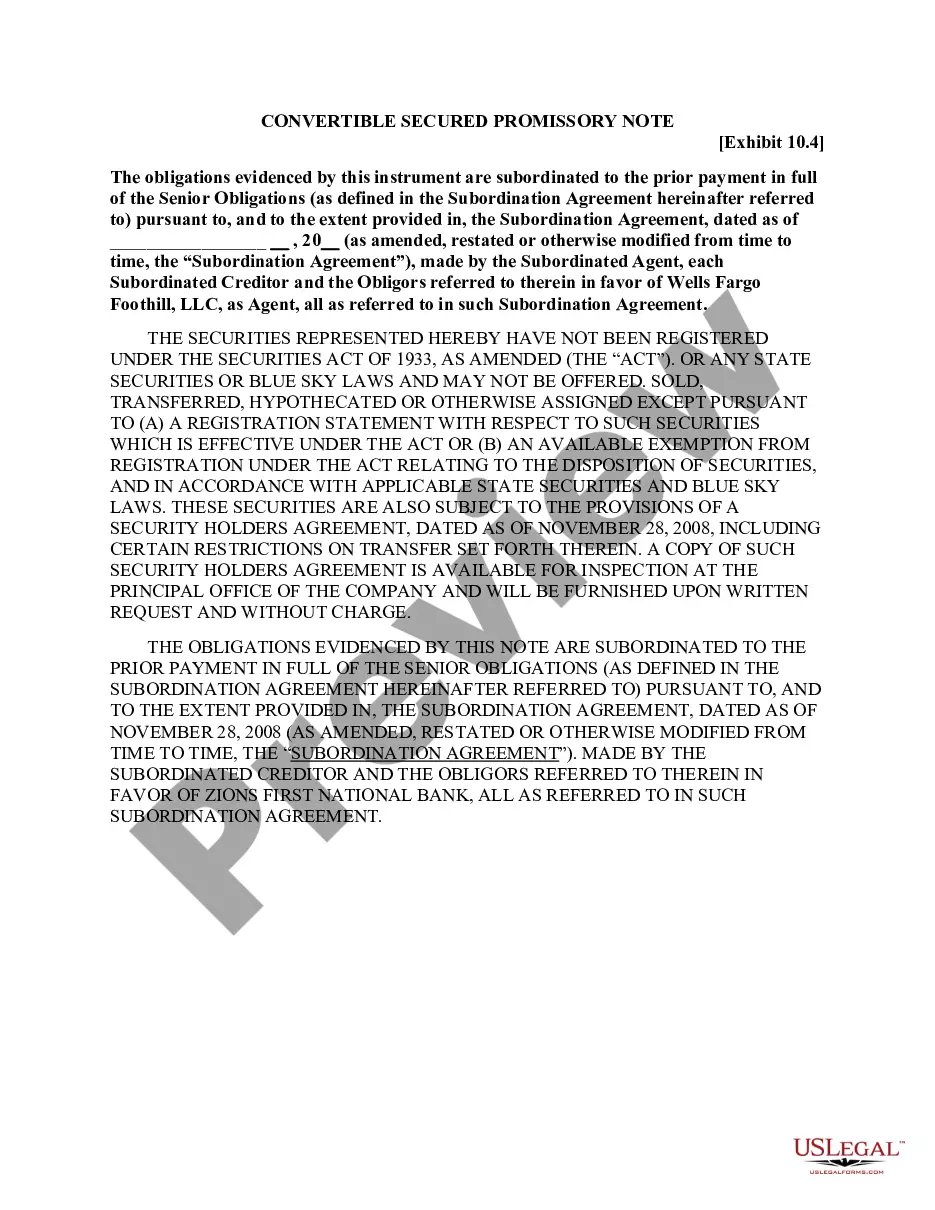

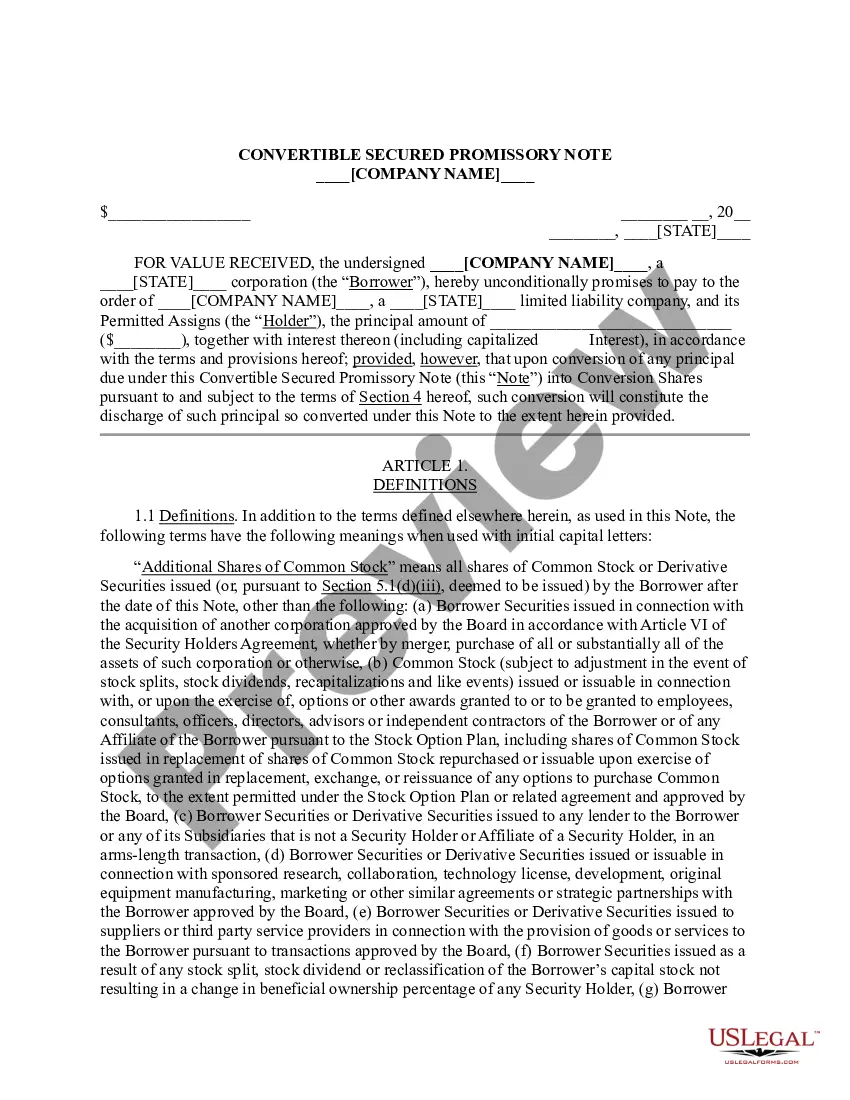

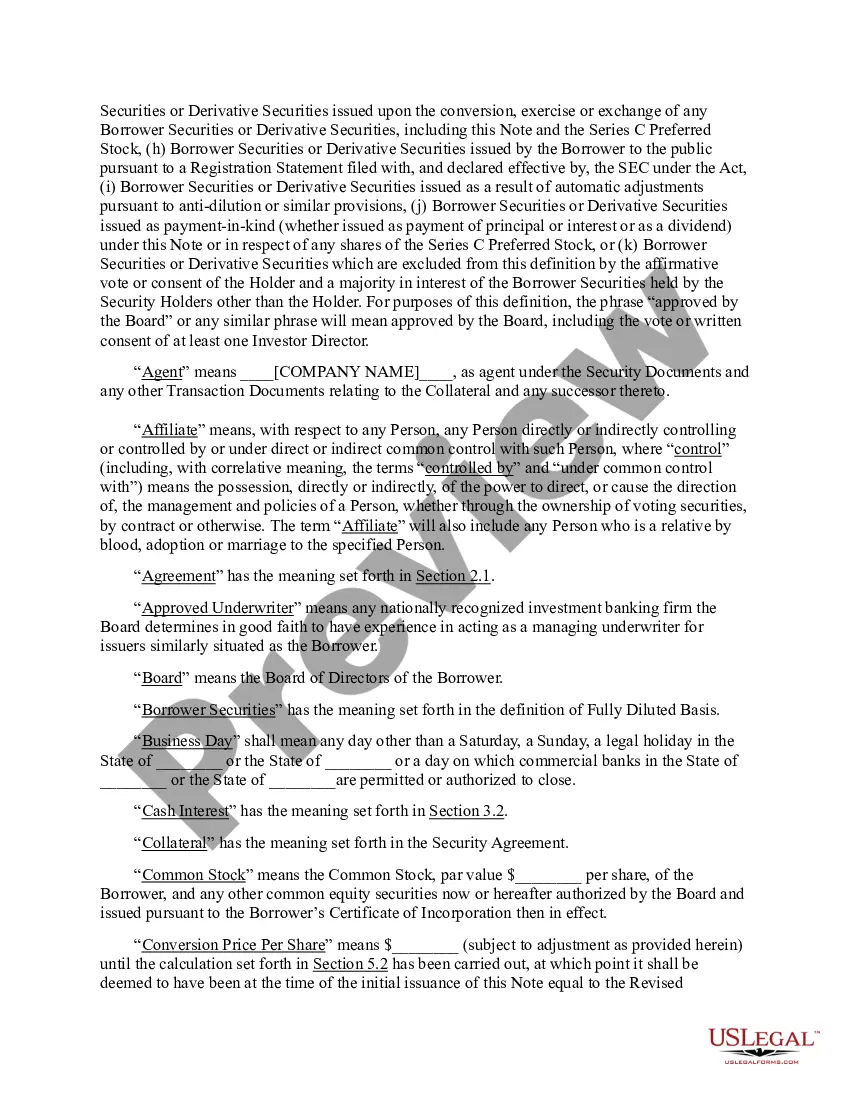

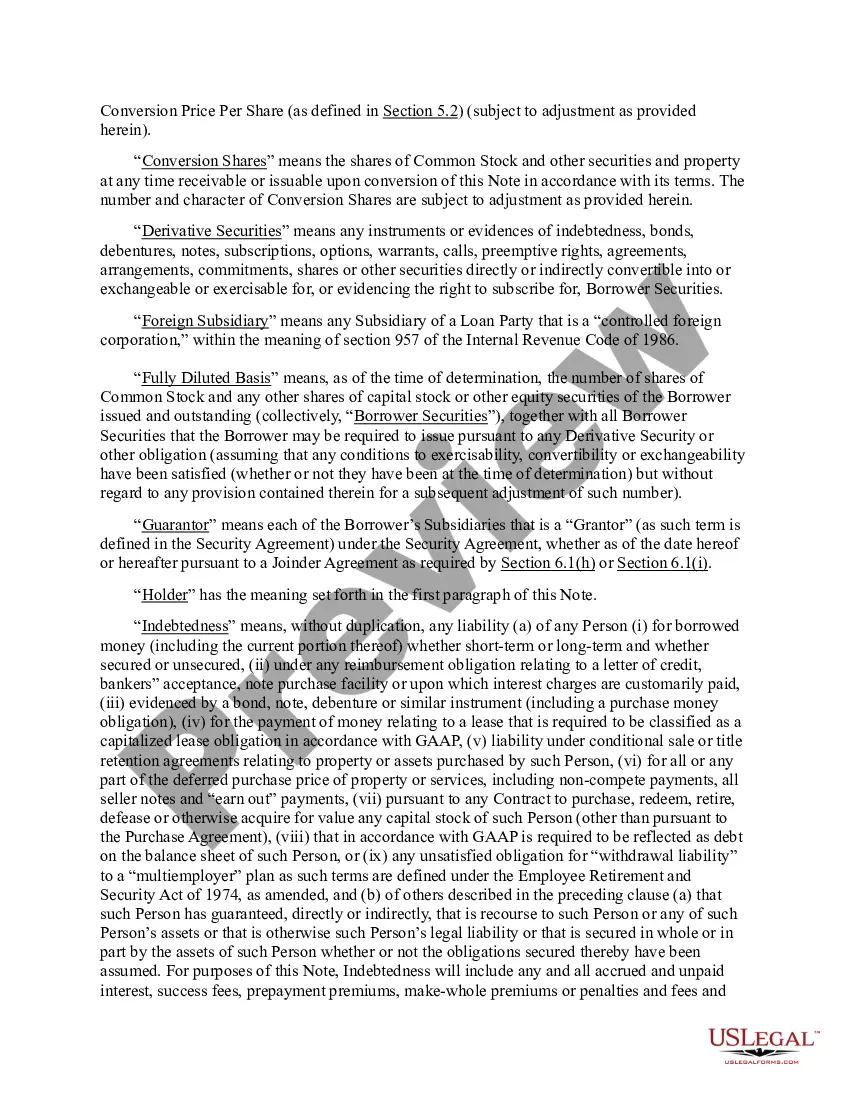

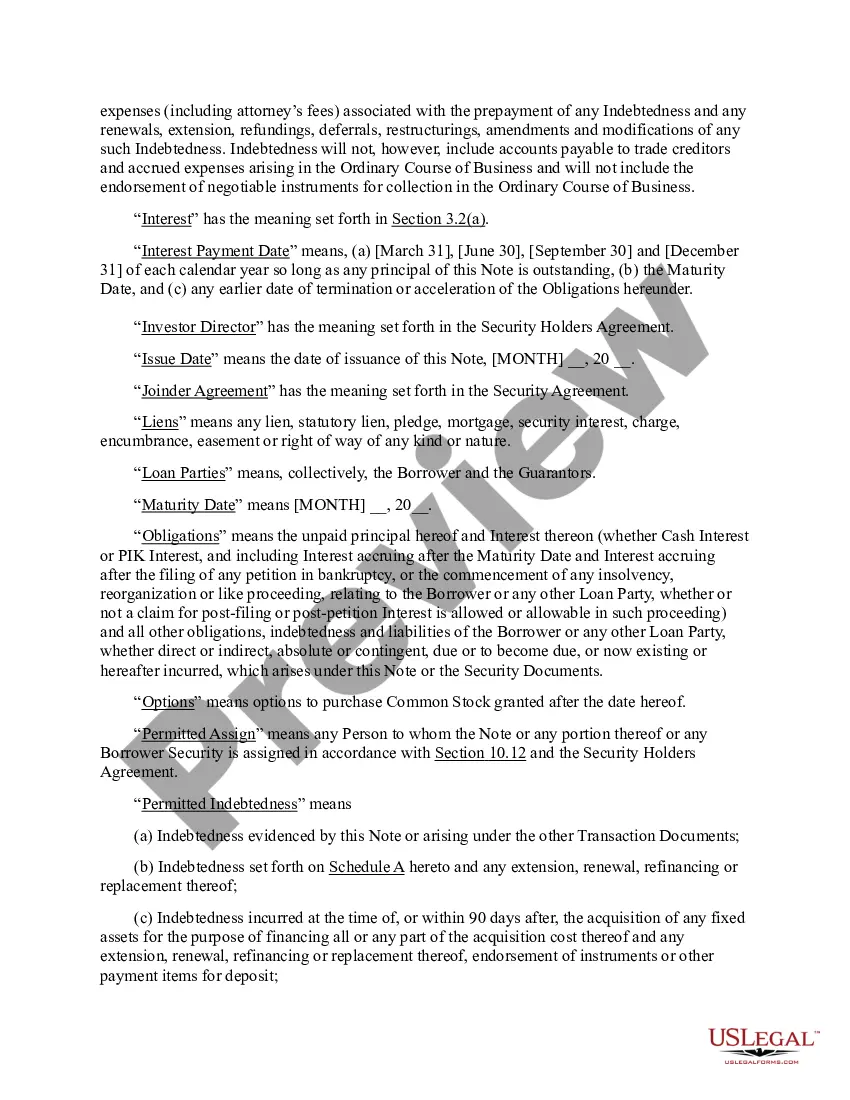

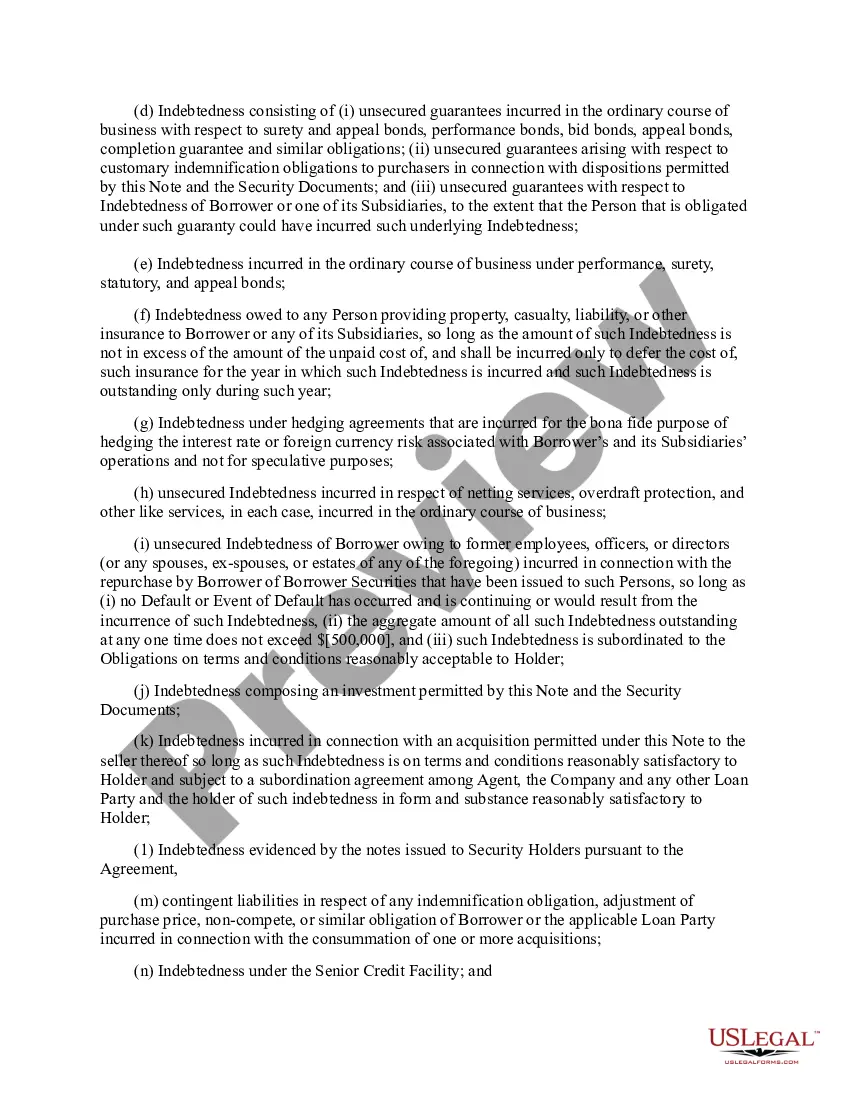

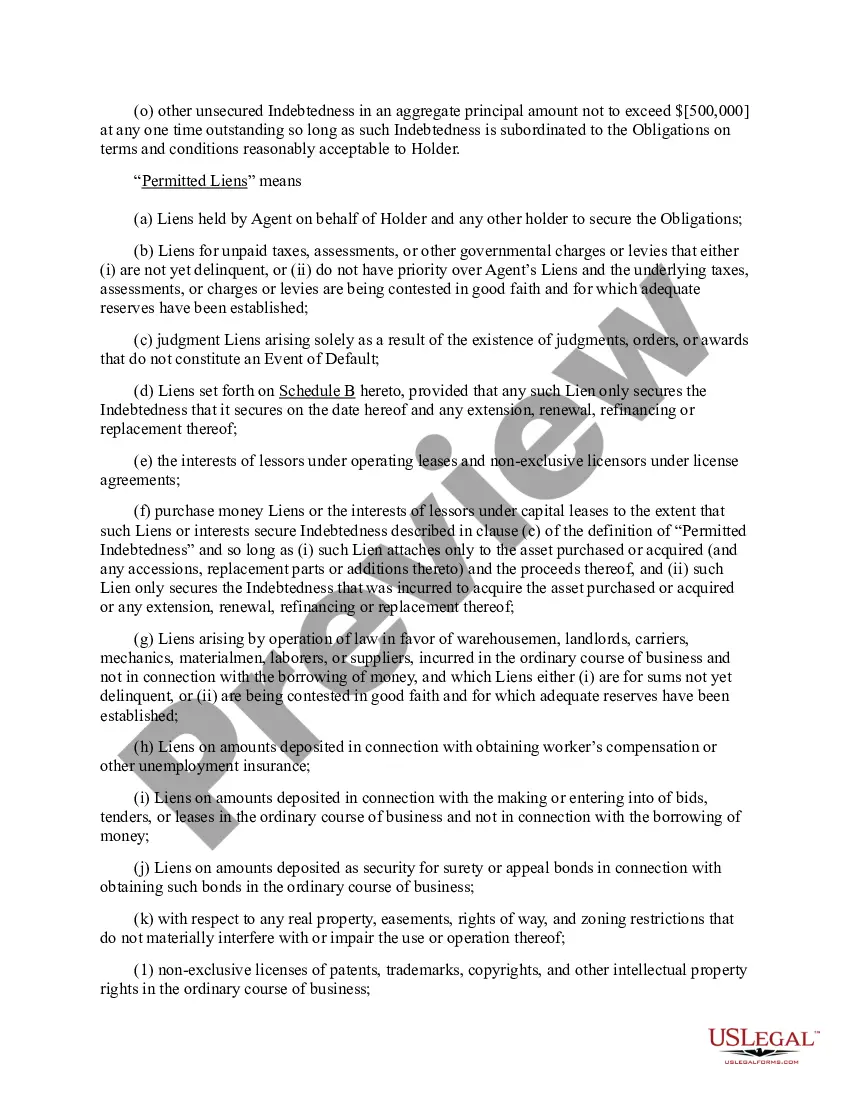

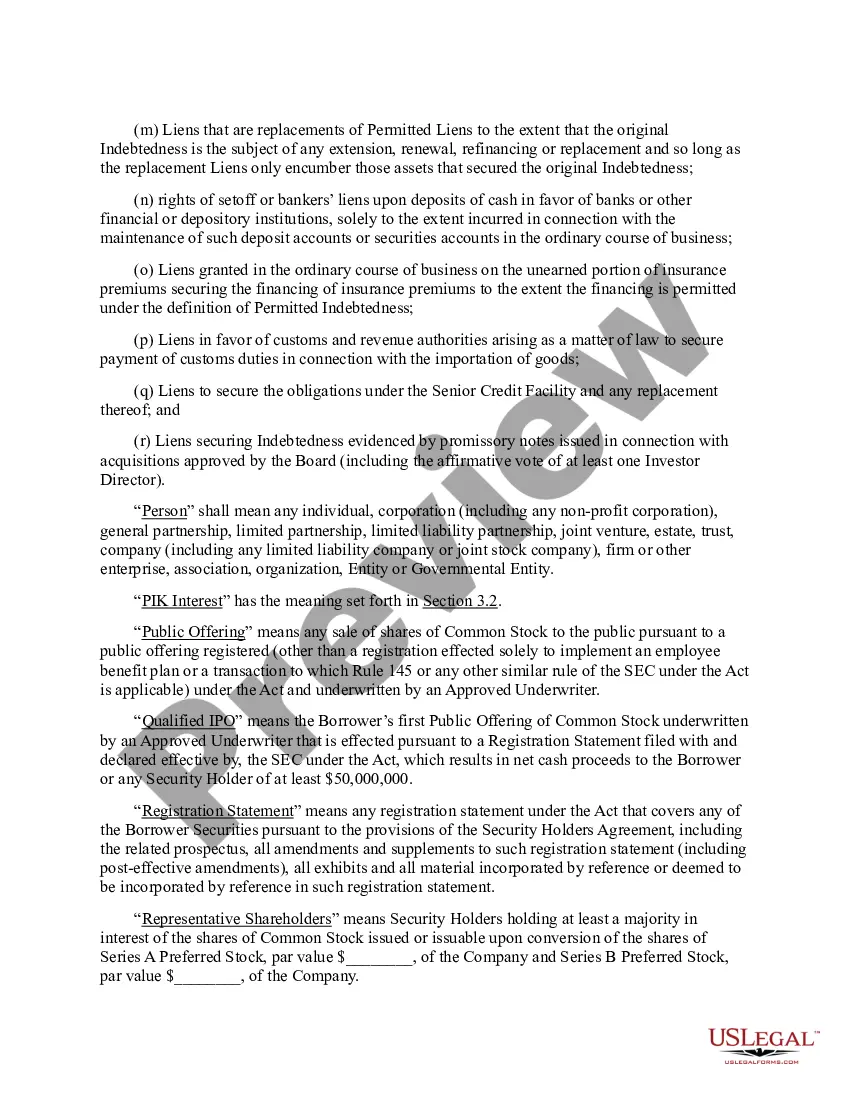

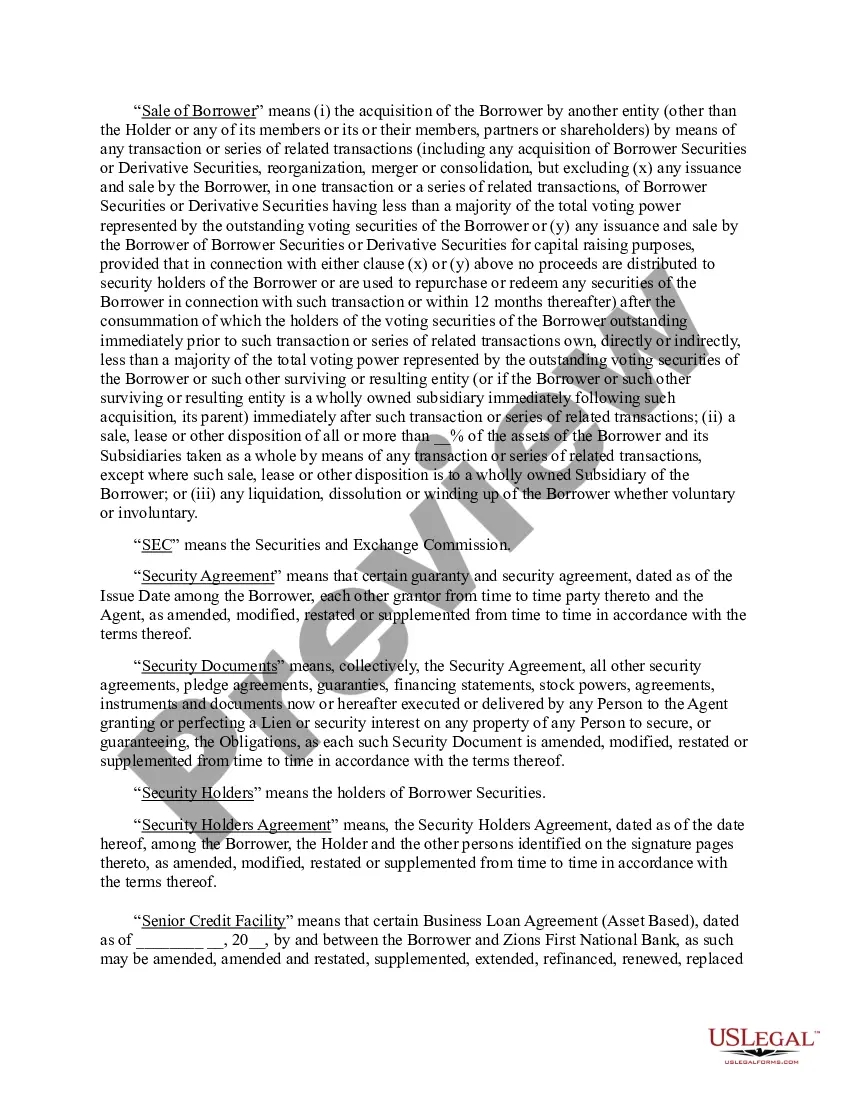

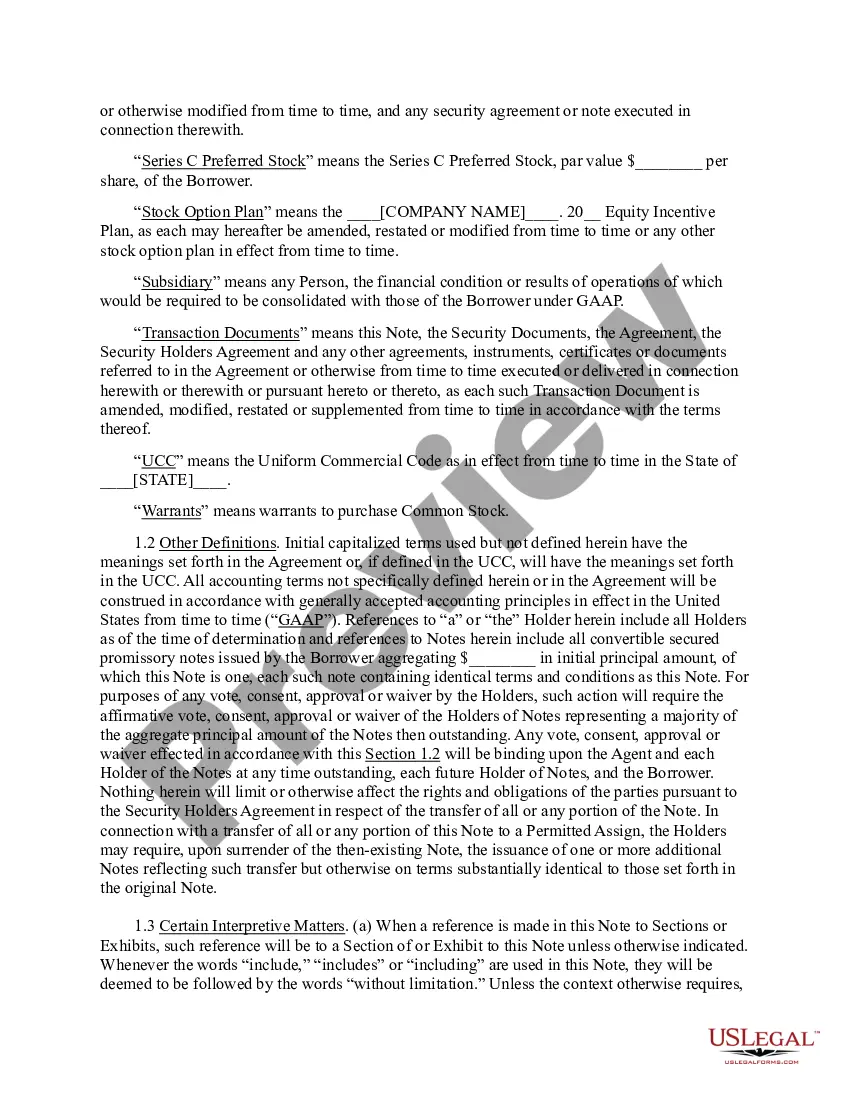

A District of Columbia Convertible Secured Promissory Note is a legal document that outlines the terms and conditions of a loan agreement between a lender and a borrower in the District of Columbia (DC). This type of promissory note provides security to the lender by incorporating a convertible feature that allows the lender to convert the outstanding balance into equity or ownership interest in the borrower's company or asset. A District of Columbia Convertible Secured Promissory Note typically includes key information such as the names and addresses of both parties, the principal amount being loaned, the interest rate, repayment terms, and maturity date. It also defines the collateral that secures the loan, which can be in the form of real estate, accounts receivables, inventory, or any other valuable asset. There are different types of District of Columbia Convertible Secured Promissory Notes based on their specific features and conditions: 1. Traditional Convertible Secured Promissory Note: This type allows the lender to convert the outstanding loan amount into equity or ownership interest in the borrower's company at a predetermined conversion rate or price. 2. Asset-Backed Convertible Secured Promissory Note: In this case, the promissory note is secured by specific assets, such as real estate or equipment. If the borrower defaults on the loan, the lender can seize these assets to recover their investment. 3. Convertible Secured Promissory Note with Warrant: This variation includes the issuance of warrants along with the loan. The lender can exercise these warrants to purchase additional equity or ownership interest in the borrower's company within a specified time frame and at a predetermined price. 4. Convertible Secured Promissory Note with Discount: This type provides the lender with a discounted price on the conversion of the loan amount into equity. It incentivizes early conversion and offers the lender a more favorable deal. 5. Convertible Secured Promissory Note with Cap: This version sets a maximum valuation or ownership percentage for the conversion, ensuring that the lender's equity interest doesn't exceed a predetermined cap, regardless of the company's actual value. It is essential for both the lender and borrower to consult with legal professionals familiar with DC laws and regulations to ensure their District of Columbia Convertible Secured Promissory Note is legally sound and accurately represents their intentions.

District of Columbia Convertible Secured Promissory Note

Description

How to fill out District Of Columbia Convertible Secured Promissory Note?

Discovering the right legal papers design can be quite a struggle. Needless to say, there are a lot of themes accessible on the Internet, but how can you find the legal kind you need? Take advantage of the US Legal Forms site. The services provides thousands of themes, such as the District of Columbia Convertible Secured Promissory Note, which you can use for business and private requirements. Every one of the types are inspected by experts and meet up with state and federal specifications.

When you are presently signed up, log in to the accounts and then click the Down load button to obtain the District of Columbia Convertible Secured Promissory Note. Use your accounts to search with the legal types you might have acquired formerly. Go to the My Forms tab of your own accounts and obtain another backup of your papers you need.

When you are a fresh customer of US Legal Forms, allow me to share basic recommendations so that you can adhere to:

- Initially, make certain you have selected the correct kind for the city/county. It is possible to look through the form making use of the Review button and read the form outline to make sure this is basically the right one for you.

- In case the kind will not meet up with your requirements, utilize the Seach industry to get the right kind.

- When you are positive that the form is suitable, click on the Get now button to obtain the kind.

- Select the pricing strategy you desire and type in the necessary information. Make your accounts and pay money for your order making use of your PayPal accounts or bank card.

- Opt for the submit structure and down load the legal papers design to the gadget.

- Comprehensive, revise and printing and indication the obtained District of Columbia Convertible Secured Promissory Note.

US Legal Forms may be the greatest library of legal types where you can see numerous papers themes. Take advantage of the company to down load expertly-manufactured documents that adhere to condition specifications.

Form popularity

FAQ

A contract for a collateral loan should clearly state what asset(s) are being used to secure the loan and include a clause on what could happen to the asset if the borrower defaults. It should also clearly outline the circumstances under which the collateral could be forfeited to the lender. How to Write a Personal Loan Agreement | LendingTree lendingtree.com ? personal-loan-contracts lendingtree.com ? personal-loan-contracts

What should be included in a Secured Promissory Note? The amount of the loan and how that money may be transferred. All parties involved and their contact information. ... Repayment schedule. ... Any interest on the loan. ... The details of the collateral.

Conversion to Equity - Accounting for Convertible Debt When the note converts, usually during a new funding round, the liability moves to the equity section of the balance sheet. At this stage, the convertible note is settled, and new equity instruments, typically preferred shares, are issued to the investor.

A secured convertible promissory note, or SCP for short, is a type of security instrument that gives the holder the right to convert their debt into equity in the issuer company. Typically, an SCP will convert at a discount to the market value of the company's shares at the time of conversion.

A Promissory Note may be secured or unsecured. In case of a secured note, the borrower will be required to provide a collateral such as property, goods, services, etc., in the event that they fail to repay the borrowed amount. Promissory Notes - Definition, Types, Elements & Points to Remember bankbazaar.com ? personal-loan ? promisso... bankbazaar.com ? personal-loan ? promisso...

What should be included in a Secured Promissory Note? The amount of the loan and how that money may be transferred. All parties involved and their contact information. ... Repayment schedule. ... Any interest on the loan. ... The details of the collateral. Free Secured Promissory Note Template & FAQs Rocket Lawyer ? ... ? Loans Rocket Lawyer ? ... ? Loans

At its most basic, a promissory note should include the following things: Date. Name of the lender and borrower. Loan amount. Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral? ... Payment amount and frequency. Payment due date. Whether the loan has a cosigner, and if so, who.

What is a Secured Promissory Note? A secured promissory note is an acknowledgment of debt that includes collateral (security) if the borrower defaults. The note will include when the payments are due and, if paid late, the security will be handed over to the lender as a replacement for the amount owed. Free Secured Promissory Note Template - PDF | Word - eForms eForms ? Promissory Note eForms ? Promissory Note