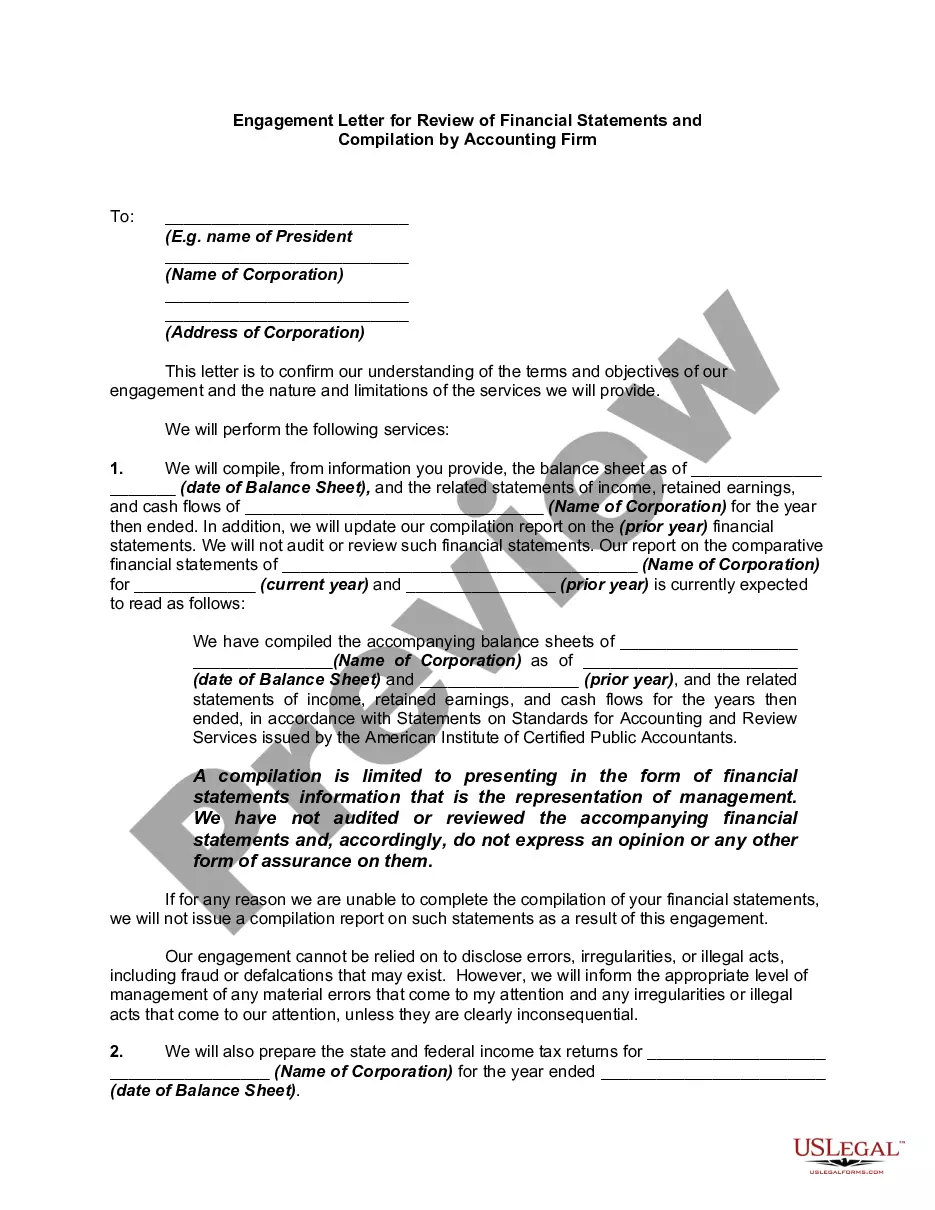

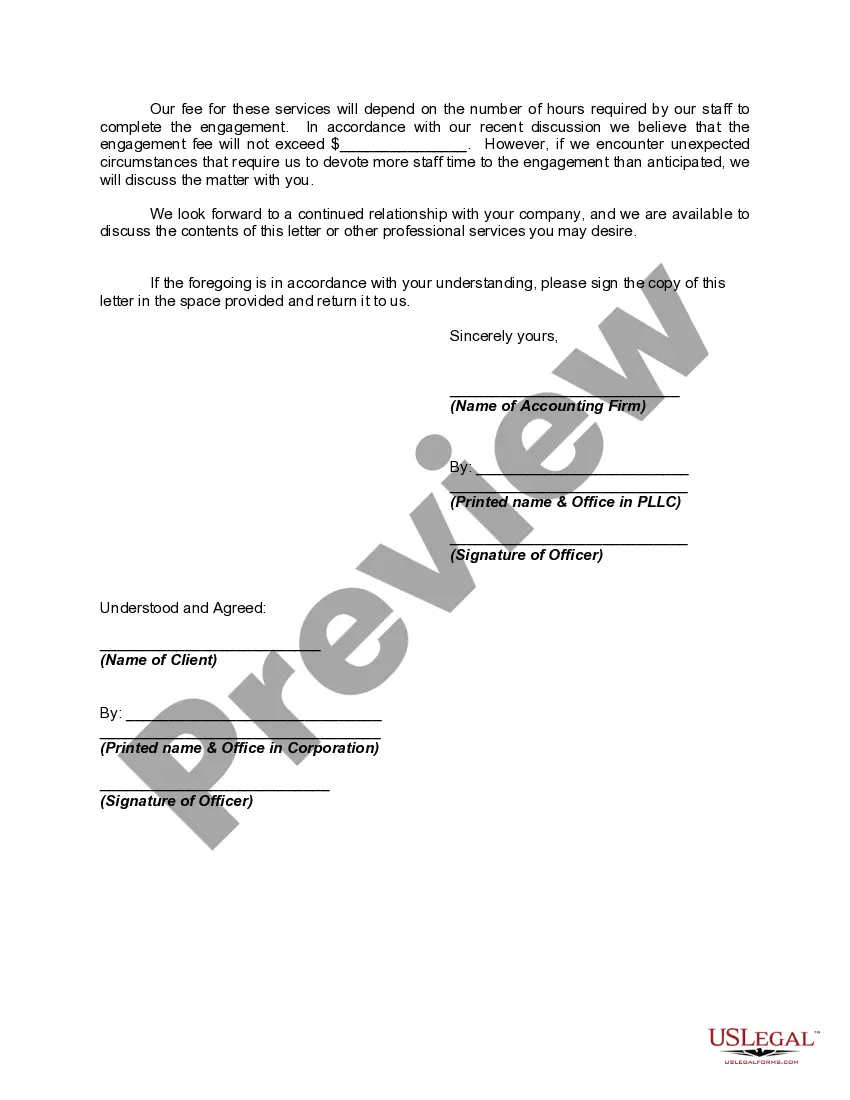

Compiled financial statements represent the most basic level of service that certified public accountants provide with respect to financial statements. In a compilation, the CPA must comply with certain basic requirements of professional standards, such as having a knowledge of the client's industry and applicable accounting principles, having a clear understanding with the client as to the services to be provided, and reading the financial statements to determine whether there are any obvious departures from generally accepted accounting principles (or, in some cases, another comprehensive basis of accounting used by the entity). It may be necessary for the CPA to perform "other accounting services" (such as creating a general ledger for the client, or assisting the client with adjusting entries for the books of the client (before the financial statements can be prepared). Upon completion, a report on the financial statements is issued that states a compilation was performed in accordance with AICPA professional standards, but no assurance is expressed that the statements are in conformity with generally accepted accounting principles. This is known as the expression of "no assurance." Compiled financial statements are often prepared for privately-held entities that do not need a higher level of assurance expressed by the CPA.

The District of Columbia Engagement Letter for Review of Financial Statements and Compilation by an Accounting Firm is a crucial document that outlines the terms and conditions between the accounting firm and the client engaging their services in the District of Columbia. This detailed description will provide information about the purpose and different types of engagement letters related to review of financial statements and compilation. An engagement letter serves as a legally binding agreement, establishing the scope of work, responsibilities, and expectations of both the accounting firm and the client. It encompasses various important aspects to ensure a smooth workflow and maintain transparency throughout the engagement. The main purpose of the Engagement Letter for Review of Financial Statements and Compilation by an Accounting Firm in the District of Columbia is to define the terms of engagement required for conducting a review of financial statements or compilation services. Reviewing financial statements involves performing analytical procedures and inquiries, whereas compilation services involve assisting in the preparation of financial statements, without expressing an opinion or assurance on their accuracy. Different types of District of Columbia Engagement Letters for Review of Financial Statements and Compilation by an Accounting Firm include: 1. Review Engagement Letter: This type of engagement letter specifically outlines the terms and conditions for the review engagement of financial statements. It includes the objectives, limitations, and responsibilities of both parties involved. The accounting firm will undertake procedures to provide limited assurance that the financial statements are free from material misstatements. 2. Compilation Engagement Letter: This engagement letter is designed for clients who require assistance in the preparation of their financial statements. It highlights the responsibilities of the accounting firm and the client throughout the compilation process, ensuring compliance with generally accepted accounting principles (GAAP) or other relevant accounting standards. Both types of engagement letter typically cover details such as the period for which the services are engaged, fees to be charged, and any specific legal or regulatory requirements within the District of Columbia. In conclusion, the District of Columbia Engagement Letter for Review of Financial Statements and Compilation by an Accounting Firm is an essential agreement that clearly defines the roles, responsibilities, and expectations of the accounting firm and the client. By establishing a comprehensive engagement letter, both parties can ensure transparency, legal compliance, and the successful completion of the review or compilation services.The District of Columbia Engagement Letter for Review of Financial Statements and Compilation by an Accounting Firm is a crucial document that outlines the terms and conditions between the accounting firm and the client engaging their services in the District of Columbia. This detailed description will provide information about the purpose and different types of engagement letters related to review of financial statements and compilation. An engagement letter serves as a legally binding agreement, establishing the scope of work, responsibilities, and expectations of both the accounting firm and the client. It encompasses various important aspects to ensure a smooth workflow and maintain transparency throughout the engagement. The main purpose of the Engagement Letter for Review of Financial Statements and Compilation by an Accounting Firm in the District of Columbia is to define the terms of engagement required for conducting a review of financial statements or compilation services. Reviewing financial statements involves performing analytical procedures and inquiries, whereas compilation services involve assisting in the preparation of financial statements, without expressing an opinion or assurance on their accuracy. Different types of District of Columbia Engagement Letters for Review of Financial Statements and Compilation by an Accounting Firm include: 1. Review Engagement Letter: This type of engagement letter specifically outlines the terms and conditions for the review engagement of financial statements. It includes the objectives, limitations, and responsibilities of both parties involved. The accounting firm will undertake procedures to provide limited assurance that the financial statements are free from material misstatements. 2. Compilation Engagement Letter: This engagement letter is designed for clients who require assistance in the preparation of their financial statements. It highlights the responsibilities of the accounting firm and the client throughout the compilation process, ensuring compliance with generally accepted accounting principles (GAAP) or other relevant accounting standards. Both types of engagement letter typically cover details such as the period for which the services are engaged, fees to be charged, and any specific legal or regulatory requirements within the District of Columbia. In conclusion, the District of Columbia Engagement Letter for Review of Financial Statements and Compilation by an Accounting Firm is an essential agreement that clearly defines the roles, responsibilities, and expectations of the accounting firm and the client. By establishing a comprehensive engagement letter, both parties can ensure transparency, legal compliance, and the successful completion of the review or compilation services.