District of Columbia Challenge to Credit Report of Experian, TransUnion, and/or Equifax

Description

How to fill out Challenge To Credit Report Of Experian, TransUnion, And/or Equifax?

If you have to full, down load, or printing legal papers themes, use US Legal Forms, the greatest collection of legal forms, which can be found on-line. Utilize the site`s simple and practical research to get the paperwork you require. A variety of themes for business and person purposes are categorized by groups and says, or keywords and phrases. Use US Legal Forms to get the District of Columbia Challenge to Credit Report of Experian, TransUnion, and/or Equifax with a few click throughs.

When you are currently a US Legal Forms buyer, log in for your accounts and then click the Download switch to obtain the District of Columbia Challenge to Credit Report of Experian, TransUnion, and/or Equifax. You may also accessibility forms you in the past downloaded within the My Forms tab of the accounts.

If you use US Legal Forms for the first time, refer to the instructions listed below:

- Step 1. Make sure you have selected the shape to the proper city/country.

- Step 2. Use the Review choice to examine the form`s articles. Never neglect to read the explanation.

- Step 3. When you are unsatisfied using the type, utilize the Lookup area near the top of the display to locate other types of your legal type web template.

- Step 4. After you have located the shape you require, go through the Buy now switch. Pick the rates program you choose and add your qualifications to sign up for the accounts.

- Step 5. Process the financial transaction. You can use your bank card or PayPal accounts to finish the financial transaction.

- Step 6. Find the format of your legal type and down load it on your own gadget.

- Step 7. Complete, revise and printing or indicator the District of Columbia Challenge to Credit Report of Experian, TransUnion, and/or Equifax.

Each legal papers web template you purchase is your own property forever. You have acces to each type you downloaded inside your acccount. Select the My Forms area and pick a type to printing or down load again.

Compete and down load, and printing the District of Columbia Challenge to Credit Report of Experian, TransUnion, and/or Equifax with US Legal Forms. There are thousands of expert and status-distinct forms you may use to your business or person demands.

Form popularity

FAQ

When you are applying for a mortgage to buy a home, lenders will typically look at all of your credit history reports from the three major credit bureaus ? Experian, Equifax, and TransUnion. In most cases, mortgage lenders will look at your FICO score. There are different FICO scoring models.

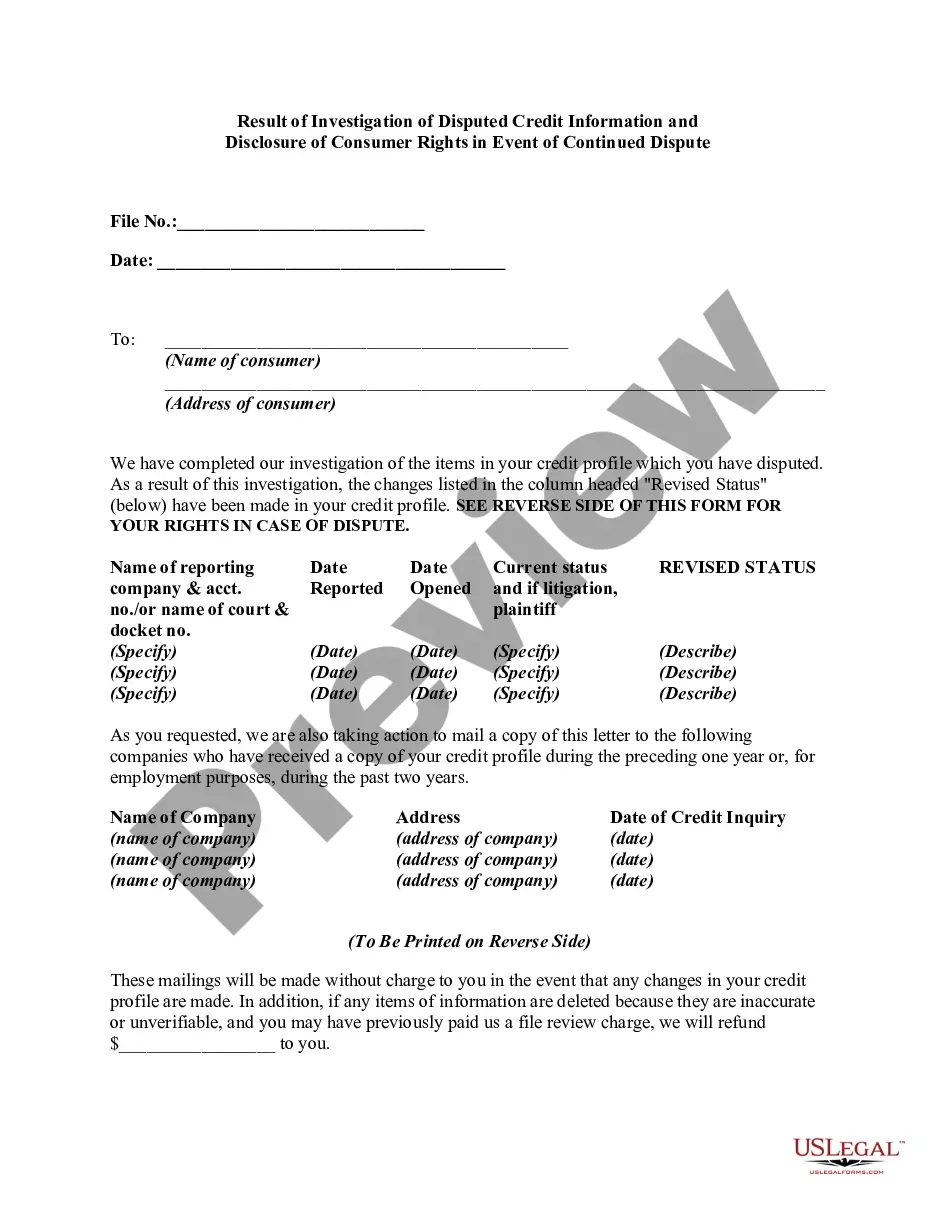

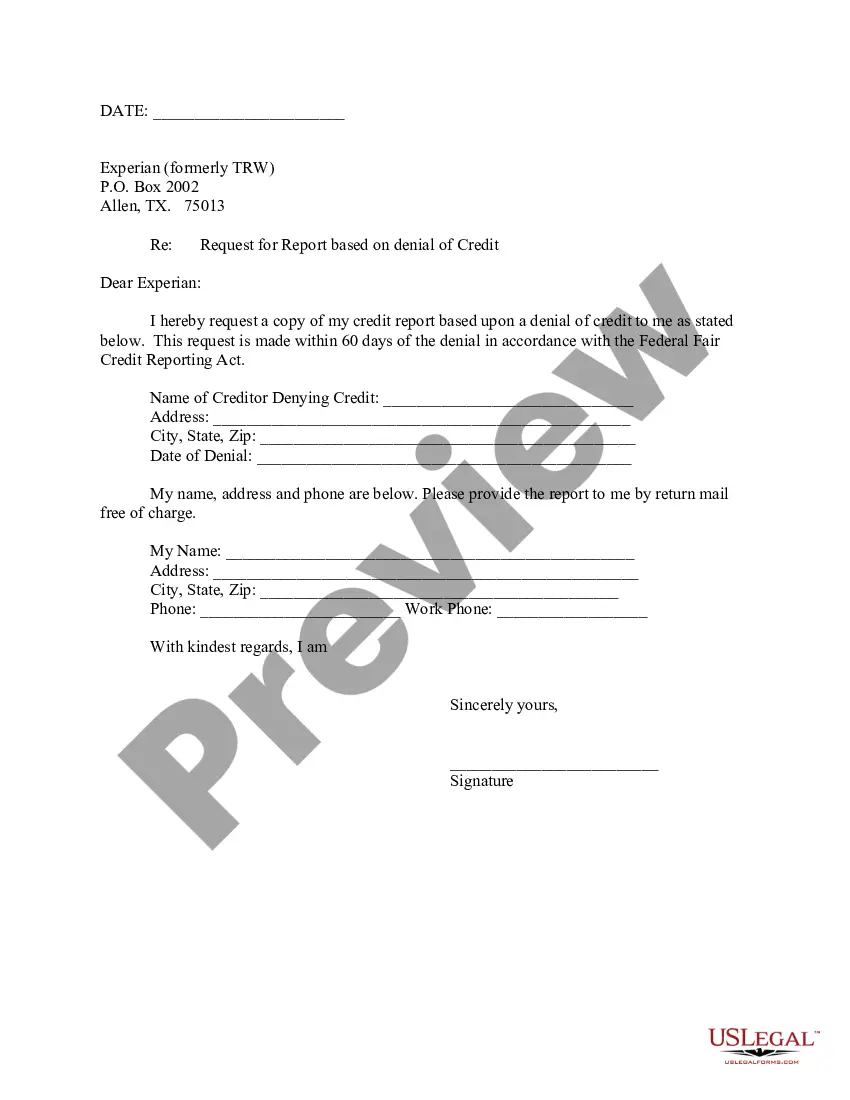

If you have a document that you would like to submit to substantiate a dispute regarding the information on your personal credit report, you can mail it to Experian's National Consumer Assistance Center at P.O. Box 4500, Allen, TX 75013, or upload your document at experian.com/upload to submit it online.

If you want to freeze your credit, you need to do it at each of the three major credit bureaus: Equifax (1-800-349-9960) TransUnion (1-888-909-8872) Experian (1-888-397-3742) .

A very poor credit score is in the range of 300 ? 600, with 601 ? 660 considered to be poor. A score of 661 ? 720 is fair. And an excellent score is in the range of 781 ? 850.

The primary credit scoring models are FICO® and VantageScore®, and both are equally accurate. Although both are accurate, most lenders are looking at your FICO score when you apply for a loan.

Neither your TransUnion or Equifax score is more or less accurate than the other. They're just calculated from slightly differing sources. Your Equifax credit score is likely lower due to reporting differences. Nonetheless, a ?fair? score from TransUnion is typically ?fair? across the board.

The Bottom Line You are entitled by law to freeze your credit reports anytime, for free. To do so, you must request a security freeze at each of the national credit bureaus individually. Freezing your credit limits criminals' ability to open loans and credit card accounts in your name.

When you are applying for a mortgage to buy a home, lenders will typically look at all of your credit history reports from the three major credit bureaus ? Experian, Equifax, and TransUnion. In most cases, mortgage lenders will look at your FICO score. There are different FICO scoring models.

To freeze your credit, you have to contact each of the three credit bureaus individually. Placing a credit freeze is free for you and your children, as is lifting it when applying for new credit.

No credit score from any one of the credit bureaus is more valuable or more accurate than another. It's possible that a lender may gravitate toward one score over another, but that doesn't necessarily mean that score is better.