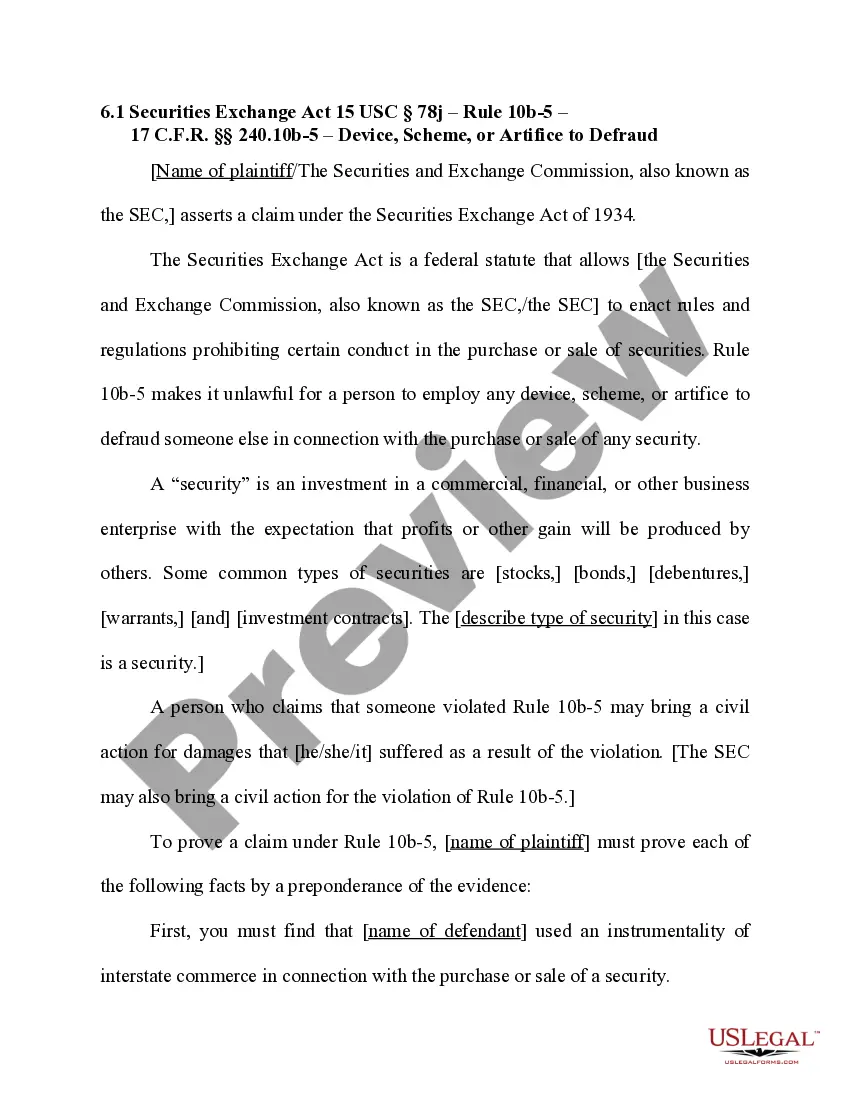

District of Columbia Jury Instruction - 4.4.1 Rule 10(b) - 5(a) Device, Scheme Or Artifice To Defraud Insider Trading

Description

How to fill out Jury Instruction - 4.4.1 Rule 10(b) - 5(a) Device, Scheme Or Artifice To Defraud Insider Trading?

Discovering the right lawful file format could be a have difficulties. Obviously, there are plenty of themes available online, but how can you discover the lawful type you need? Utilize the US Legal Forms site. The assistance provides a huge number of themes, for example the District of Columbia Jury Instruction - 4.4.1 Rule 10(b) - 5(a) Device, Scheme Or Artifice To Defraud Insider Trading, that you can use for organization and private requires. Every one of the kinds are examined by pros and fulfill state and federal demands.

When you are currently authorized, log in to your profile and click on the Obtain key to find the District of Columbia Jury Instruction - 4.4.1 Rule 10(b) - 5(a) Device, Scheme Or Artifice To Defraud Insider Trading. Utilize your profile to search through the lawful kinds you possess bought formerly. Visit the My Forms tab of your own profile and obtain another backup from the file you need.

When you are a brand new consumer of US Legal Forms, listed here are basic guidelines that you should stick to:

- Very first, ensure you have selected the right type to your city/region. You may check out the shape using the Review key and read the shape description to ensure this is basically the right one for you.

- If the type will not fulfill your requirements, take advantage of the Seach discipline to get the correct type.

- Once you are certain the shape would work, select the Acquire now key to find the type.

- Choose the prices program you want and type in the necessary information. Make your profile and buy your order utilizing your PayPal profile or credit card.

- Pick the data file file format and obtain the lawful file format to your device.

- Complete, change and produce and indication the obtained District of Columbia Jury Instruction - 4.4.1 Rule 10(b) - 5(a) Device, Scheme Or Artifice To Defraud Insider Trading.

US Legal Forms is the greatest local library of lawful kinds in which you can find different file themes. Utilize the service to obtain expertly-created documents that stick to state demands.