Generally, a contract to employ a certified public accountant need not be in writing. However, such contracts often call for services of a highly complex and technical nature, and hence they should be explicit in their terms, and they should be in writing. In particular, a written employment contract is necessary in order to avoid misunderstanding with the employer regarding the amount of the accountant's fee or compensation and the nature of its computation. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

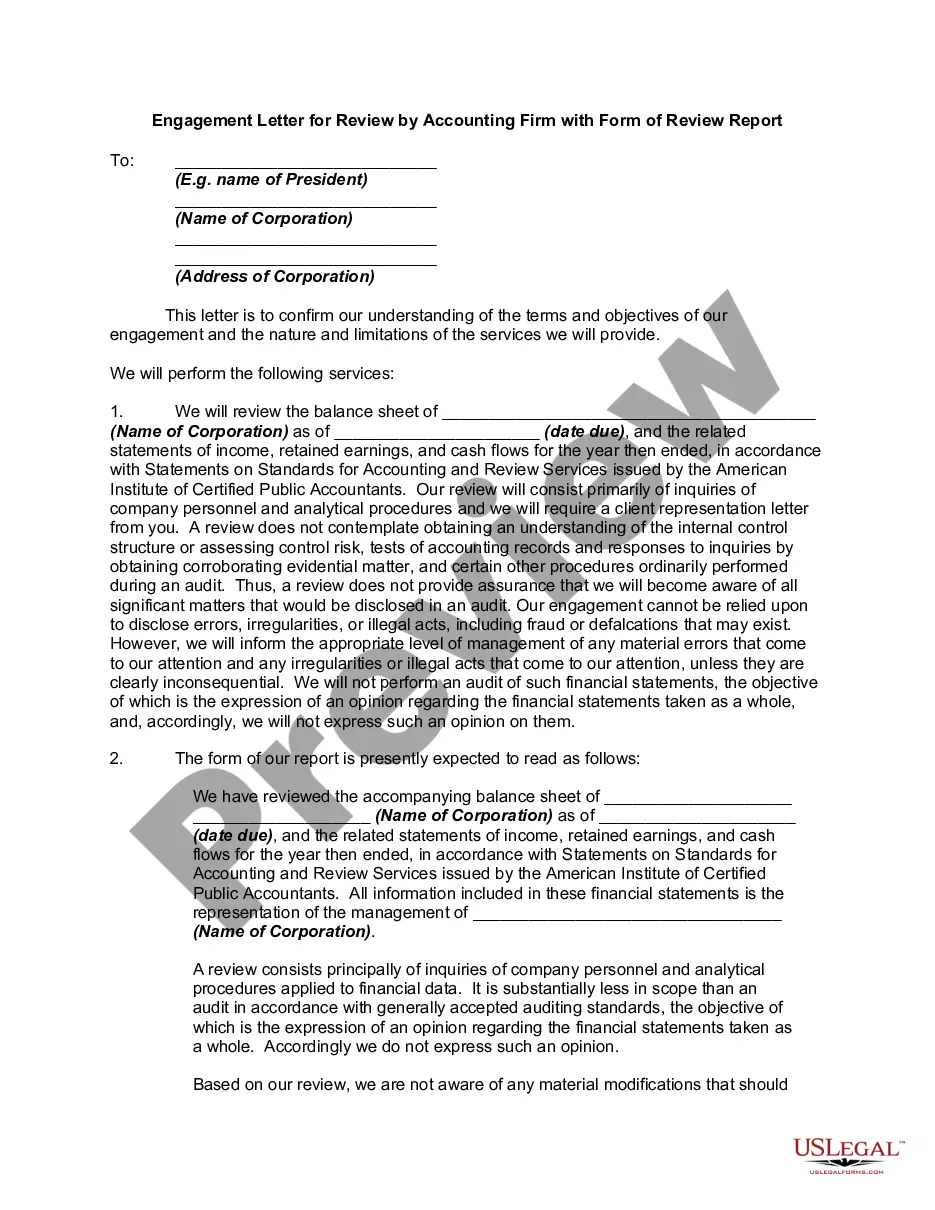

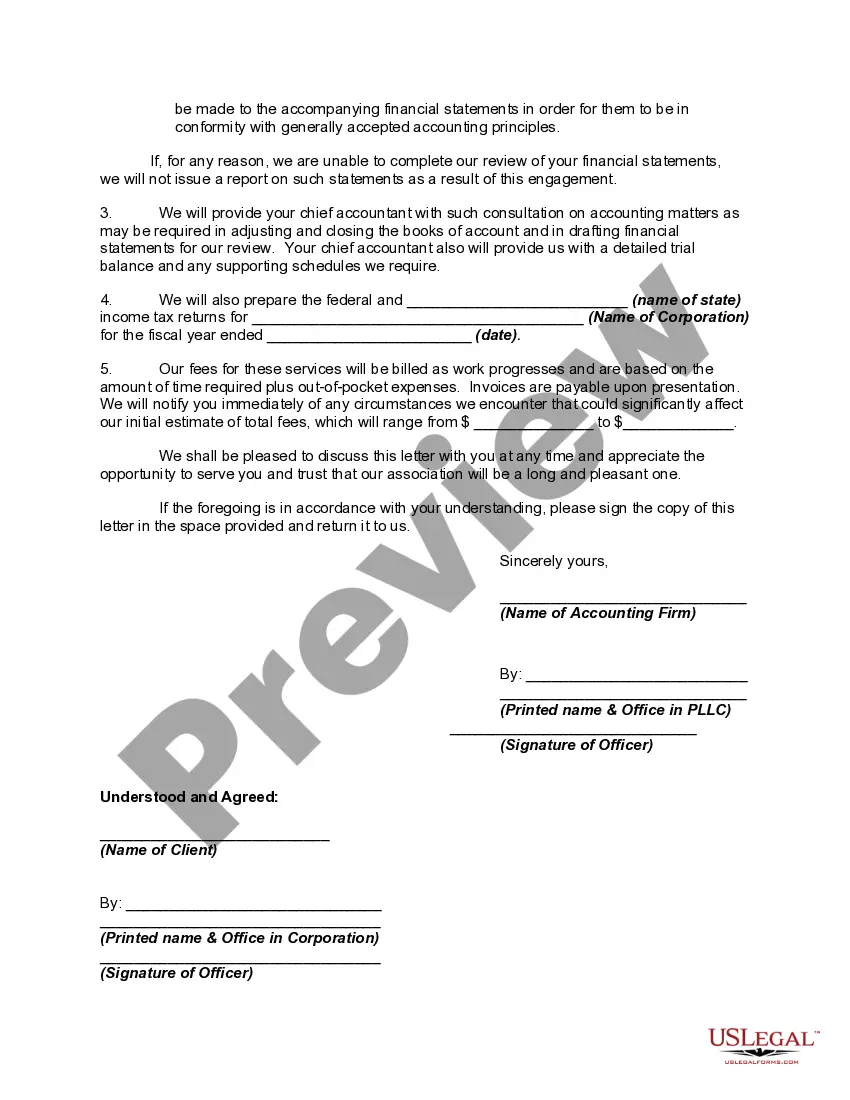

The District of Columbia Engagement Letter for Review by Accounting Firm with Form of Review Report is a crucial document that outlines the terms and conditions between an accounting firm and their client in the District of Columbia. This letter serves as a legally binding agreement between the two parties and sets the expectations for the review of financial statements and related documents. The engagement letter is designed to ensure that the accounting firm understands the scope of work requested by the client and that the client is aware of the services they will receive. It addresses the responsibilities, rights, and obligations of both parties involved. This letter is an essential component of the professional relationship between the accounting firm and their client. The District of Columbia Engagement Letter for Review by Accounting Firm with Form of Review Report consists of several sections that cover various aspects of the engagement. These sections include: 1. Introduction: This section introduces the engagement letter, identifies the parties involved (the accounting firm and the client), and specifies the purpose of the engagement. 2. Objective and Scope: This section outlines the objective of the review engagement, which is typically to express limited assurance concerning whether the financial statements are free from material misstatement. It also defines the scope of the review by describing what will be reviewed, including the accounting principles used and significant estimates made by management. 3. Responsibilities of the Accounting Firm: This section defines the responsibilities of the accounting firm, which typically include conducting the review in accordance with applicable professional standards, obtaining an understanding of the client's business, assessing the risks of material misstatement, performing analytical procedures, and issuing a review report. 4. Responsibilities of the Client: This section outlines the responsibilities of the client, such as providing the accounting firm with complete and accurate financial statements and supporting documents, granting access to necessary information, and ensuring compliance with applicable laws and regulations. 5. Fees and Billing: This section specifies the fees associated with the review engagement and the billing arrangements between the accounting firm and the client. It may include information about the hourly rates, fixed fees, or any other payment terms agreed upon. 6. Limitation of Liability: This section highlights any limitations on the liability of the accounting firm arising from the engagement. 7. Termination: This section explains the conditions under which either party can terminate the engagement, such as non-payment of fees, breaches of contract, or mutual agreement. Different types of District of Columbia Engagement Letters for Review by Accounting Firm with Form of Review Report may exist. Some may be tailored for specific industries or sectors, while others may be more general in nature. It is essential to consider the unique needs of the client and the specific requirements of the engagement when selecting the appropriate template. In conclusion, the District of Columbia Engagement Letter for Review by Accounting Firm with Form of Review Report is a comprehensive document that outlines the terms, responsibilities, and objectives of the review engagement between an accounting firm and their client. This letter ensures clarity and mutual understanding, ultimately strengthening the professional relationship between both parties involved.The District of Columbia Engagement Letter for Review by Accounting Firm with Form of Review Report is a crucial document that outlines the terms and conditions between an accounting firm and their client in the District of Columbia. This letter serves as a legally binding agreement between the two parties and sets the expectations for the review of financial statements and related documents. The engagement letter is designed to ensure that the accounting firm understands the scope of work requested by the client and that the client is aware of the services they will receive. It addresses the responsibilities, rights, and obligations of both parties involved. This letter is an essential component of the professional relationship between the accounting firm and their client. The District of Columbia Engagement Letter for Review by Accounting Firm with Form of Review Report consists of several sections that cover various aspects of the engagement. These sections include: 1. Introduction: This section introduces the engagement letter, identifies the parties involved (the accounting firm and the client), and specifies the purpose of the engagement. 2. Objective and Scope: This section outlines the objective of the review engagement, which is typically to express limited assurance concerning whether the financial statements are free from material misstatement. It also defines the scope of the review by describing what will be reviewed, including the accounting principles used and significant estimates made by management. 3. Responsibilities of the Accounting Firm: This section defines the responsibilities of the accounting firm, which typically include conducting the review in accordance with applicable professional standards, obtaining an understanding of the client's business, assessing the risks of material misstatement, performing analytical procedures, and issuing a review report. 4. Responsibilities of the Client: This section outlines the responsibilities of the client, such as providing the accounting firm with complete and accurate financial statements and supporting documents, granting access to necessary information, and ensuring compliance with applicable laws and regulations. 5. Fees and Billing: This section specifies the fees associated with the review engagement and the billing arrangements between the accounting firm and the client. It may include information about the hourly rates, fixed fees, or any other payment terms agreed upon. 6. Limitation of Liability: This section highlights any limitations on the liability of the accounting firm arising from the engagement. 7. Termination: This section explains the conditions under which either party can terminate the engagement, such as non-payment of fees, breaches of contract, or mutual agreement. Different types of District of Columbia Engagement Letters for Review by Accounting Firm with Form of Review Report may exist. Some may be tailored for specific industries or sectors, while others may be more general in nature. It is essential to consider the unique needs of the client and the specific requirements of the engagement when selecting the appropriate template. In conclusion, the District of Columbia Engagement Letter for Review by Accounting Firm with Form of Review Report is a comprehensive document that outlines the terms, responsibilities, and objectives of the review engagement between an accounting firm and their client. This letter ensures clarity and mutual understanding, ultimately strengthening the professional relationship between both parties involved.