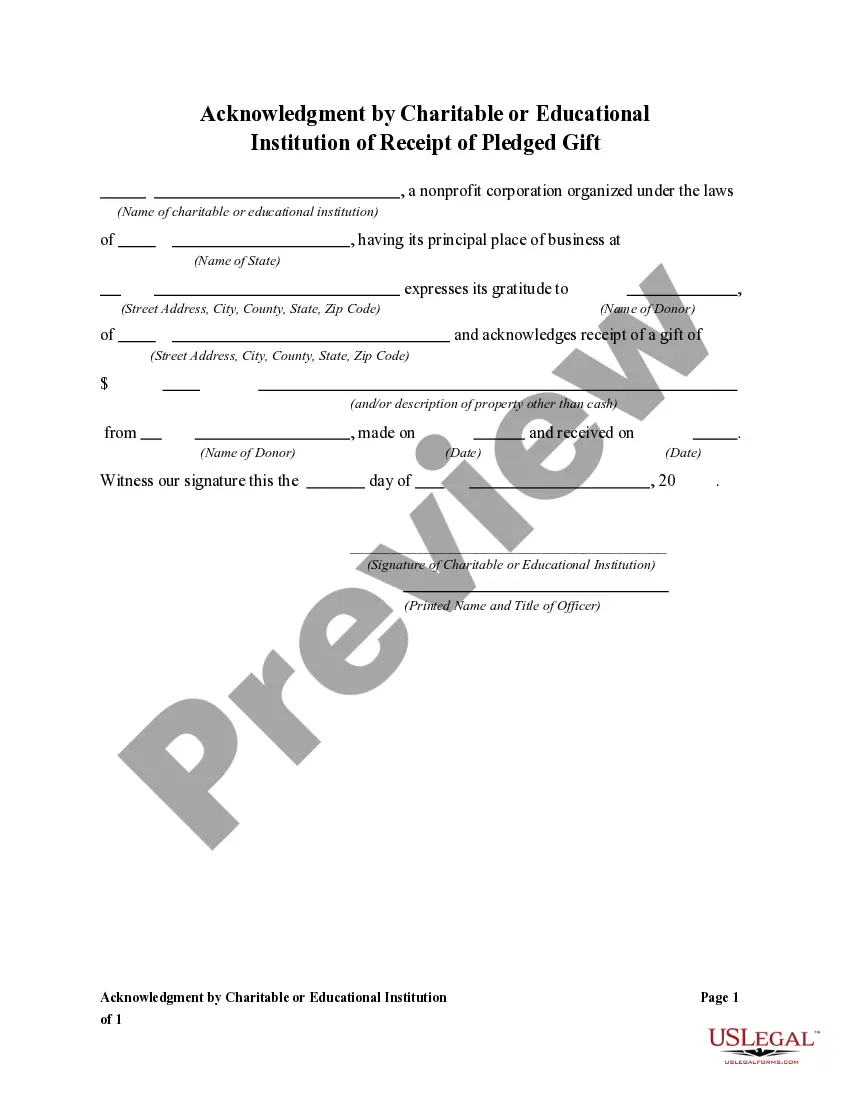

The Delaware Acknowledgment by Charitable or Educational Institution of Receipt of Gift is a document that plays a crucial role in the charitable giving process. It serves as an official acknowledgment by the institution to recognize and verify the donation made to them. This has significant importance for both the donor and the recipient organization, as it helps maintain transparency, compliance, and accountability in the financial transactions involved. The Delaware acknowledgment provides a detailed description of the gift received by the charitable or educational institution. It includes various keywords that are essential for clarity and accuracy in the document. Some relevant keywords to be mentioned in the acknowledgment are: 1. Organization's Details: The acknowledgment should start by clearly stating the name, address, and tax identification number of the charitable or educational institution involved. This information ensures the authenticity of the receiving organization. 2. Donor's Information: The acknowledgment must contain the donor's name, along with their complete contact details. This information helps in identifying and corresponding with the donor if necessary. 3. Gift Description: The document should provide a comprehensive description of the gifted item or contribution. Whether it is a monetary donation, property, securities, stocks, or any other form of gift, it should be clearly stated in the acknowledgment. 4. Fair Market Value: When applicable, the acknowledgment should specify the fair market value of the gift received. This valuation helps both the donor and the institution for tax purposes. 5. Date of Donation: It is crucial to mention the exact date when the gift was received by the institution. This date is essential for tracking and recording purposes. 6. Tax Reducibility: The acknowledgment must mention whether the donation is tax-deductible or not. This information enables the donor to claim a tax deduction, depending on the laws and regulations governing charitable contributions. Types of Delaware Acknowledgment by Charitable or Educational Institution of Receipt of Gift: 1. Monetary Donations: This acknowledgment is used for cash or check donations made by individuals or organizations to a Delaware charitable or educational institution. 2. In-Kind Contributions: This type of acknowledgment is used when non-monetary gifts, such as property, goods, or services, are donated to the institution. 3. Gift of Securities: If a donor contributes stocks, bonds, or other marketable securities, a separate acknowledgment is required to record the specific details related to such gifts. 4. Planned Gifts: Acknowledgments related to planned gifts, including bequests, charitable remainder trusts, or life insurance policies, have their own unique requirements and should be mentioned and recorded separately. It is important for both the donor and the charitable or educational institution to retain a copy of the acknowledgment for their records. The acknowledgment serves as proof of the gift and can be requested by tax authorities for verification purposes.

Delaware Acknowledgment by Charitable or Educational Institution of Receipt of Gift

Description

How to fill out Delaware Acknowledgment By Charitable Or Educational Institution Of Receipt Of Gift?

It is possible to invest hrs on-line searching for the legal papers web template that meets the federal and state needs you will need. US Legal Forms gives a large number of legal types which are reviewed by professionals. You can actually acquire or printing the Delaware Acknowledgment by Charitable or Educational Institution of Receipt of Gift from my assistance.

If you already have a US Legal Forms account, it is possible to log in and then click the Down load switch. Following that, it is possible to total, edit, printing, or sign the Delaware Acknowledgment by Charitable or Educational Institution of Receipt of Gift. Each legal papers web template you acquire is yours forever. To obtain one more backup of any obtained form, proceed to the My Forms tab and then click the related switch.

If you use the US Legal Forms internet site the first time, keep to the easy instructions under:

- First, be sure that you have selected the best papers web template for that county/metropolis of your liking. Browse the form information to make sure you have chosen the correct form. If available, utilize the Preview switch to appear from the papers web template also.

- If you wish to find one more edition of your form, utilize the Lookup field to discover the web template that meets your requirements and needs.

- Once you have found the web template you desire, click Buy now to proceed.

- Select the costs plan you desire, key in your qualifications, and sign up for a merchant account on US Legal Forms.

- Total the financial transaction. You can use your Visa or Mastercard or PayPal account to pay for the legal form.

- Select the formatting of your papers and acquire it to the gadget.

- Make modifications to the papers if needed. It is possible to total, edit and sign and printing Delaware Acknowledgment by Charitable or Educational Institution of Receipt of Gift.

Down load and printing a large number of papers templates utilizing the US Legal Forms site, which offers the largest assortment of legal types. Use professional and condition-distinct templates to handle your company or personal requires.