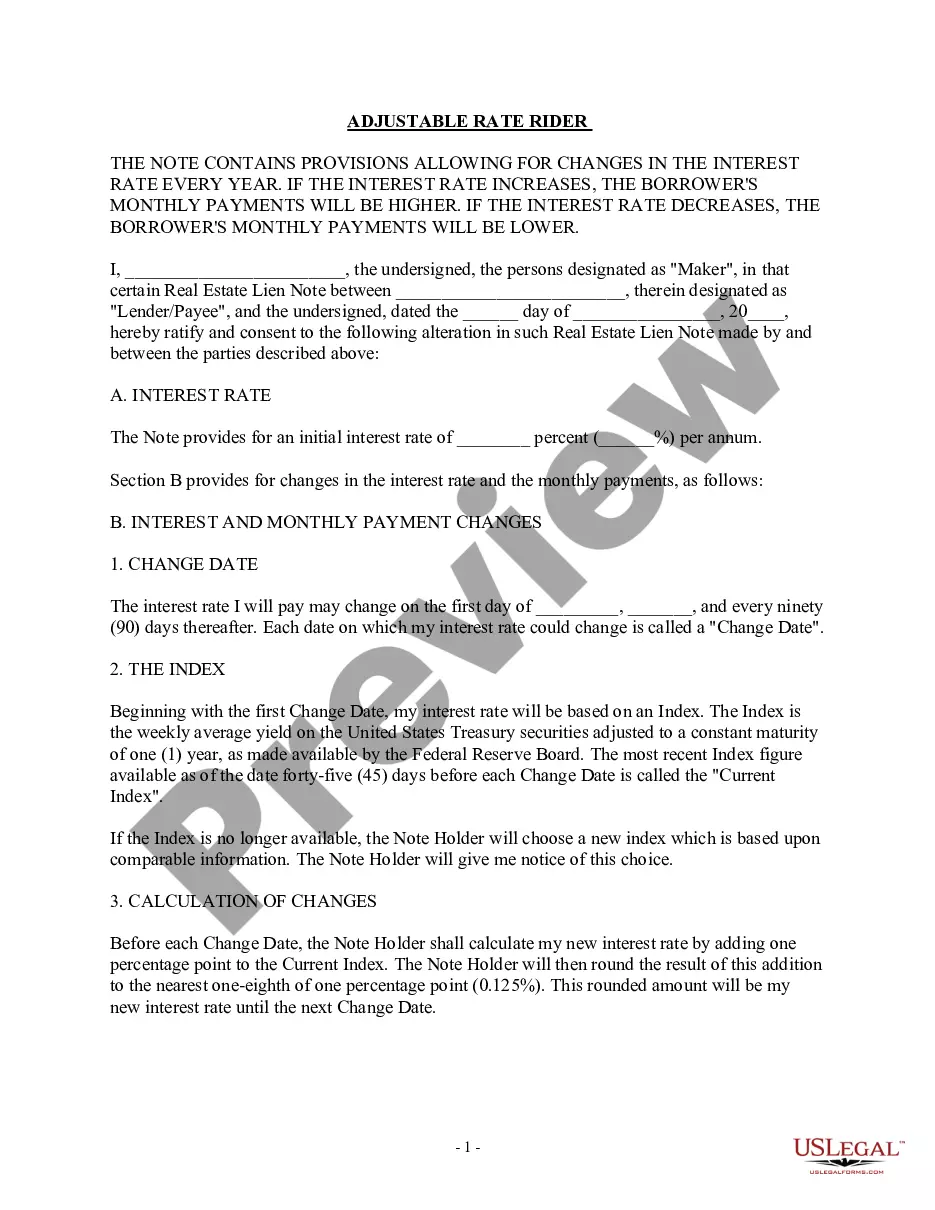

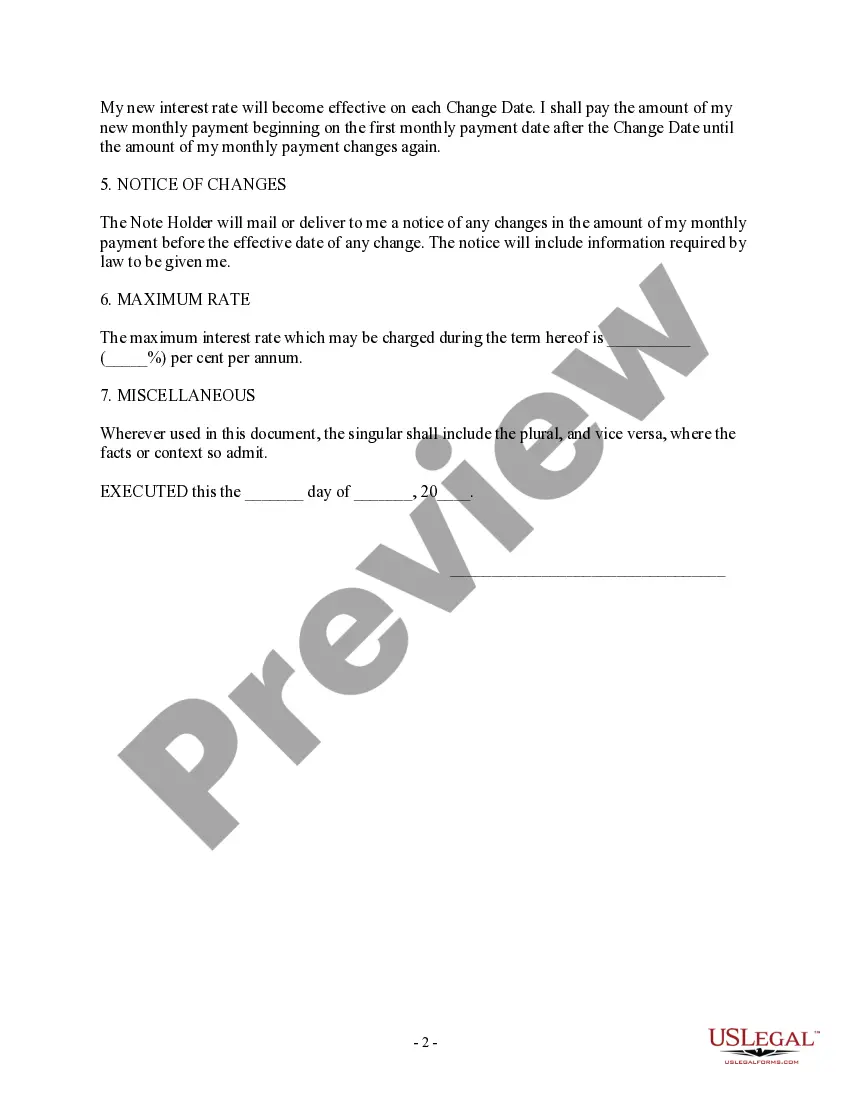

The District of Columbia Adjustable Rate Rider (ARR) — Variable Rate Note is a legal document used in real estate transactions to define the terms and conditions of an adjustable-rate mortgage (ARM) in the District of Columbia. This rider, also known as a variable rate note, provides important information about how the interest rate on the mortgage may change over time, protecting both the borrower and the lender. The District of Columbia ARR — Variable Rate Note includes several key elements. Firstly, it outlines the initial interest rate at which the mortgage will commence, usually lower than the prevailing market rate. This starting rate remains fixed for an initial period, after which it becomes adjustable based on specific criteria. The document also specifies how often the interest rate can be adjusted, often annually, and the maximum percentage by which the rate can change during each adjustment period. This protects the borrower from excessive increases in their monthly payments, known as payment shock. Furthermore, the District of Columbia ARR — Variable Rate Note contains information regarding how the new interest rate is determined. It typically references an index, such as the one-year Treasury Constant Maturity Rate, and adds a set margin determined by the lender. This combination generates the new interest rate applicable for the next adjustment period. This type of rider may include various types of adjustable rate options. For example, some District of Columbia ARR — Variable Rate Notes offer a "rate cap" that sets a maximum increase in percentage points allowed during a single adjustment period or over the entire loan term. Additionally, certain ARM's may include a "rate floor" that establishes a minimum interest rate, safeguarding the borrower from excessive decreases in the event of market fluctuations. Another consideration is the District of Columbia ARR — Variable Rate Note's "conversion option," which allows borrowers to convert their adjustable-rate mortgage into a fixed-rate mortgage after a predetermined waiting period. This feature provides flexibility in managing mortgage payments and protects against significant interest rate hikes. It is crucial for borrowers to thoroughly review the details within the District of Columbia ARR — Variable Rate Note before signing the agreement. Understanding the terms and conditions outlined in this document is essential to make informed decisions and ensure financial stability throughout the life of the mortgage. In conclusion, the District of Columbia Adjustable Rate Rider — Variable Rate Note is a legal document that defines the terms and conditions of an adjustable-rate mortgage in the District of Columbia. This document protects both borrowers and lenders by outlining the initial interest rate, the parameters for rate adjustments, and any additional features that may apply. Understanding the various types of adjustable rate options, such as rate caps, rate floors, and conversion options, can assist borrowers in making informed decisions about their mortgage financing.

District of Columbia Adjustable Rate Rider - Variable Rate Note

Description

How to fill out District Of Columbia Adjustable Rate Rider - Variable Rate Note?

It is possible to devote several hours on-line searching for the legitimate papers template that suits the federal and state demands you will need. US Legal Forms provides a large number of legitimate varieties that happen to be analyzed by pros. You can easily download or printing the District of Columbia Adjustable Rate Rider - Variable Rate Note from our service.

If you have a US Legal Forms profile, you may log in and click the Acquire button. Afterward, you may comprehensive, revise, printing, or indicator the District of Columbia Adjustable Rate Rider - Variable Rate Note. Each and every legitimate papers template you acquire is yours permanently. To acquire another backup of any acquired kind, go to the My Forms tab and click the related button.

If you work with the US Legal Forms website for the first time, follow the easy directions below:

- Initially, make sure that you have chosen the best papers template to the state/town of your choosing. Look at the kind description to ensure you have selected the correct kind. If accessible, utilize the Preview button to check throughout the papers template too.

- In order to get another version of your kind, utilize the Search area to discover the template that meets your needs and demands.

- When you have identified the template you need, click on Buy now to carry on.

- Select the costs prepare you need, key in your qualifications, and register for a free account on US Legal Forms.

- Comprehensive the transaction. You can use your credit card or PayPal profile to cover the legitimate kind.

- Select the formatting of your papers and download it in your product.

- Make modifications in your papers if possible. It is possible to comprehensive, revise and indicator and printing District of Columbia Adjustable Rate Rider - Variable Rate Note.

Acquire and printing a large number of papers layouts making use of the US Legal Forms website, that provides the largest selection of legitimate varieties. Use expert and state-certain layouts to deal with your company or specific demands.