District of Columbia Simple Promissory Note for Tutition Fee

Description

How to fill out Simple Promissory Note For Tutition Fee?

Are you in a situation where you frequently require documents for both business or personal purposes? There are numerous legal document templates available online, but finding reliable ones can be challenging.

US Legal Forms offers thousands of form templates, including the District of Columbia Simple Promissory Note for Tuition Fee, designed to meet both federal and state regulations.

If you are already familiar with the US Legal Forms website and have an account, simply Log In. Afterward, you can download the District of Columbia Simple Promissory Note for Tuition Fee template.

You can access all the document templates you have purchased in the My documents section. You can download another copy of the District of Columbia Simple Promissory Note for Tuition Fee at any time if necessary. Just click on the required form to download or print the document template.

Utilize US Legal Forms, one of the most extensive collections of legal documents, to save time and minimize errors. The service provides professionally created legal document templates that can be used for various purposes. Create an account on US Legal Forms and start making your life easier.

- If you do not have an account and want to start using US Legal Forms, follow these steps.

- 1. Locate the form you need and ensure it is for the correct state/region.

- 2. Use the Review button to examine the form.

- 3. Read the description to confirm you have selected the right form.

- 4. If the form isn’t what you are looking for, use the Search box to find the form that fits your needs and requirements.

- 5. Once you find the correct form, click Purchase now.

- 6. Choose the pricing plan you want, fill out the required information to create your account, and pay for the order using PayPal or a credit card.

- 7. Select a convenient document format and download your version.

Form popularity

FAQ

To fill out a promissory demand note, begin similarly to a traditional promissory note, specifying the terms under which repayment is expected. Mention that the amount is due upon demand, which provides flexibility and urgency. Clearly include both parties' names, addresses, and the total amount owed. For a reliable and user-friendly experience, uslegalforms offers templates that guide you in creating a comprehensive promissory demand note.

A simple promissory note might be for a lump sum repayment on a certain date. For example, you lend your friend $1,000 and he agrees to repay you by December 1. The full amount is due on that date, and there is no payment schedule involved.

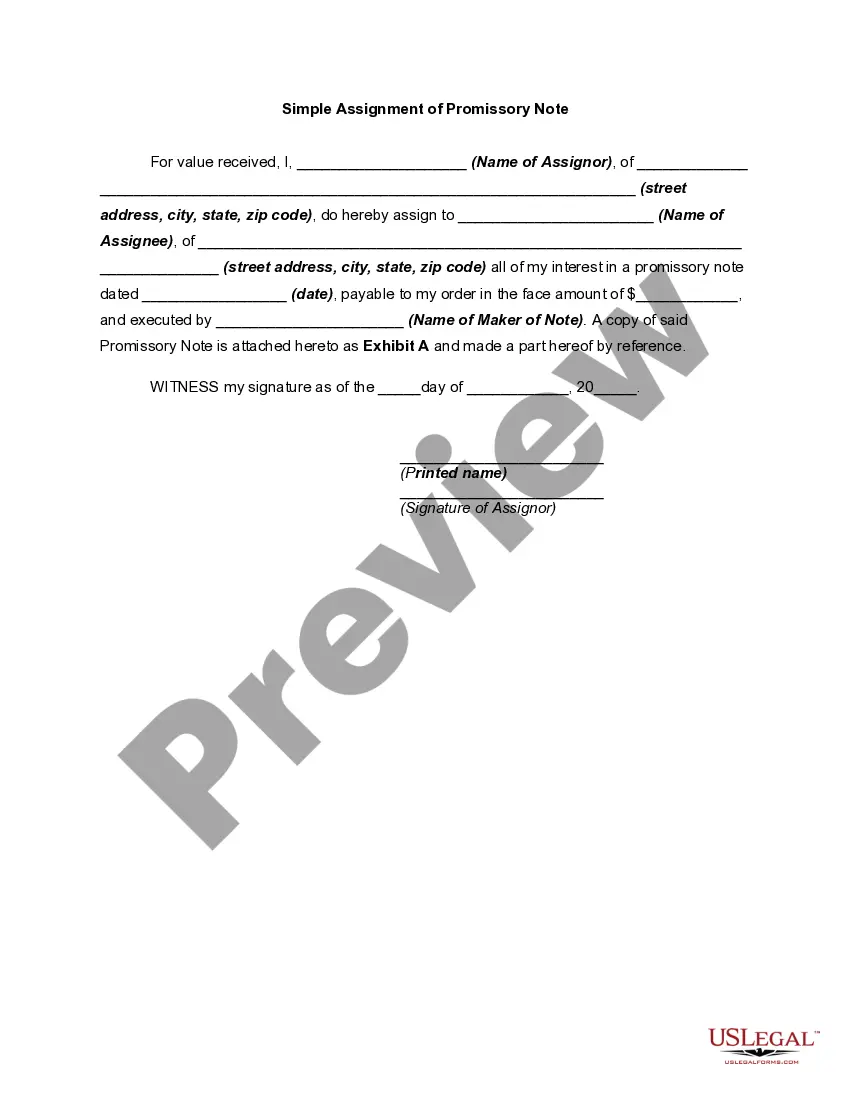

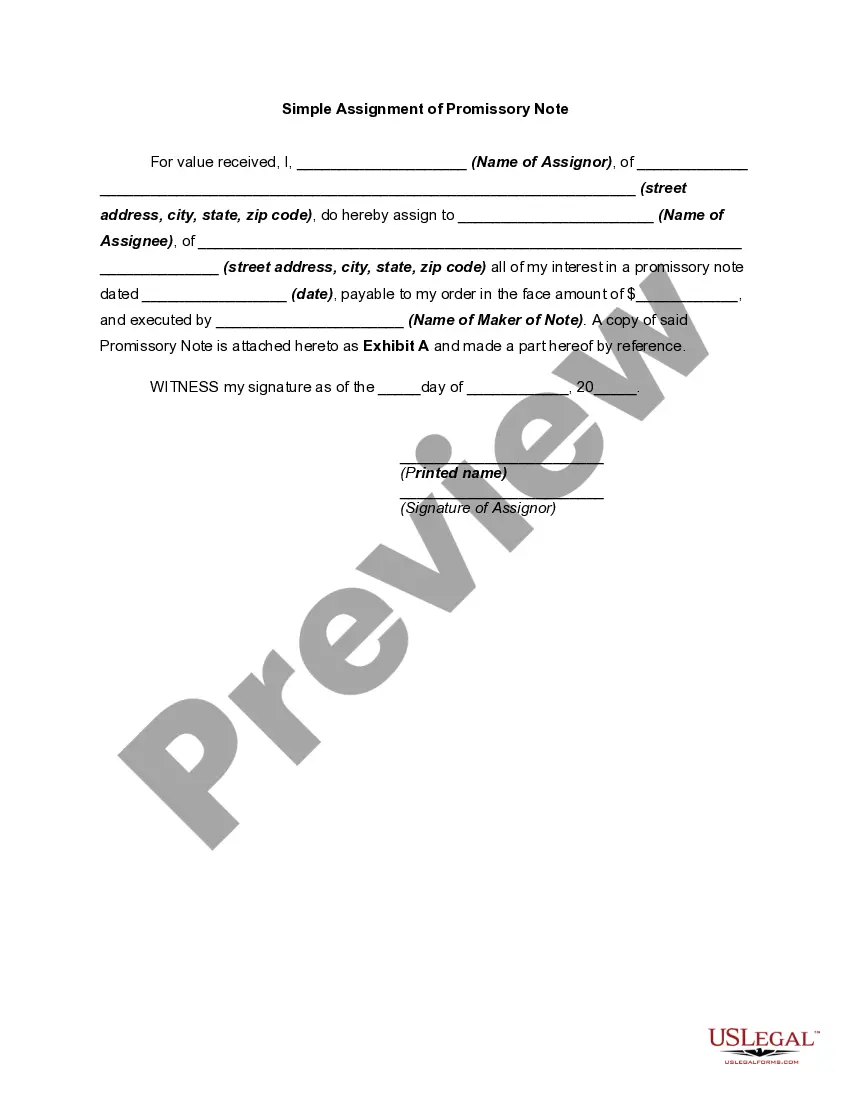

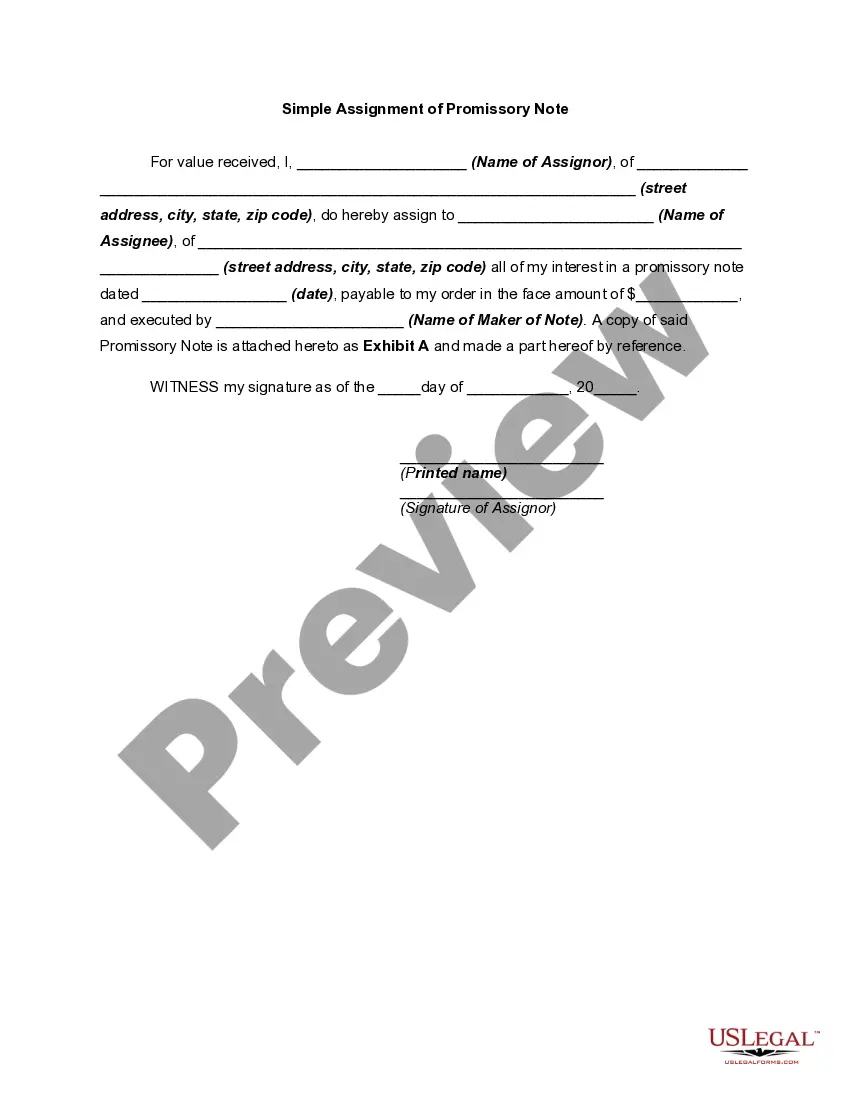

Simple Promissory Note SampleInclude the date you are writing or the date you plan to send the note at the top. Write the total amount due in both numeric and long-form. Add a detailed description of the loan or note terms. For example, you'll need to include what the loan or payment is for, who will pay it and how.

In order for a promissory note to be valid and legally binding, it needs to include specific information. "A promissory note should include details including the amount loaned, the repayment schedule and whether it is secured or unsecured," says Wheeler.

You can use a template or create a promissory note online. But before you begin, you'll need to gather some information and make decisions about the way the loan will be structured. First, you'll need the names and addresses of both the lender (or "payee") and the borrower.

At its most basic, a promissory note should include the following things:Date.Name of the lender and borrower.Loan amount.Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral?Payment amount and frequency.Payment due date.Whether the loan has a cosigner, and if so, who.

Although a promissory note is usually written on a computer and printed out or a pre-made form is filled out, a handwritten promissory note signed by both parties is legal and will stand up in court.

You can use a template or create a promissory note online. But before you begin, you'll need to gather some information and make decisions about the way the loan will be structured. First, you'll need the names and addresses of both the lender (or "payee") and the borrower.

This is to express in writing my inability to pay on time the amount due for my tuition fees amounting to P. I promise to pay said amount on or before . Furthermore, I am fully aware that subsequent Promissory Notes shall not be accepted without settling my current due amount.

If you're signing a promissory note, make sure it includes these details:Date. The promissory note should include the date it was created at the top of the page.Amount.Loan terms.Interest rate.Collateral.Lender and borrower information.Signatures.