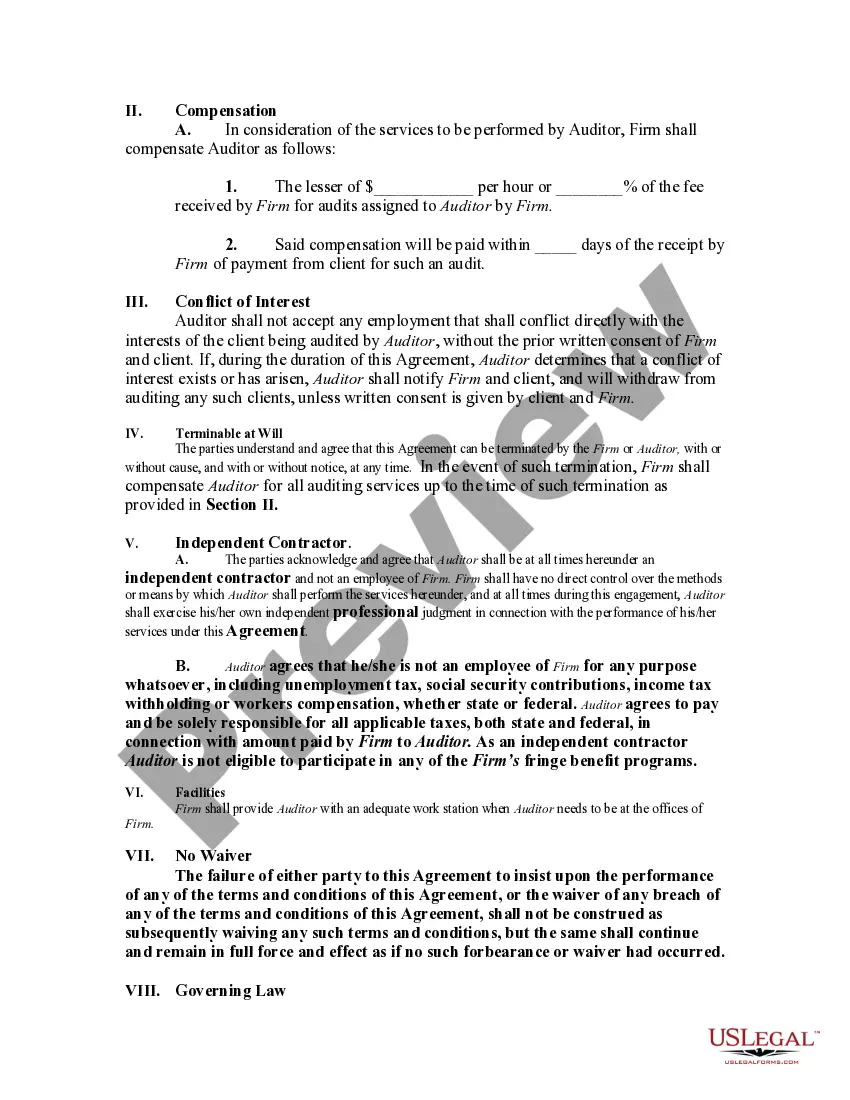

Although no definite rule exists for determining whether one is an independent contractor or an employee, certain indicia of the status of an independent contractor are recognized, and the insertion of provisions embodying these indicia in the contract will help to insure that the relationship reflects the intention of the parties. These indicia generally relate to the basic issue of control. The general test of what constitutes an independent contractor relationship involves which party has the right to direct what is to be done, and how and when. Another important test involves the method of payment of the contractor.

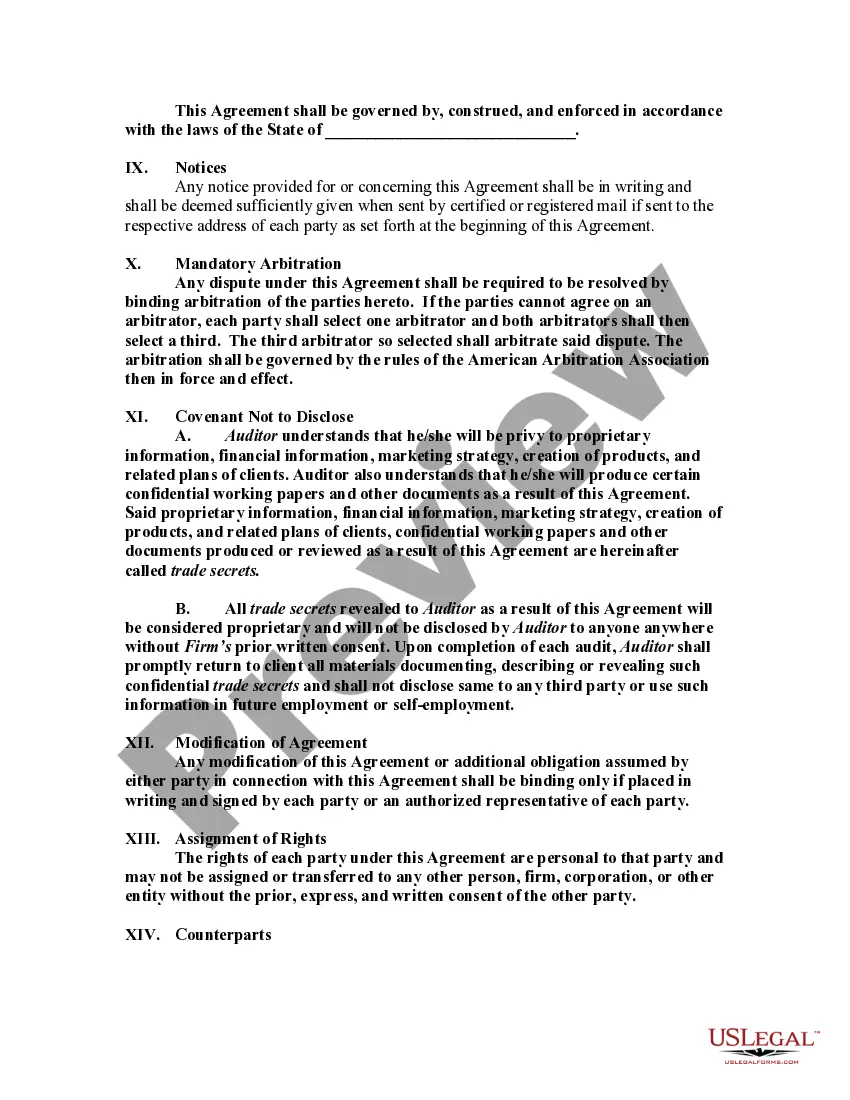

Title: District of Columbia Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor Keywords: District of Columbia, agreement, accounting firm, auditor, self-employed, independent contractor Introduction: The District of Columbia Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor is a legal document that outlines the terms and conditions between an accounting firm and an auditor who will be engaged as a self-employed independent contractor. This agreement is specifically tailored to comply with the laws and regulations in the District of Columbia. It ensures a mutual understanding of the roles, responsibilities, and expectations of both parties involved. Types of District of Columbia Agreements by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: 1. General District of Columbia Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: This comprehensive agreement covers all essential clauses and elements required to establish an employer-auditor relationship in the District of Columbia. It includes provisions related to confidentiality, intellectual property, compensation, termination, non-compete, and dispute resolution, among others. 2. Non-Disclosure District of Columbia Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: This specific agreement focuses on maintaining strict confidentiality and protecting sensitive financial information. It enforces stricter non-disclosure obligations on the auditor to safeguard the accounting firm's proprietary data. It can be used when auditors will have access to highly confidential client data. 3. Project-Specific District of Columbia Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: In cases where the accounting firm requires an auditor for a specific project or engagement, this agreement is suitable. It outlines the project scope, deliverables, timeline, and compensation terms unique to the engagement. It allows both parties to define the project parameters while still adhering to relevant District of Columbia regulations. 4. Scope of Work District of Columbia Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: This agreement provides a detailed description of the auditor's responsibilities and scope of work. It specifies the services to be rendered, such as financial statement preparation, auditing, accounting system evaluations, or tax compliance. It is used when specific services need to be defined accurately to avoid misunderstandings. Conclusion: The District of Columbia Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor is a vital legal document that ensures a clear understanding between an accounting firm and an auditor. It establishes the terms and conditions governing their professional relationship, providing protection and clarity for both parties. By utilizing specific types of agreements, accounting firms can tailor the contract to their unique requirements while complying with District of Columbia laws and regulations.Title: District of Columbia Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor Keywords: District of Columbia, agreement, accounting firm, auditor, self-employed, independent contractor Introduction: The District of Columbia Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor is a legal document that outlines the terms and conditions between an accounting firm and an auditor who will be engaged as a self-employed independent contractor. This agreement is specifically tailored to comply with the laws and regulations in the District of Columbia. It ensures a mutual understanding of the roles, responsibilities, and expectations of both parties involved. Types of District of Columbia Agreements by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: 1. General District of Columbia Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: This comprehensive agreement covers all essential clauses and elements required to establish an employer-auditor relationship in the District of Columbia. It includes provisions related to confidentiality, intellectual property, compensation, termination, non-compete, and dispute resolution, among others. 2. Non-Disclosure District of Columbia Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: This specific agreement focuses on maintaining strict confidentiality and protecting sensitive financial information. It enforces stricter non-disclosure obligations on the auditor to safeguard the accounting firm's proprietary data. It can be used when auditors will have access to highly confidential client data. 3. Project-Specific District of Columbia Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: In cases where the accounting firm requires an auditor for a specific project or engagement, this agreement is suitable. It outlines the project scope, deliverables, timeline, and compensation terms unique to the engagement. It allows both parties to define the project parameters while still adhering to relevant District of Columbia regulations. 4. Scope of Work District of Columbia Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: This agreement provides a detailed description of the auditor's responsibilities and scope of work. It specifies the services to be rendered, such as financial statement preparation, auditing, accounting system evaluations, or tax compliance. It is used when specific services need to be defined accurately to avoid misunderstandings. Conclusion: The District of Columbia Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor is a vital legal document that ensures a clear understanding between an accounting firm and an auditor. It establishes the terms and conditions governing their professional relationship, providing protection and clarity for both parties. By utilizing specific types of agreements, accounting firms can tailor the contract to their unique requirements while complying with District of Columbia laws and regulations.