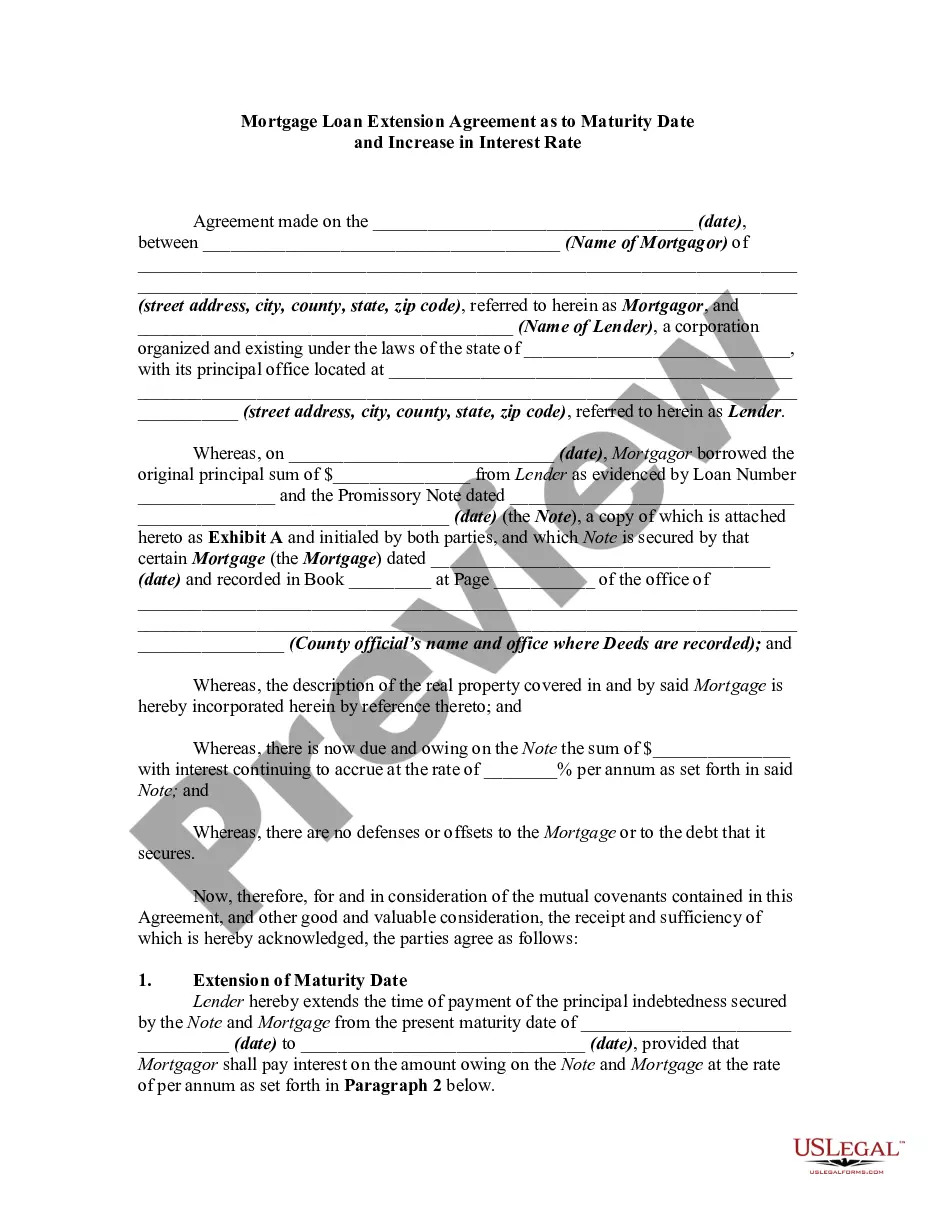

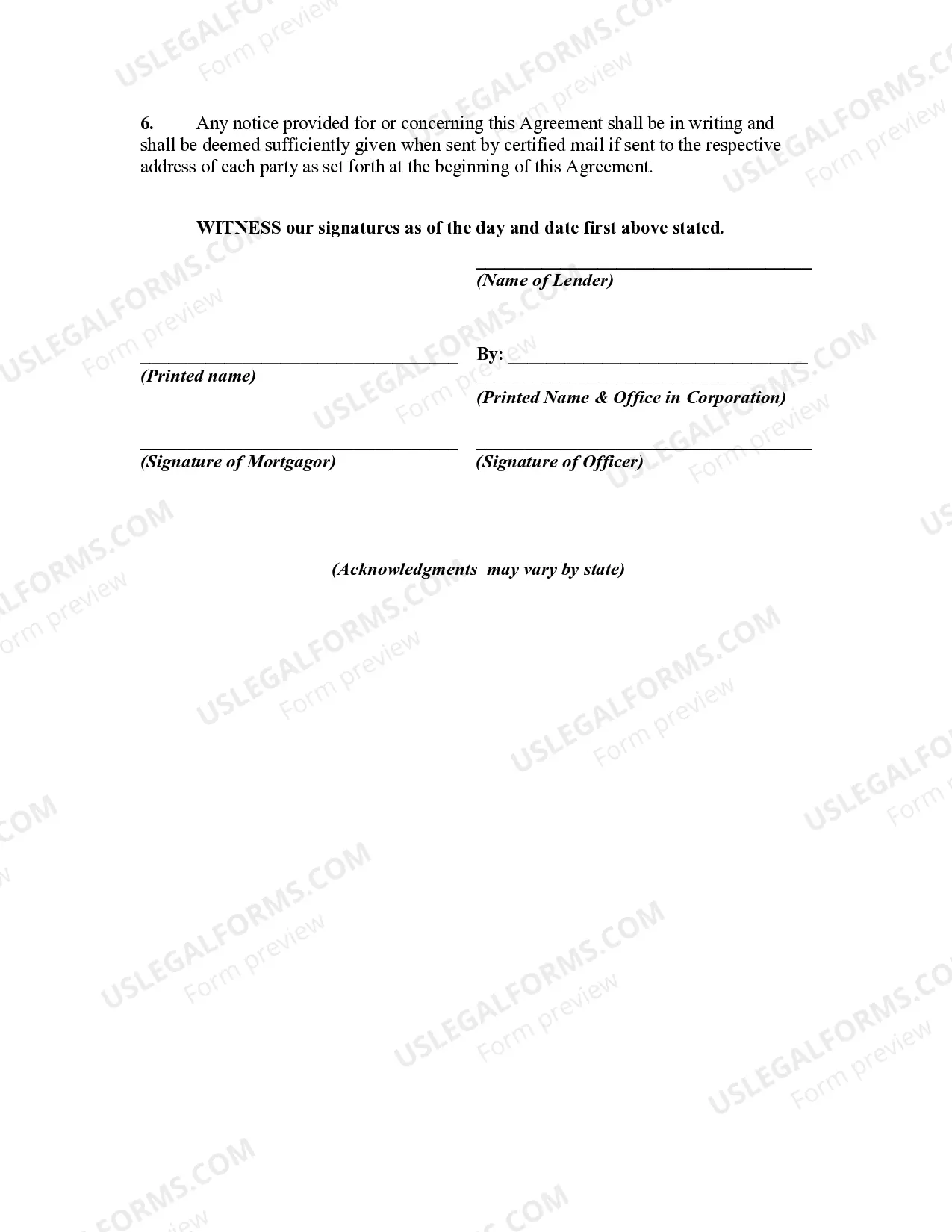

An agreement modifying a loan agreement and mortgage should be signed by both parties to the transaction and recorded in the office of the register of deeds and mortgages where the original mortgage was recorded. Such a modification or extension is contractual in nature and must be supported by consideration. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

District of Columbia Mortgage Loan Extension Agreement as to Maturity Date and Increase in Interest Rate refers to a legal document that allows borrowers in the District of Columbia to extend the maturity date of their mortgage loan while also potentially increasing their interest rate. This agreement is typically entered into when borrowers are unable to repay their mortgage loan within the originally agreed upon timeline. The extension agreement is a common solution for borrowers who are facing financial hardship or are unable to sell their property to repay the loan. By extending the maturity date, borrowers can buy themselves more time to meet their repayment obligations. In addition to extending the maturity date, this agreement may also allow for an increase in the interest rate of the mortgage loan. The interest rate is typically increased in order to compensate the lender for the additional risk and extended lending period. The specific terms and conditions of the interest rate increase are negotiable between the borrower and lender. Different types of District of Columbia Mortgage Loan Extension Agreements as to Maturity Date and Increase in Interest Rate may include: 1. Fixed-rate extension agreement: This type of agreement stipulates a fixed interest rate increase for the extended mortgage loan period. The borrower and lender agree upon a specific increased interest rate, which remains unchanged throughout the extension period. 2. Adjustable-rate extension agreement: In this agreement, the increased interest rate is subject to adjustment based on market conditions. The interest rate may be tied to an index, such as the prime rate, and fluctuate periodically over the extended loan term. 3. Step-up extension agreement: This type of extension agreement involves gradually increasing the interest rate over the extended period. The borrower and lender agree upon predetermined increments of interest rate increases at specific intervals, providing the borrower with a gradual adjustment period. 4. Balloon payment extension agreement: Sometimes, a borrower might agree to extend the maturity date but include a provision for a larger final payment known as a balloon payment. This means that the borrower will continue making regular payments at the existing interest rate during the extension period but will be required to pay off the remaining balance in a lump sum at the end of the extended term. It is important for both borrowers and lenders to carefully review and understand the terms and conditions of the District of Columbia Mortgage Loan Extension Agreement as to Maturity Date and Increase in Interest Rate before entering into the agreement. Seeking legal advice is highly recommended ensuring compliance with relevant laws and regulations governing mortgage loans in the District of Columbia.District of Columbia Mortgage Loan Extension Agreement as to Maturity Date and Increase in Interest Rate refers to a legal document that allows borrowers in the District of Columbia to extend the maturity date of their mortgage loan while also potentially increasing their interest rate. This agreement is typically entered into when borrowers are unable to repay their mortgage loan within the originally agreed upon timeline. The extension agreement is a common solution for borrowers who are facing financial hardship or are unable to sell their property to repay the loan. By extending the maturity date, borrowers can buy themselves more time to meet their repayment obligations. In addition to extending the maturity date, this agreement may also allow for an increase in the interest rate of the mortgage loan. The interest rate is typically increased in order to compensate the lender for the additional risk and extended lending period. The specific terms and conditions of the interest rate increase are negotiable between the borrower and lender. Different types of District of Columbia Mortgage Loan Extension Agreements as to Maturity Date and Increase in Interest Rate may include: 1. Fixed-rate extension agreement: This type of agreement stipulates a fixed interest rate increase for the extended mortgage loan period. The borrower and lender agree upon a specific increased interest rate, which remains unchanged throughout the extension period. 2. Adjustable-rate extension agreement: In this agreement, the increased interest rate is subject to adjustment based on market conditions. The interest rate may be tied to an index, such as the prime rate, and fluctuate periodically over the extended loan term. 3. Step-up extension agreement: This type of extension agreement involves gradually increasing the interest rate over the extended period. The borrower and lender agree upon predetermined increments of interest rate increases at specific intervals, providing the borrower with a gradual adjustment period. 4. Balloon payment extension agreement: Sometimes, a borrower might agree to extend the maturity date but include a provision for a larger final payment known as a balloon payment. This means that the borrower will continue making regular payments at the existing interest rate during the extension period but will be required to pay off the remaining balance in a lump sum at the end of the extended term. It is important for both borrowers and lenders to carefully review and understand the terms and conditions of the District of Columbia Mortgage Loan Extension Agreement as to Maturity Date and Increase in Interest Rate before entering into the agreement. Seeking legal advice is highly recommended ensuring compliance with relevant laws and regulations governing mortgage loans in the District of Columbia.