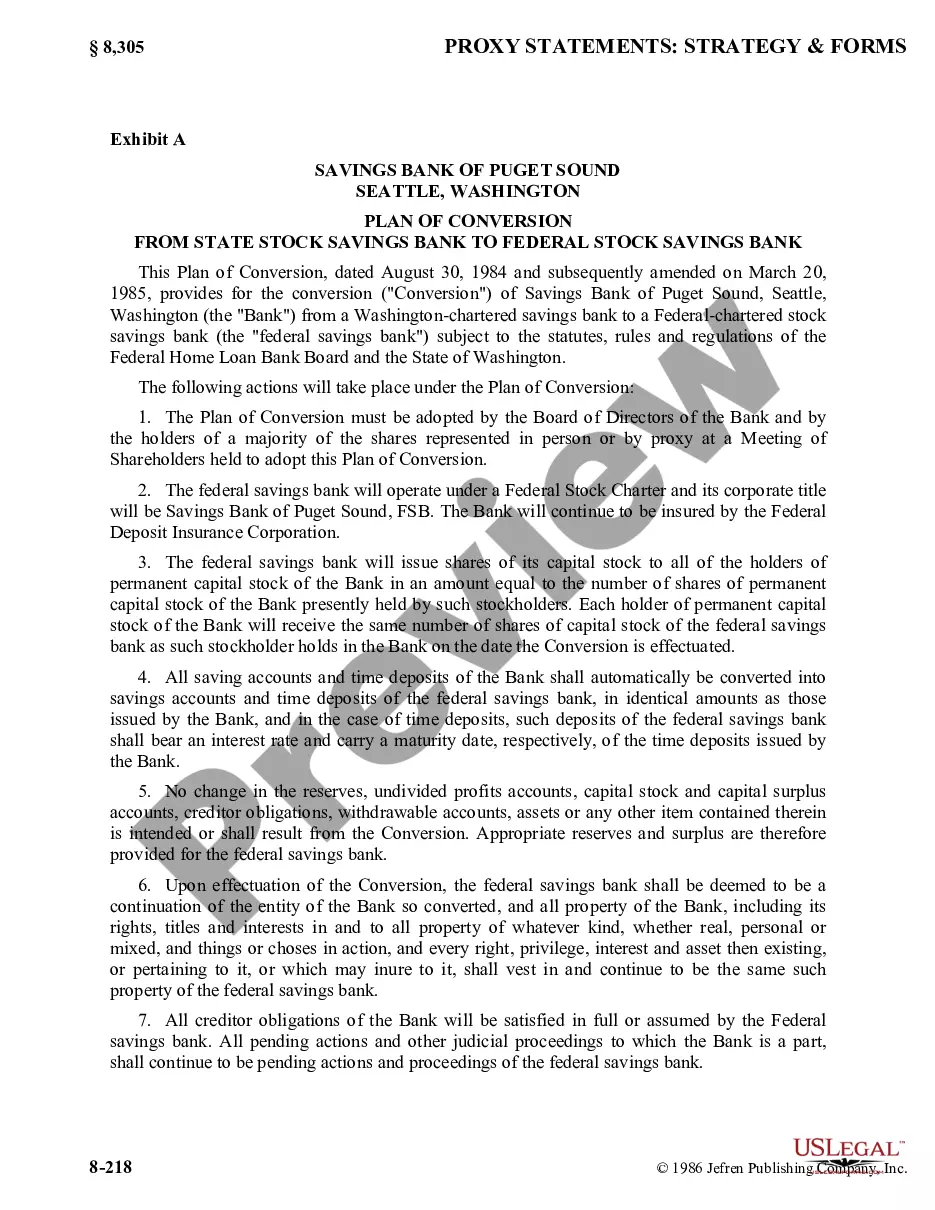

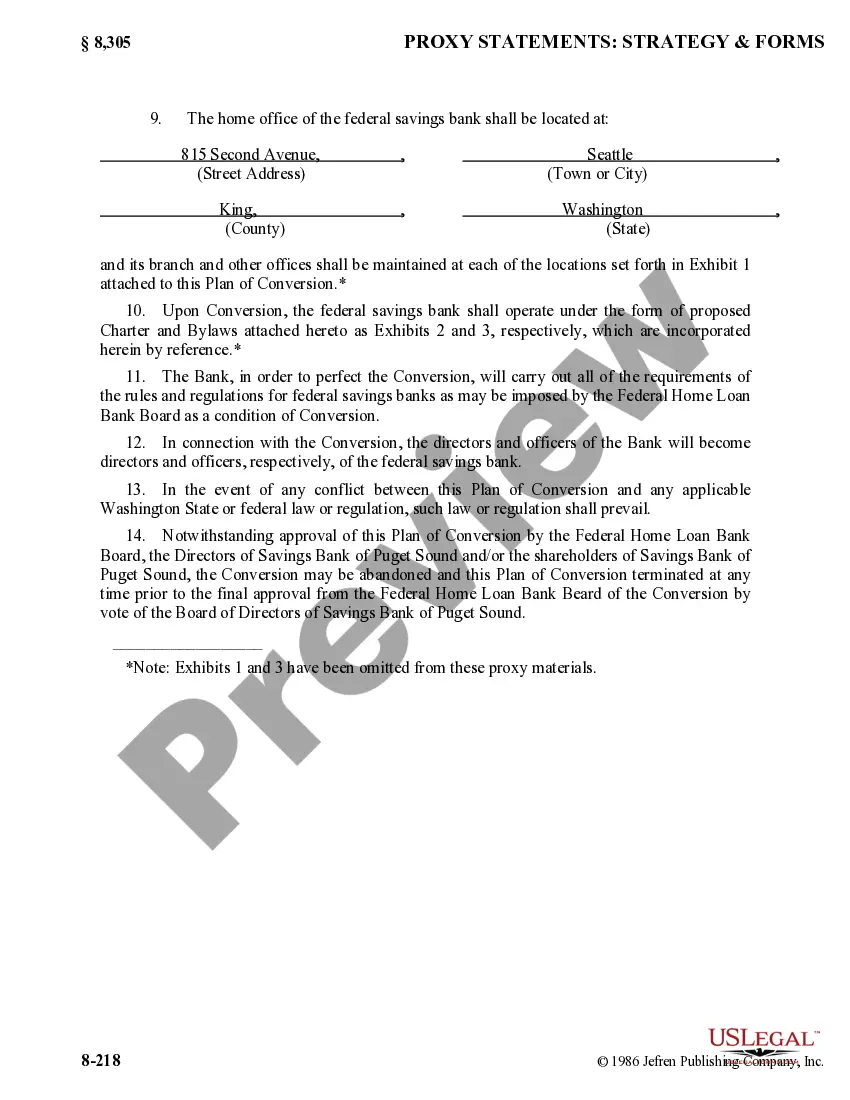

The District of Columbia Plan of Conversion from state stock savings bank to federal stock savings bank refers to the process through which state-chartered stock savings banks in the District of Columbia convert to become federally chartered stock savings banks. This conversion allows these institutions to operate under the regulations and framework established by the Federal Deposit Insurance Corporation (FDIC) and the Office of the Comptroller of the Currency (OCC), rather than solely adhering to state banking laws. The District of Columbia Plan of Conversion involves several key steps and considerations. Initially, a state stock savings bank that wishes to convert must submit an application to the OCC requesting approval for the conversion. The application typically includes detailed financial information, business plans, and operating procedures to demonstrate the bank's ability to comply with federal banking requirements. Once the OCC approves the application, the state stock savings bank needs to obtain approval from its board of directors and shareholders to move forward with the conversion process. This often involves drafting and distributing disclosure documents to shareholders to inform them about the conversion and its potential impact on the bank's operations, governance, and shareholder rights. After receiving the necessary approvals, the bank needs to file a certificate of conversion with the District of Columbia Department of Insurance, Securities and Banking (DISC). This certificate officially documents the change in charter and signifies the bank's new status as a federal stock savings bank. Additionally, the bank has to make any necessary changes to its articles of incorporation, bylaws, and other organizational documents to align with federal regulations. The District of Columbia Plan of Conversion aims to ensure a smooth transition for both the bank and its customers. As part of the process, the bank needs to inform its customers about any changes in account terms, services, or fees resulting from the conversion. This helps maintain transparency and allows customers to make informed decisions regarding their banking relationships. It's important to note that there are no specific variations or different types of the District of Columbia Plan of Conversion from state stock savings bank to federal stock savings bank. However, each individual bank's conversion process may vary slightly due to factors such as its organizational structure, size, and shareholder agreements. In summary, the District of Columbia Plan of Conversion from state stock savings bank to federal stock savings bank enables state-chartered stock savings banks in the District of Columbia to transition into federally chartered institutions. This conversion necessitates obtaining approval from regulatory bodies, engaging shareholders, appropriately amending organizational documents, and informing customers. By converting, banks gain access to the benefits and regulations associated with federal oversight by entities like the FDIC and OCC.

District of Columbia Plan of Conversion from state stock savings bank to federal stock savings bank

Description

How to fill out District Of Columbia Plan Of Conversion From State Stock Savings Bank To Federal Stock Savings Bank?

You may spend several hours on-line attempting to find the lawful file format that meets the state and federal needs you require. US Legal Forms offers 1000s of lawful varieties which can be reviewed by pros. It is simple to download or print out the District of Columbia Plan of Conversion from state stock savings bank to federal stock savings bank from our assistance.

If you currently have a US Legal Forms bank account, you are able to log in and click on the Download key. Following that, you are able to total, revise, print out, or sign the District of Columbia Plan of Conversion from state stock savings bank to federal stock savings bank. Each lawful file format you buy is your own for a long time. To obtain another version of any acquired kind, proceed to the My Forms tab and click on the related key.

If you use the US Legal Forms internet site initially, follow the easy directions listed below:

- Initially, make certain you have selected the best file format to the state/area of your choosing. Browse the kind information to ensure you have picked the right kind. If accessible, utilize the Preview key to look with the file format too.

- In order to find another variation from the kind, utilize the Look for industry to discover the format that suits you and needs.

- After you have discovered the format you would like, click on Purchase now to proceed.

- Select the prices plan you would like, type in your credentials, and sign up for a merchant account on US Legal Forms.

- Comprehensive the deal. You can use your credit card or PayPal bank account to purchase the lawful kind.

- Select the format from the file and download it for your product.

- Make adjustments for your file if required. You may total, revise and sign and print out District of Columbia Plan of Conversion from state stock savings bank to federal stock savings bank.

Download and print out 1000s of file templates making use of the US Legal Forms site, which provides the biggest selection of lawful varieties. Use skilled and state-specific templates to deal with your company or personal needs.