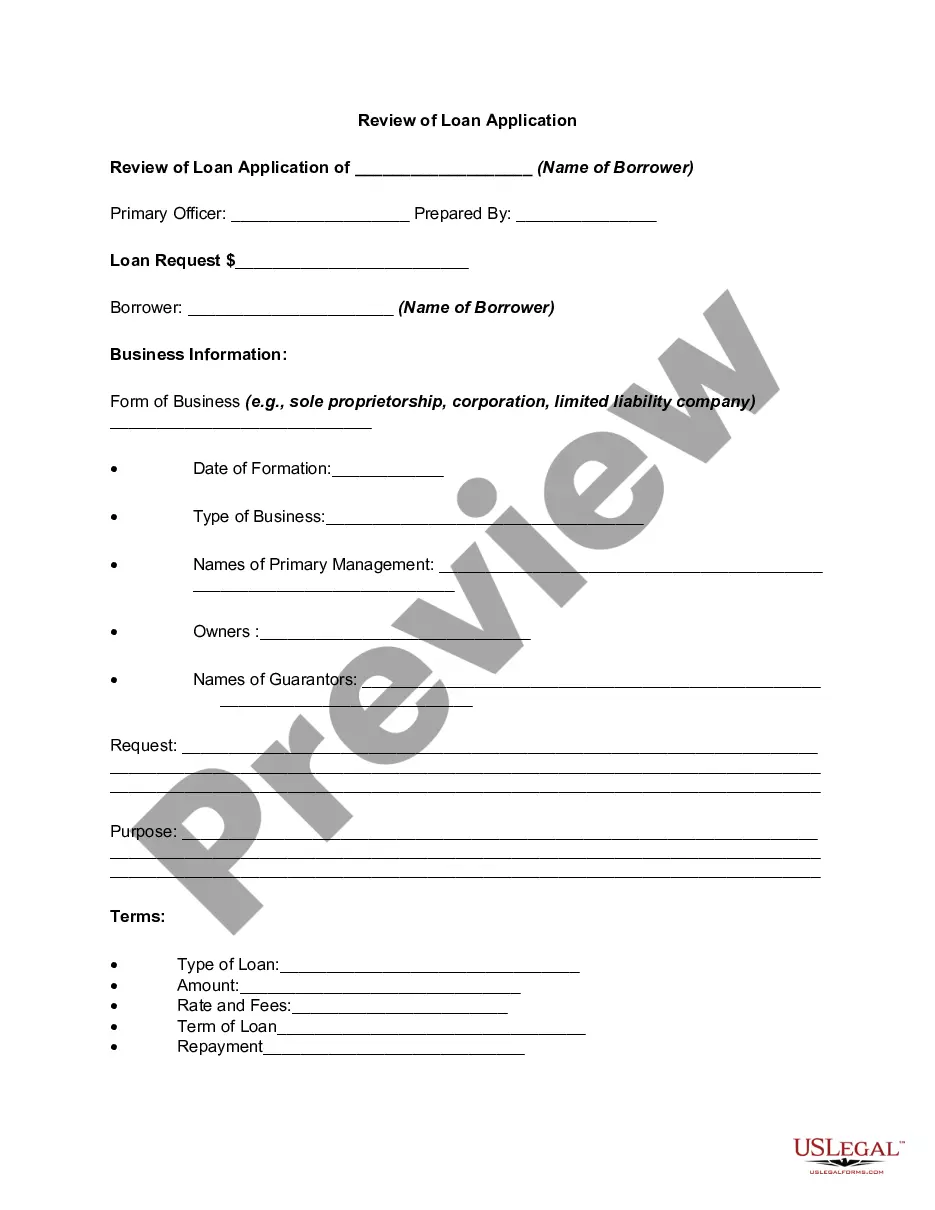

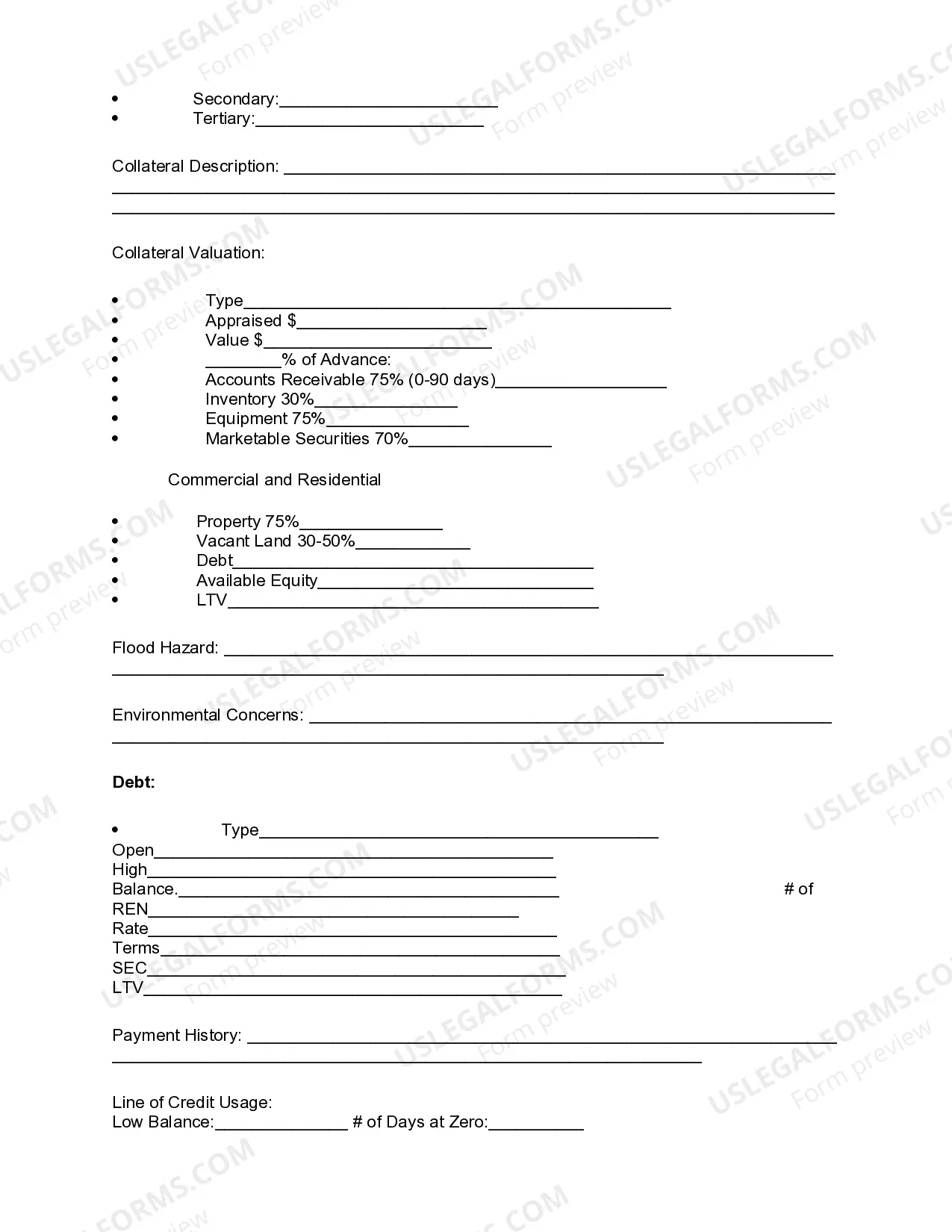

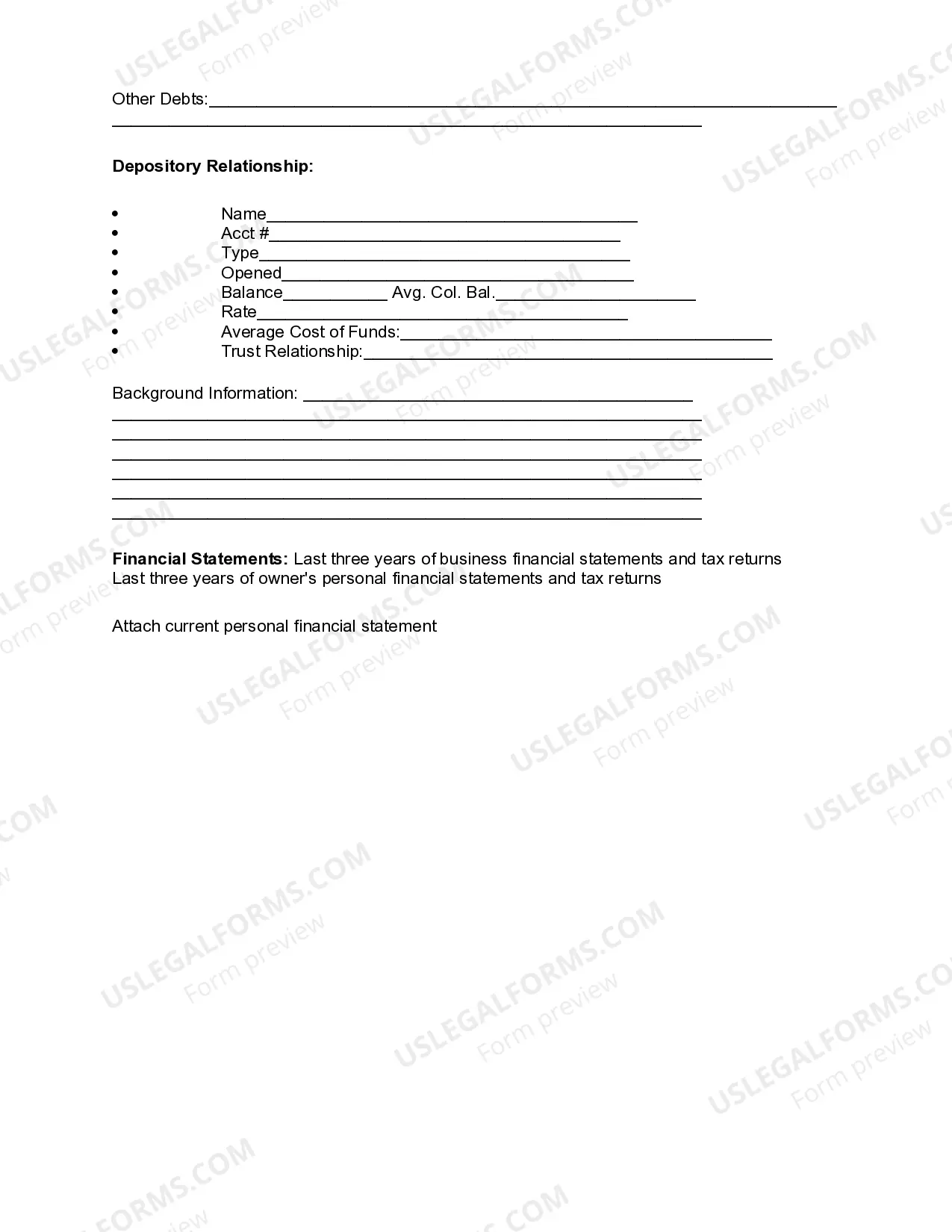

District of Columbia Review of Loan Application is a thorough and extensive evaluation process conducted by financial institutions or lending agencies in the District of Columbia to assess and analyze loan applications submitted by borrowers. This review aims to determine the eligibility, creditworthiness, and overall financial stability of the applicants in order to make informed decisions regarding loan approval or rejection. The District of Columbia Review of Loan Application examines various crucial aspects of the borrower's finances, including income, employment history, credit score, and debt-to-income ratio. Lenders closely scrutinize these factors to gauge the applicant's ability to make regular payments and repay the loan on time. In addition to the regular loan application review, there are certain types of District of Columbia Review of Loan Application that are specific to different loan categories. These may include: 1. Mortgage Loan Application Review: This type of review focuses on assessing the borrower's eligibility for a mortgage loan, such as verifying employment stability, analyzing credit history, conducting property appraisals, and evaluating the loan-to-value ratio. 2. Auto Loan Application Review: Lenders perform an extensive evaluation of the applicant's creditworthiness, employment, income, and the vehicle's value and condition. This review helps in determining the loan amount, interest rate, and loan terms applicable to the auto loan. 3. Personal Loan Application Review: For personal loans, lenders review the borrower's credit score, income, debt obligations, and other factors to assess the risk associated with lending money. This review helps in determining the loan amount, interest rate, and repayment period for the personal loan. 4. Small Business Loan Application Review: This type of review focuses on evaluating the creditworthiness, financial statements, business plan, collateral, and the potential profitability of the small business seeking a loan. This review helps lenders in determining the loan terms, interest rate, and loan amount applicable to the business loan. During the District of Columbia Review of Loan Application, the lender may request additional documentation and information from the borrower to validate the details provided in the application. They may also check the borrower's employment history, contact references, and perform background checks. Ultimately, the District of Columbia Review of Loan Application serves as a comprehensive evaluation method that enables lenders to assess the risk associated with approving a loan for borrowers in the District of Columbia. It ensures responsible lending practices and protects both the borrower and the lender's interests.

District of Columbia Review of Loan Application

Description

How to fill out District Of Columbia Review Of Loan Application?

US Legal Forms - one of the greatest libraries of lawful varieties in the United States - provides a wide array of lawful file themes you may acquire or produce. Utilizing the site, you can get a huge number of varieties for business and person functions, categorized by types, says, or keywords.You will find the newest types of varieties just like the District of Columbia Review of Loan Application within minutes.

If you currently have a subscription, log in and acquire District of Columbia Review of Loan Application through the US Legal Forms collection. The Down load option can look on each and every kind you view. You gain access to all formerly acquired varieties from the My Forms tab of your own accounts.

If you would like use US Legal Forms the first time, listed below are straightforward recommendations to help you started off:

- Make sure you have picked the proper kind to your area/region. Click the Review option to review the form`s information. See the kind explanation to actually have selected the correct kind.

- If the kind doesn`t fit your demands, make use of the Look for field at the top of the display screen to discover the one that does.

- When you are satisfied with the form, validate your decision by simply clicking the Buy now option. Then, choose the costs plan you prefer and offer your qualifications to sign up for the accounts.

- Approach the deal. Make use of charge card or PayPal accounts to accomplish the deal.

- Choose the formatting and acquire the form on the gadget.

- Make changes. Fill up, edit and produce and sign the acquired District of Columbia Review of Loan Application.

Each and every template you put into your money does not have an expiry day and it is the one you have permanently. So, if you would like acquire or produce one more duplicate, just visit the My Forms area and click on about the kind you will need.

Obtain access to the District of Columbia Review of Loan Application with US Legal Forms, the most considerable collection of lawful file themes. Use a huge number of expert and condition-certain themes that meet up with your business or person needs and demands.