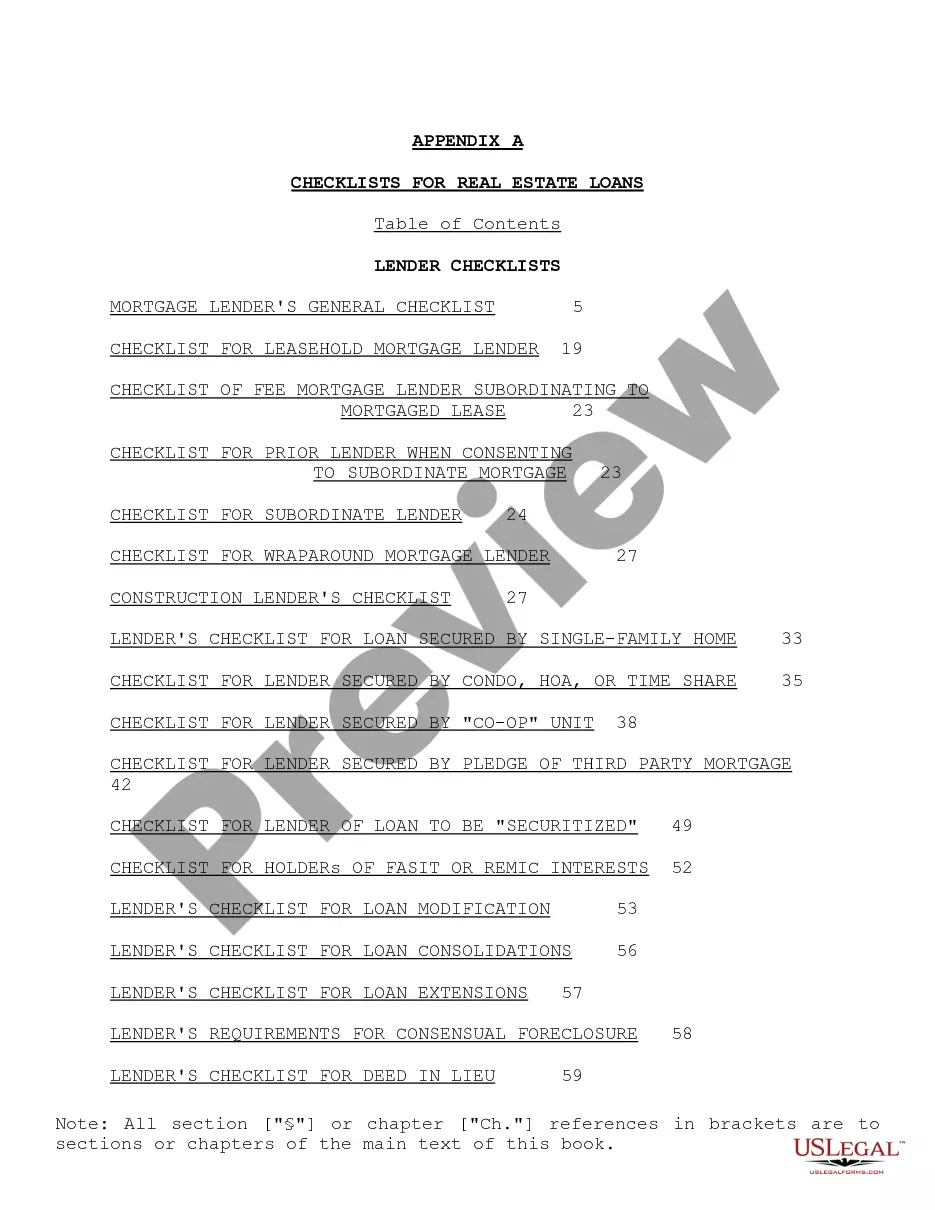

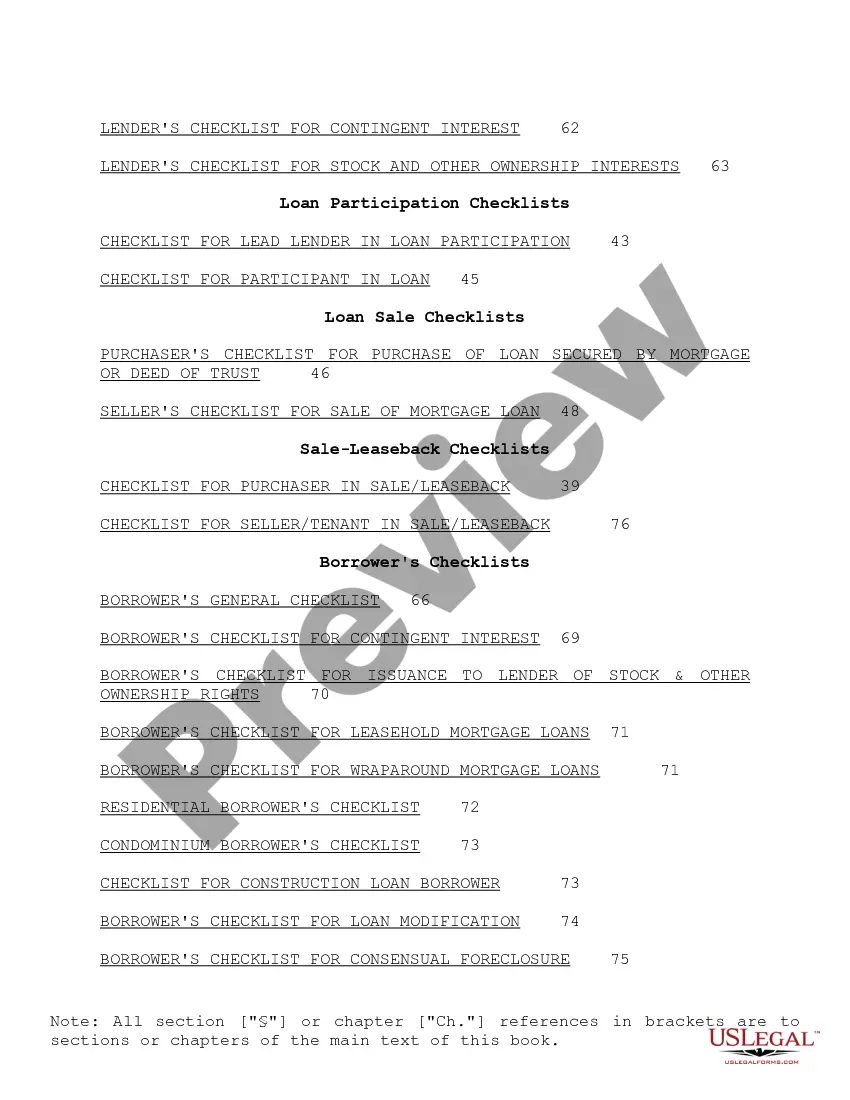

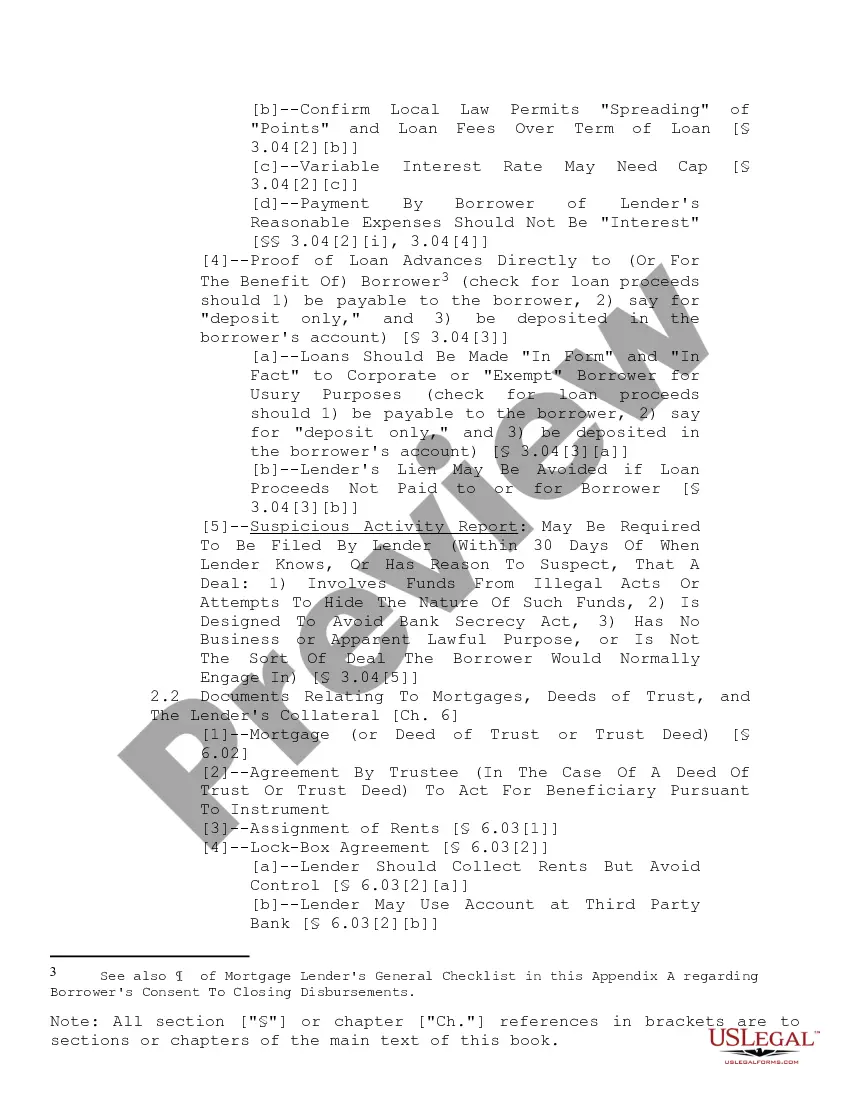

"Checklist for Real Estate Loans" is a American Lawyer Media form. This consist of many checklist that can be used for real estate loans.

District of Columbia Checklist for Real Estate Loans: A Comprehensive Guide Keywords: District of Columbia, real estate loans, checklist, types Introduction: If you are considering applying for a real estate loan in the District of Columbia (D.C.), it is essential to have a thorough understanding of the specific requirements and checklist associated with the process. This detailed guide will outline the essential documents and steps you need to follow when applying for various types of real estate loans in the D.C. area. Whether it's a conventional mortgage, FHA loan, or VA loan, we've got you covered. 1. Conventional Mortgage Checklist: Obtaining a conventional mortgage in the District of Columbia requires meticulous preparation. Ensure you check off these crucial items: — Completed loan application form, which includes personal and financial information — Proof of employment, such as pay stubs or tax returns — Bank statements showing your financial stability and ability to repay the loan — Credit report to evaluate your creditworthiness — Appraisal report to determine the property's value — Loan estimate, detailing the terms, interest rate, and associated costs — Title insurance to protect your property rights — Homeowner's insurance, which is required for most conventional mortgage loans 2. FHA Loan Checklist: Federal Housing Administration (FHA) loans are government-backed programs designed to make homeownership more accessible. When applying for an FHA loan in D.C., remember these key documents: — FHA loan application, capturing personal and financial details — Employment verification, including recent pay stubs or tax returns — Bank statements to demonstrate financial stability — Credit report to ascertain creditworthiness — Property appraisal to determine its value and eligibility for FHA financing — FHA loan estimate, outlining the loan terms, mortgage insurance, and associated fees — Homeowner's insuranccoverageag— - Title insurance to protect your investment 3. VA Loan Checklist: For veterans, active-duty military personnel, and their families, applying for a VA loan can be an excellent option. Here's a checklist specific to D.C. for securing a VA loan: — VA loan application, providing necessary personal and military service information — Certificate of Eligibility (COE) from the VA or DD Form 214 for veterans — Proof of employment or income, including pay stubs or tax returns — Bank statements to demonstrate financial stability — Credit report to assess creditworthiness — VA appraisal report to determine the property's value and eligibility for VA financing — Loan estimate, outlining the terms, interest rate, and related costs — Homeowner's insurance as required by the VA — Title insurance to safeguard your investment Conclusion: Acquiring a real estate loan in the District of Columbia, whether it be a conventional mortgage, FHA loan, or VA loan, demands attention to detail and proper documentation. By following the respective checklists provided for each loan type, you can streamline the application process and increase your chances of securing your dream home in this vibrant and historical region. Be sure to consult with a trusted lender or mortgage professional who can guide you through the specifics of your loan application and help you make informed decisions.District of Columbia Checklist for Real Estate Loans: A Comprehensive Guide Keywords: District of Columbia, real estate loans, checklist, types Introduction: If you are considering applying for a real estate loan in the District of Columbia (D.C.), it is essential to have a thorough understanding of the specific requirements and checklist associated with the process. This detailed guide will outline the essential documents and steps you need to follow when applying for various types of real estate loans in the D.C. area. Whether it's a conventional mortgage, FHA loan, or VA loan, we've got you covered. 1. Conventional Mortgage Checklist: Obtaining a conventional mortgage in the District of Columbia requires meticulous preparation. Ensure you check off these crucial items: — Completed loan application form, which includes personal and financial information — Proof of employment, such as pay stubs or tax returns — Bank statements showing your financial stability and ability to repay the loan — Credit report to evaluate your creditworthiness — Appraisal report to determine the property's value — Loan estimate, detailing the terms, interest rate, and associated costs — Title insurance to protect your property rights — Homeowner's insurance, which is required for most conventional mortgage loans 2. FHA Loan Checklist: Federal Housing Administration (FHA) loans are government-backed programs designed to make homeownership more accessible. When applying for an FHA loan in D.C., remember these key documents: — FHA loan application, capturing personal and financial details — Employment verification, including recent pay stubs or tax returns — Bank statements to demonstrate financial stability — Credit report to ascertain creditworthiness — Property appraisal to determine its value and eligibility for FHA financing — FHA loan estimate, outlining the loan terms, mortgage insurance, and associated fees — Homeowner's insuranccoverageag— - Title insurance to protect your investment 3. VA Loan Checklist: For veterans, active-duty military personnel, and their families, applying for a VA loan can be an excellent option. Here's a checklist specific to D.C. for securing a VA loan: — VA loan application, providing necessary personal and military service information — Certificate of Eligibility (COE) from the VA or DD Form 214 for veterans — Proof of employment or income, including pay stubs or tax returns — Bank statements to demonstrate financial stability — Credit report to assess creditworthiness — VA appraisal report to determine the property's value and eligibility for VA financing — Loan estimate, outlining the terms, interest rate, and related costs — Homeowner's insurance as required by the VA — Title insurance to safeguard your investment Conclusion: Acquiring a real estate loan in the District of Columbia, whether it be a conventional mortgage, FHA loan, or VA loan, demands attention to detail and proper documentation. By following the respective checklists provided for each loan type, you can streamline the application process and increase your chances of securing your dream home in this vibrant and historical region. Be sure to consult with a trusted lender or mortgage professional who can guide you through the specifics of your loan application and help you make informed decisions.