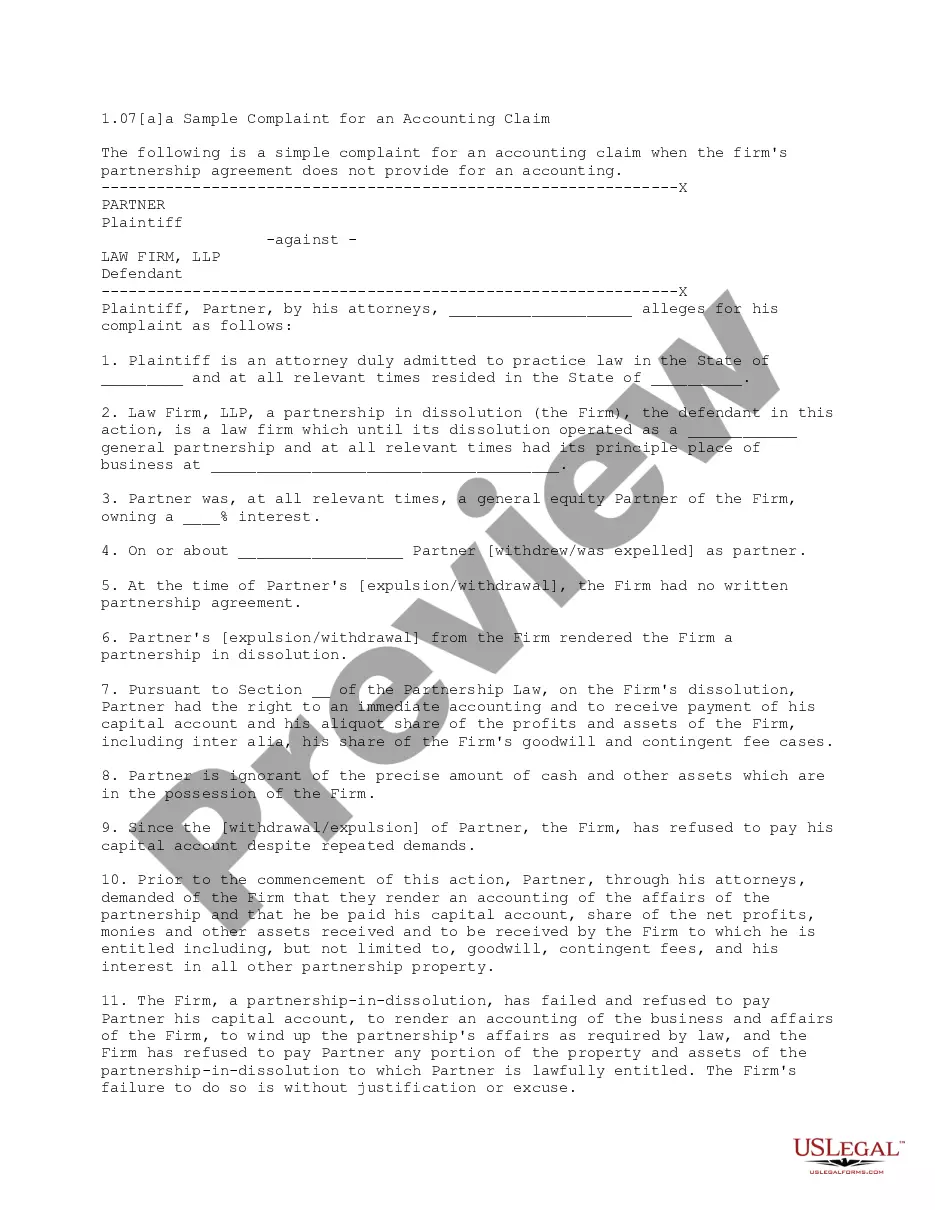

This complaint is for a plaintiff attorney who has been removed from the partnership of his former firm. The complaint requests an accounting of the former firm, stating that the plaintiff has been deprived of economic benefits rightfully due to him under the former partnership agreement, and also alleges egregious acts by his former partners.

District of Columbia Alternative Complaint for an Accounting which includes Egregious Acts

Category:

State:

Multi-State

Control #:

US-L0107A

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Alternative Complaint For An Accounting Which Includes Egregious Acts?

Are you within a placement that you need to have documents for possibly organization or personal purposes nearly every working day? There are tons of lawful file themes available on the Internet, but discovering versions you can rely isn`t easy. US Legal Forms provides 1000s of form themes, much like the District of Columbia Alternative Complaint for an Accounting which includes Egregious Acts, that are composed in order to meet state and federal demands.

When you are previously acquainted with US Legal Forms website and also have your account, just log in. Following that, you may download the District of Columbia Alternative Complaint for an Accounting which includes Egregious Acts design.

Unless you provide an bank account and would like to begin using US Legal Forms, follow these steps:

- Get the form you need and ensure it is for that correct town/county.

- Use the Review button to examine the form.

- Read the description to actually have selected the appropriate form.

- If the form isn`t what you are looking for, make use of the Research area to get the form that suits you and demands.

- Once you discover the correct form, simply click Get now.

- Opt for the rates plan you want, fill out the necessary details to make your money, and pay money for the order with your PayPal or Visa or Mastercard.

- Pick a hassle-free file format and download your duplicate.

Discover every one of the file themes you might have purchased in the My Forms food selection. You can get a more duplicate of District of Columbia Alternative Complaint for an Accounting which includes Egregious Acts whenever, if possible. Just click the necessary form to download or produce the file design.

Use US Legal Forms, the most comprehensive selection of lawful varieties, to save lots of efforts and steer clear of faults. The support provides expertly manufactured lawful file themes that can be used for a selection of purposes. Generate your account on US Legal Forms and initiate creating your life easier.

Form popularity

FAQ

The Office of Adjudication's ruling may be appealed to court within 7 days of notice thereof on the Director, respondent, and complainant. (k)(1)(A) A consumer may bring an action seeking relief from the use of a trade practice in violation of a law of the District.

The District of Columbia's general consumer protection law, which prohibits a wide variety of deceptive and unconscionable business practices, is called the Consumer Protection Procedures Act or ?CPPA.? It is codified at DC Official Code §§ 28-3901 to 28-3913.

A complaint is the pleading that starts a case. Essentially, a document that sets forth a jurisdictional basis for the court's power, the plaintiff's cause of action, and a demand for judicial relief. A plaintiff starts a civil action by filing a pleading called a complaint.

This chapter establishes an enforceable right to truthful information from merchants about consumer goods and services that are or would be purchased, leased, or received in the District of Columbia.

Under D.C. Code § 28-3904, false advertising is an unlawful trade practice.

The law is found in 18 DCMR 2000.2 ?No person shall fail or refuse to comply with any lawful order or direction of any police officer, police cadet, or civilian crossing guard invested by law with authority to direct, control, or regulate traffic.