In the United States, the Fair Credit Billing Act allows there is protection for a consumer in the event of unsatisfactory purchases, and undelivered or misrepresented services/products. If you are unsatisfied with a purchase from a store, there are things you can do. If the merchant refuses to refund your money or replace the item, you may be able to take action against your credit card company. Your rights are established by law, but they depend on certain things, such as the purpose of your purchase (business or personal), how much the product cost, and how far from your home you were when you made the purchase.

There are some factors regarding your purchase that must be considered to determine if the credit card company is legally liable:

" Type of card that you used - You must have charged the item by using the charge card issued by the store where you bought it or by using a bank card, rebate card, or travel card. Even if two stores are owned by a parent company, one store may not give you a refund for purchases made at another store.

" Price of merchandise - If the merchandise was bought with a card not issued by the seller, then the product must cost more than $50. If you paid $49.99, then the dispute is between you and the merchant, and the credit card issuer does not have to resolve the matter.

" Form and timing of complaint - You must complain in writing within 60 days after the first bill containing the error arrives. Some bank cards will intervene on your behalf even if you do not write them until after the time limit, but they may charge you an additional fee for doing so.

" Location of transaction - The purchase must have occurred within your home state or within 100 miles of your billing address, unless the item was purchased with the seller's charge card. If you travel more than 100 miles from your billing address to make a purchase, your card issuers does not legally have to become involved in your request for a refund. However, many card issuers will waive this mileage rule.

There are some circumstances under which the card company is not legally responsible. Some of these include:

" Business purchases. The credit card issuer has no responsibility for the transaction if a purchase was made for business purposes.

" If you have already paid for your merchandise. It may not help to contact your credit card company if the purchase is paid for already. If a product is defective or stops working after it is paid for, your dispute is with the store and not with your card issuer. Your best course of action in this case is to contact the store, the manufacturer, and/or the service center.

" You sign a blank receipt. If you sign a blank credit card receipt before services are rendered, and the service provider determines that additional costs are necessary even though above and beyond what was quoted, you may still liable.

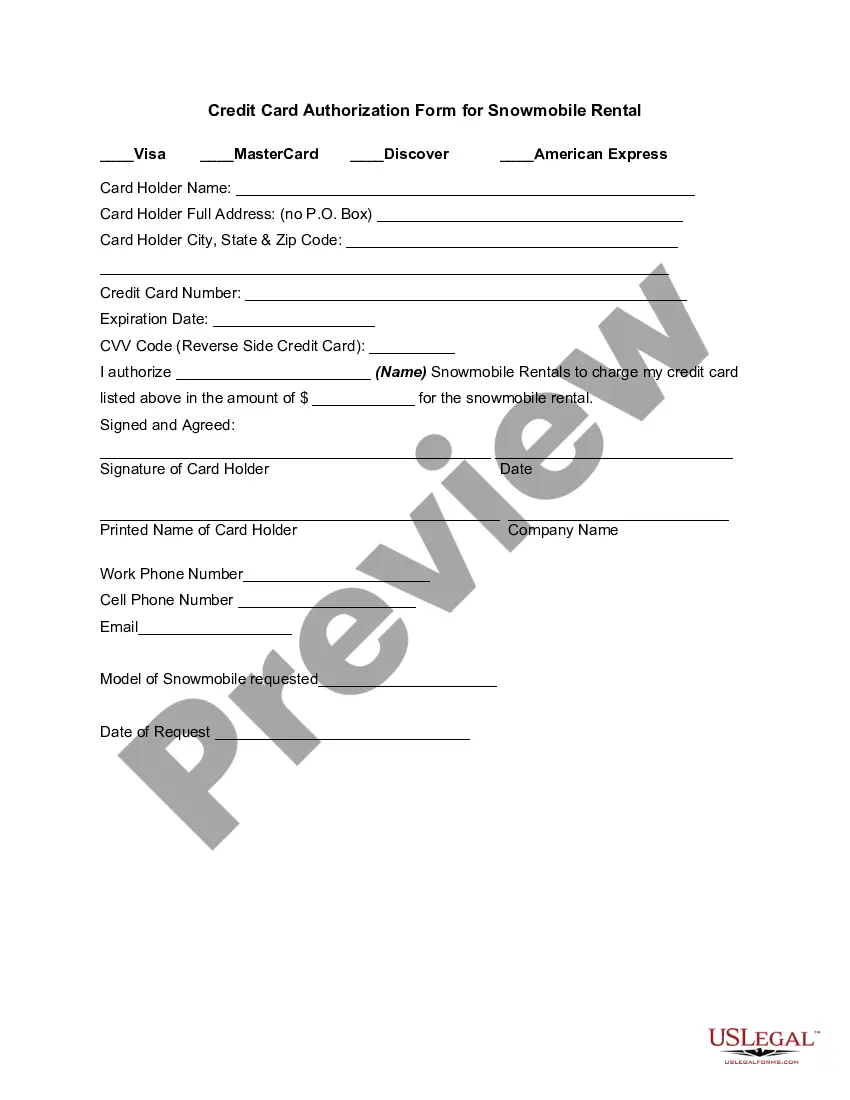

The District of Columbia Credit Card Authorization Form for Snowmobile Rental is a document that allows snowmobile rental companies in the District of Columbia to securely obtain the necessary credit card information from customers as a security deposit for renting snowmobiles. This form is a crucial financial management tool, granting the company permission to charge the credit card in case of any damage, loss, or additional fees incurred during the rental period. Snowmobile rental companies in the District of Columbia understand the need for a credit card authorization process to protect their assets and ensure a smooth customer experience. By utilizing this form, rental companies can request and collect all relevant information, including the customer's name, contact details, credit card number, expiration date, security code, and billing address. The form guarantees that the customer consents to the rental company charging their credit card for any potential expenses due to accidents, repairs, or unpaid rental fees. It also typically includes important terms and conditions such as rental rates, cancellation policies, and liability waivers. Customers are required to read and agree to these terms before signing the form, ensuring legal compliance and mutual understanding. Different variations or types of District of Columbia Credit Card Authorization Form for Snowmobile Rental might exist, such as: 1. Standard Credit Card Authorization Form: This is the basic version of the form that incorporates all the essential fields to collect credit card information and customer consent. It complies with the legal requirements of the District of Columbia. 2. Customized Credit Card Authorization Form: Some snowmobile rental companies may create their own customized form to fit their specific business needs. This variation could include additional sections to collect supplementary information or include company-specific policies and disclaimers. 3. Online Credit Card Authorization Form: With advancements in technology, many businesses offer the convenience of online forms. This type of form allows customers to provide their credit card details securely through an encrypted online portal. Regardless of the specific type, the District of Columbia Credit Card Authorization Form for Snowmobile Rental serves as a vital document in ensuring a secure and efficient rental process for both the company and its customers. By using this form, rental companies can protect their interests while providing customers with a hassle-free experience, ensuring a memorable and enjoyable snowmobiling adventure in the District of Columbia.