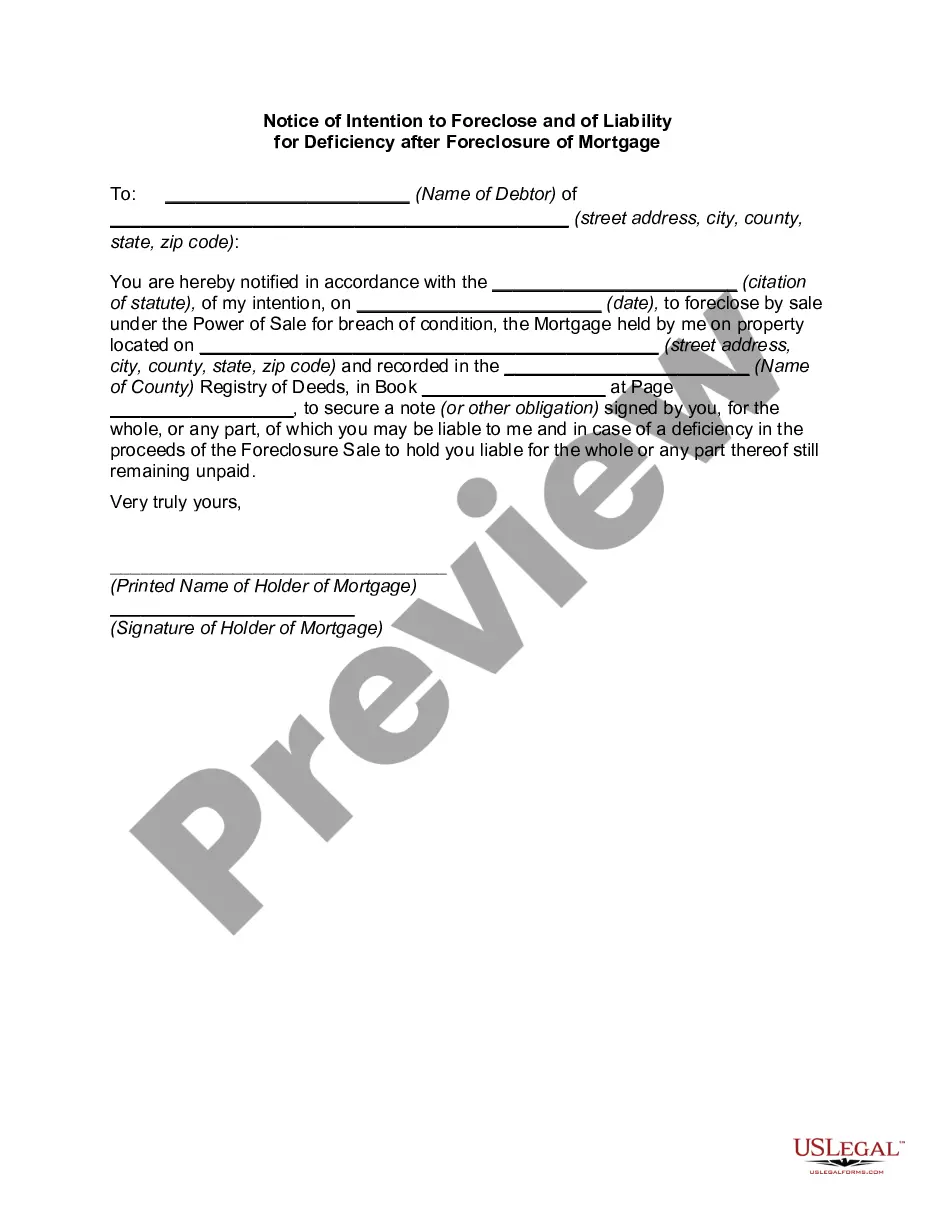

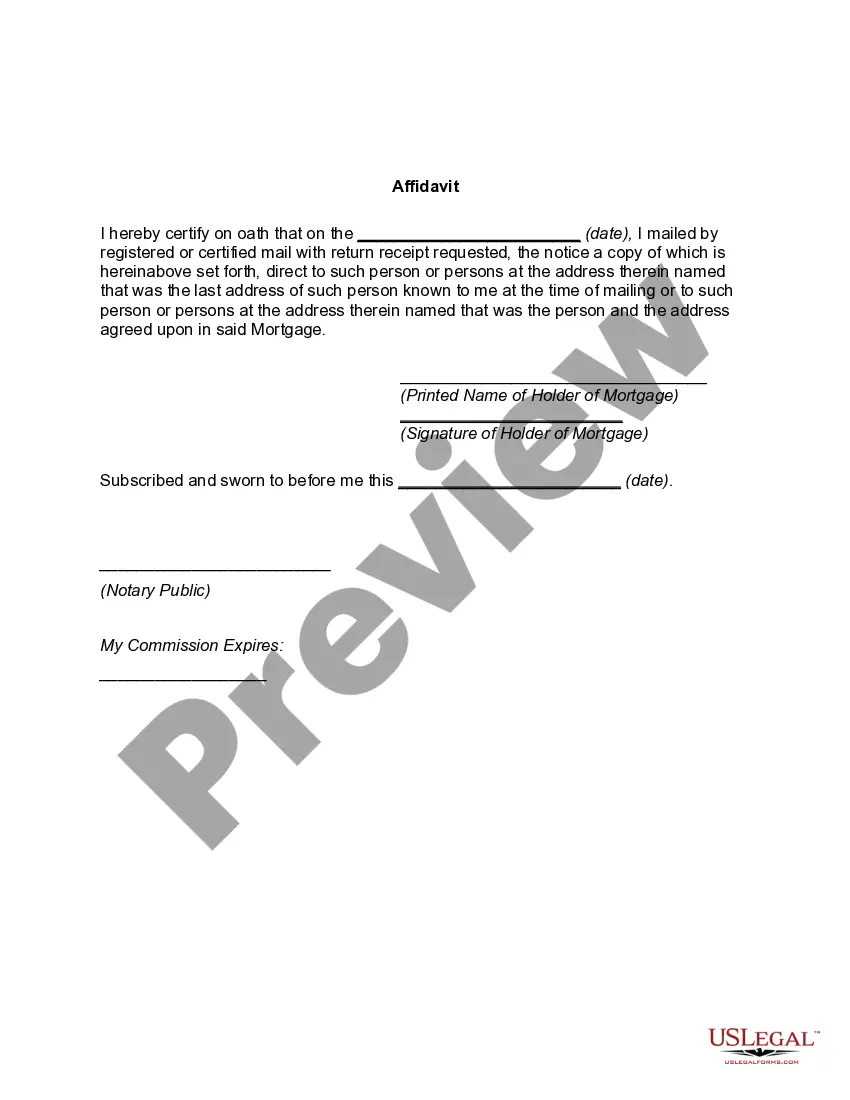

The District of Columbia Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage is a legal document that serves as notification to borrowers of the lender's intention to initiate foreclosure proceedings due to a default on the mortgage loan. This notice outlines the borrower's rights and responsibilities during the foreclosure process, as well as the potential liability for any deficiency balance remaining after the foreclosure sale. In the District of Columbia, there are different types or variations of the Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage. Some specific types include: 1. Standard Notice of Intention to Foreclose: This type of notice is typically sent by the lender to the borrower when they fall behind on their mortgage payments. It provides notification that the lender intends to foreclose on the property if the borrower does not remedy the default within a specified period. 2. Final Notice of Intention to Foreclose: If the borrower fails to cure the default or reach a mutually acceptable agreement with the lender within the specified period mentioned in the initial notice, the lender may issue a Final Notice of Intention to Foreclose. This notice reiterates the lender's intent to proceed with foreclosure and provides a last opportunity for the borrower to resolve the default. 3. Notice of Sale: Once the foreclosure process has been initiated, the lender must provide the borrower with a Notice of Sale. This notice details the date, time, and location of the foreclosure sale and informs the borrower of their right to redeem the property prior to the sale, if applicable. 4. Notice of Liability for Deficiency: After the completion of the foreclosure sale, if the proceeds from the sale do not cover the outstanding mortgage debt, the lender may pursue a deficiency judgment against the borrower. The Notice of Liability for Deficiency serves as a notification to the borrower that they may be held responsible for the remaining deficiency balance. It is important for borrowers who receive any of these notices to seek legal advice and explore available options to prevent foreclosure or minimize potential liability for deficiency. Understanding the specific requirements and timelines outlined in these notices can help borrowers navigate the foreclosure process and protect their rights.

District of Columbia Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage

Description

How to fill out District Of Columbia Notice Of Intention To Foreclose And Of Liability For Deficiency After Foreclosure Of Mortgage?

US Legal Forms - among the biggest libraries of lawful varieties in America - provides a wide range of lawful record web templates you can obtain or print out. While using site, you may get 1000s of varieties for organization and specific purposes, sorted by categories, says, or keywords and phrases.You will find the latest variations of varieties such as the District of Columbia Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage within minutes.

If you currently have a monthly subscription, log in and obtain District of Columbia Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage from your US Legal Forms local library. The Download option will appear on every form you view. You get access to all previously acquired varieties inside the My Forms tab of the profile.

If you wish to use US Legal Forms for the first time, listed below are simple guidelines to get you started off:

- Ensure you have chosen the proper form to your city/area. Select the Preview option to analyze the form`s content. Read the form description to ensure that you have chosen the appropriate form.

- When the form doesn`t fit your specifications, take advantage of the Lookup area at the top of the display screen to obtain the one that does.

- If you are satisfied with the form, affirm your selection by clicking on the Buy now option. Then, select the costs strategy you like and offer your references to register on an profile.

- Method the financial transaction. Use your credit card or PayPal profile to complete the financial transaction.

- Pick the formatting and obtain the form in your product.

- Make modifications. Complete, revise and print out and sign the acquired District of Columbia Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage.

Every format you put into your bank account lacks an expiry time and is also your own property eternally. So, in order to obtain or print out one more copy, just visit the My Forms portion and click about the form you want.

Gain access to the District of Columbia Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage with US Legal Forms, one of the most substantial local library of lawful record web templates. Use 1000s of specialist and state-specific web templates that meet up with your small business or specific demands and specifications.