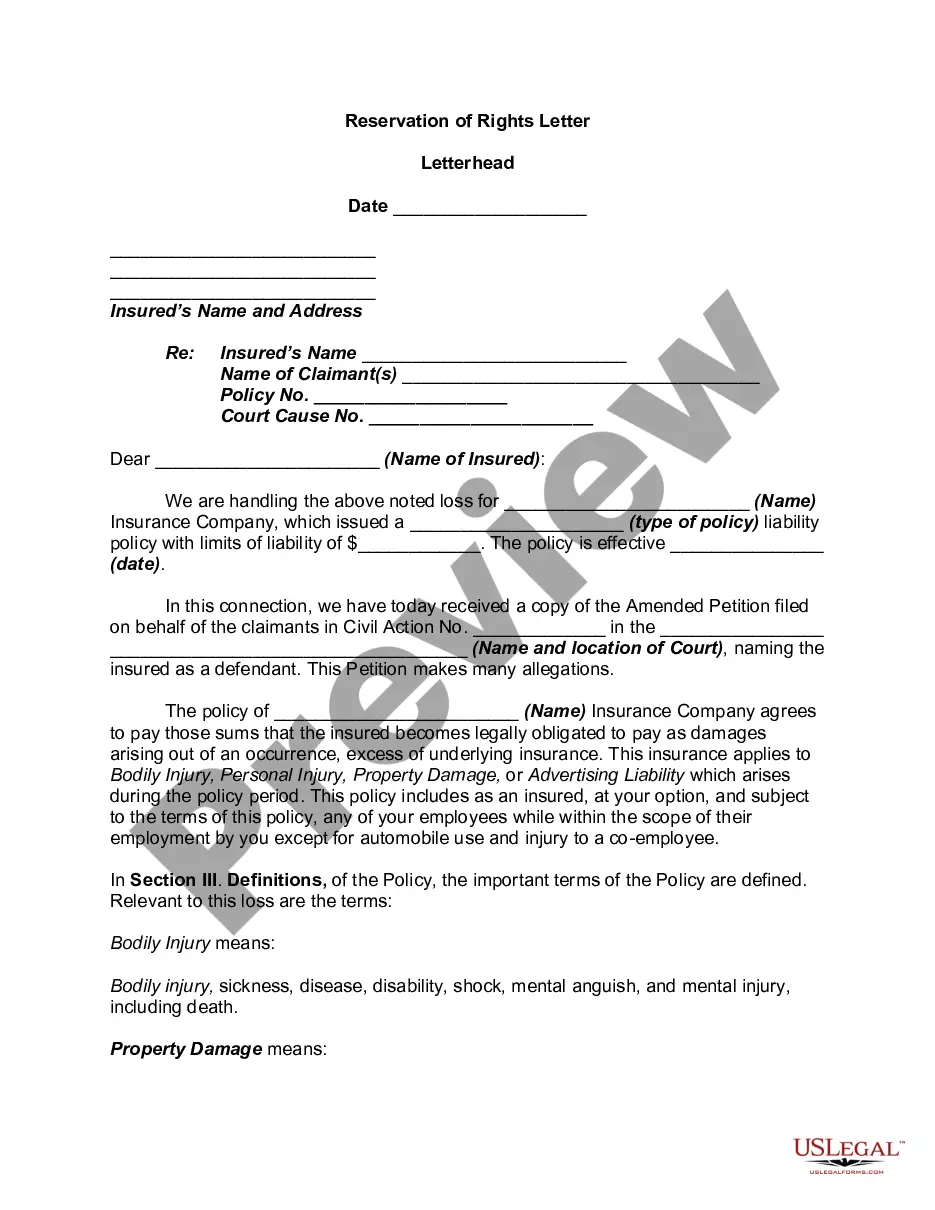

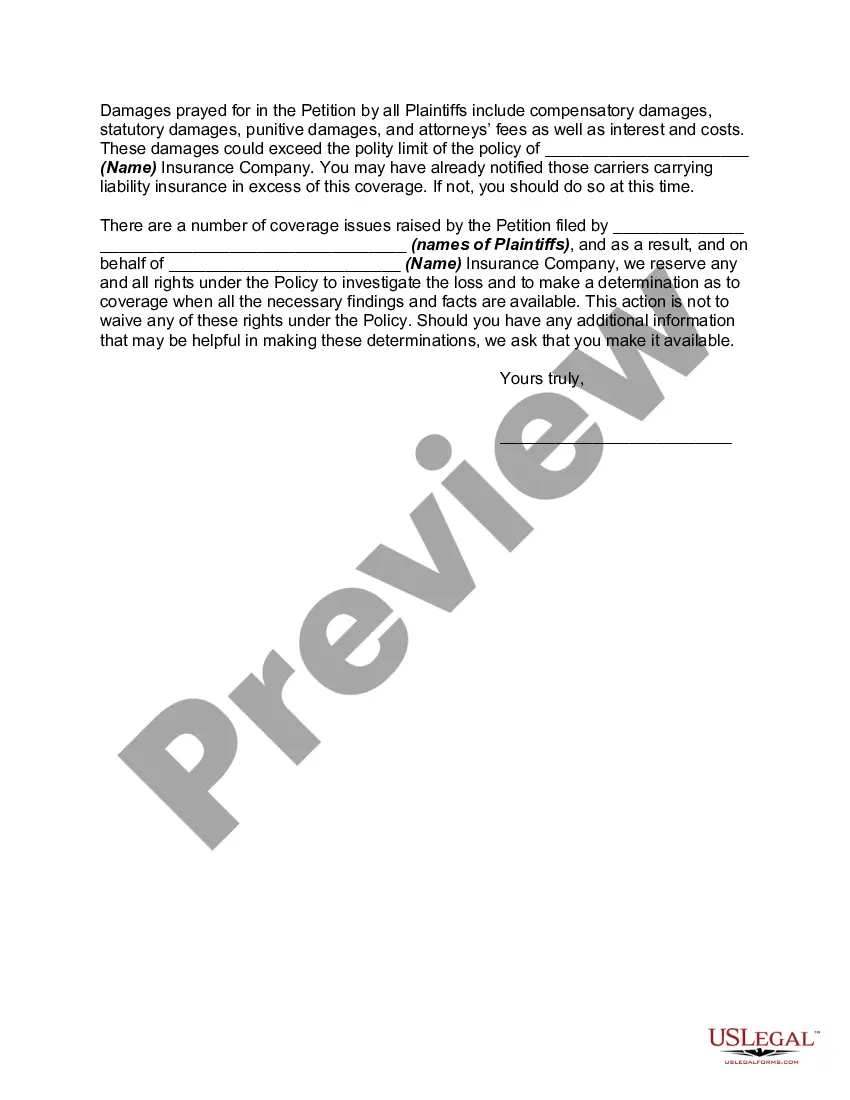

A reservation of rights defense is a means by which a liability insurance carrier agrees to protect and defend its insured against a claim or suit while reserving the right to further evaluate and perhaps even deny coverage for some or all of the claim. It is most commonly used when the claim or suit contains both covered and non-covered allegations, when the allegations are in excess of policy limits, or when the insurer is still investigating its defense and coverage obligations. For the insurer, a reservation of rights provides the flexibility to satisfy its duty to defend without committing to coverage. For the business owner who ultimately may have to pay for an adverse judgment, it requires careful monitoring and attention.

The District of Columbia Reservation of Rights Letter is a legal document that outlines the rights and protections given to individuals or businesses in the District of Columbia when it comes to insurance claims. It is essentially a written communication from an insurance company to the policyholder, notifying them of their rights and the limitations of coverage under the policy. The purpose of the Reservation of Rights Letter is to remind policyholders that the insurance company has the right to deny certain claims if they fall outside the scope of the policy's coverage. It also serves as a precautionary measure for the insurance company to avoid waiving their right to deny a claim in the event of potential coverage disputes or errors. When drafting a Reservation of Rights Letter in the District of Columbia, it is crucial to include specific keywords and information. These may include: 1. Policyholder Information: The letter must identify the policyholder, their contact details, and policy number for easy identification and reference. 2. Policy Coverage Details: It should clearly outline the coverage provisions, policy limits, exclusions, and any applicable endorsements relevant to the claim in question. This information helps the policyholder understand the extent of coverage they can expect. 3. Description of the Claim: A Reservation of Rights Letter should provide a detailed description of the claim and the circumstances of it. This allows the policyholder to understand how the insurance company perceives the situation and any potential issues with coverage. 4. Reservation of Rights Statement: The letter should explicitly state that the insurance company reserves the right to deny coverage for the claim in question or future claims if certain criteria are not met. This statement helps protect the insurance company's position in case of disputes or legal actions. 5. Legal and Financial Consequences: The Reservation of Rights Letter should outline the potential consequences of a claim denial, including the policyholder's obligations, responsibilities, and any potential costs they may bear. It is important to note that there may not be different types of Reservation of Rights Letters specific to the District of Columbia. However, variations in content and language may occur depending on the nature of the claim, the applicable insurance policy type (e.g., homeowners, commercial, auto), and any unique circumstances associated with the claim. Overall, the District of Columbia Reservation of Rights Letter is a crucial legal document that ensures transparency and clarifies the rights and obligations of both the insurance company and the policyholder in case of claim disputes.