This form is a type of asset-financing arrangement in which a company uses its receivables (money owed by customers) as collateral in a financing agreement. The company receives an amount that is equal to a reduced value of the receivables pledged. The age of the receivables have a large effect on the amount a company will receive. The older the receivables, the less the company can expect.

This type of financing helps companies free up capital that is stuck in accounts receivables. Accounts receivable financing transfers the default risk associated with the accounts receivables to the financing company. This transfer of risk can help the company using the financing to shift focus from trying to collect receivables to current business activities.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

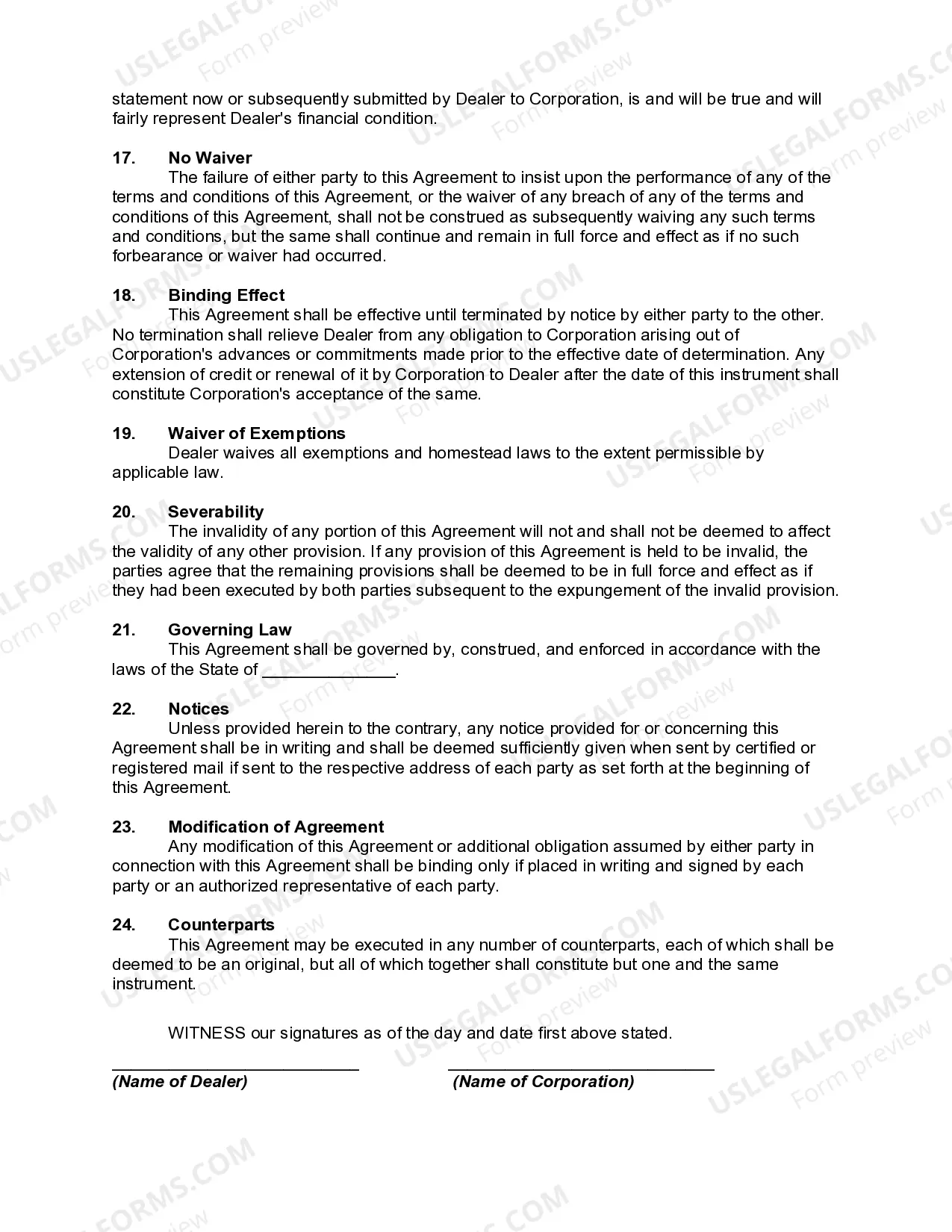

District of Columbia Financing Agreement between Dealer and Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles is an important legal document that outlines the terms and conditions of the financial arrangement between the dealer and the credit corporation. This agreement is specifically designed for wholesale financing transactions while also establishing a security interest in accounts and general intangibles. In the District of Columbia, several types of financing agreements may be conducted between the dealer and the credit corporation. These can include: 1. Traditional Financing Agreement: This type of agreement involves the credit corporation providing funds directly to the dealer for the purchase of wholesale inventory. The dealer agrees to repay the credit corporation in installments according to the terms outlined in the agreement. 2. Floor Plan Financing Agreement: This agreement allows the dealer to borrow funds from the credit corporation to purchase and maintain inventory for resale. The dealer's inventory serves as collateral for the loan, ensuring the credit corporation's security interest in the accounts and general intangibles. 3. Revolving Line of Credit Agreement: This type of agreement establishes a predetermined credit limit for the dealer to finance wholesale purchases and other business expenses. The dealer can borrow and repay funds within the credit limit, similar to a credit card. The accounts and general intangibles act as security for the credit corporation. The District of Columbia Financing Agreement between Dealer and Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles serves several purposes. Firstly, it sets forth the terms of the financing arrangement, such as the loan amount, interest rates, repayment schedule, and any associated fees. Furthermore, the agreement specifies the rights and obligations of both parties involved. It outlines the rights of the credit corporation to monitor the dealer's financial performance, access records, and inspect the collateral to ensure compliance with the agreement. Similarly, the dealer's responsibilities, including maintaining and insuring the inventory, providing financial statements, and timely repayment, are also detailed within the agreement. The security interest section of the agreement is crucial, as it establishes the credit corporation's rights over the dealer's accounts and general intangibles. This encompasses receivables from customers, intellectual property, and any other intangible assets, providing added security for the credit corporation in case of default. It is vital for both the dealer and credit corporation to carefully review and negotiate the terms of the District of Columbia Financing Agreement. Seeking legal counsel is advised to ensure compliance with local regulations and to protect the interests of both parties involved in the wholesale financing transaction.