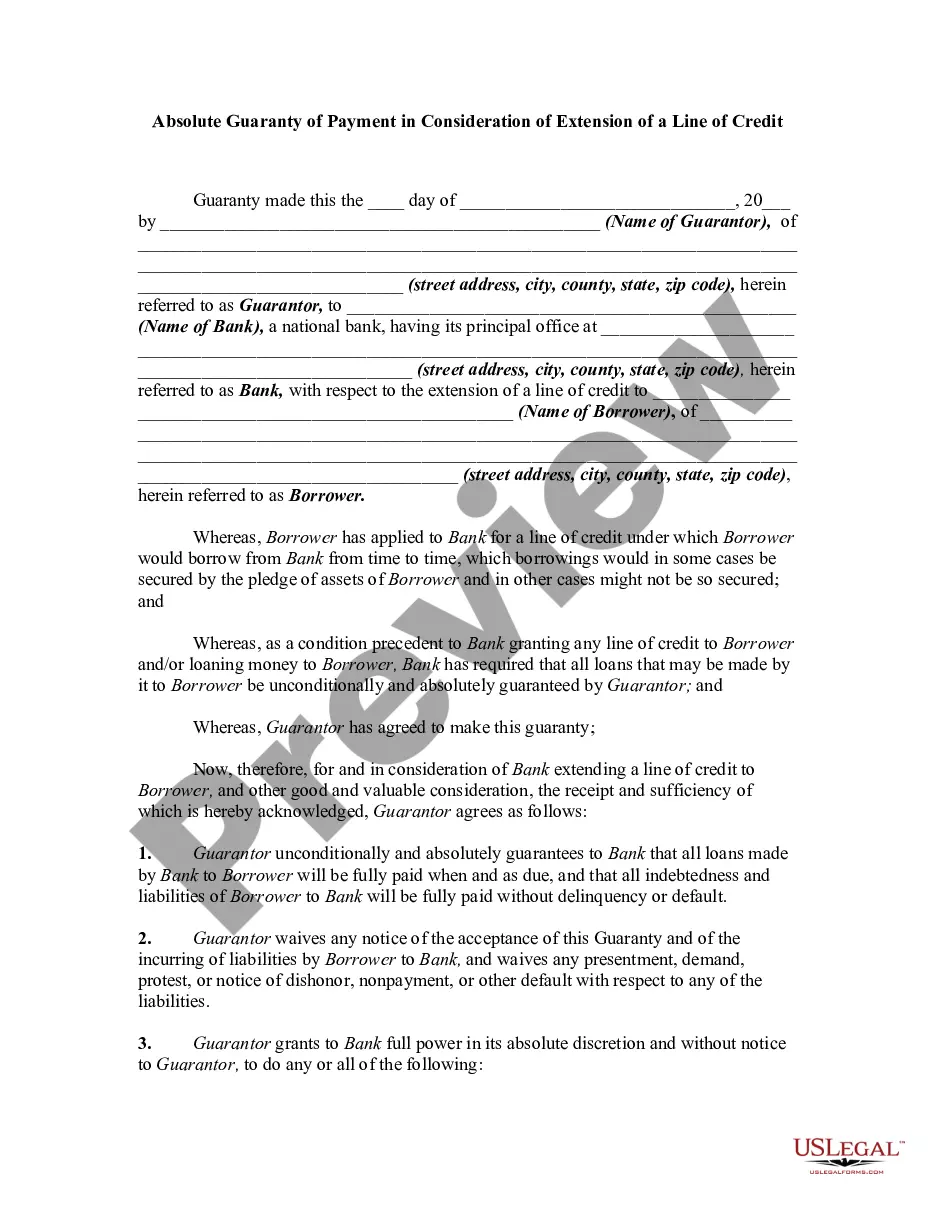

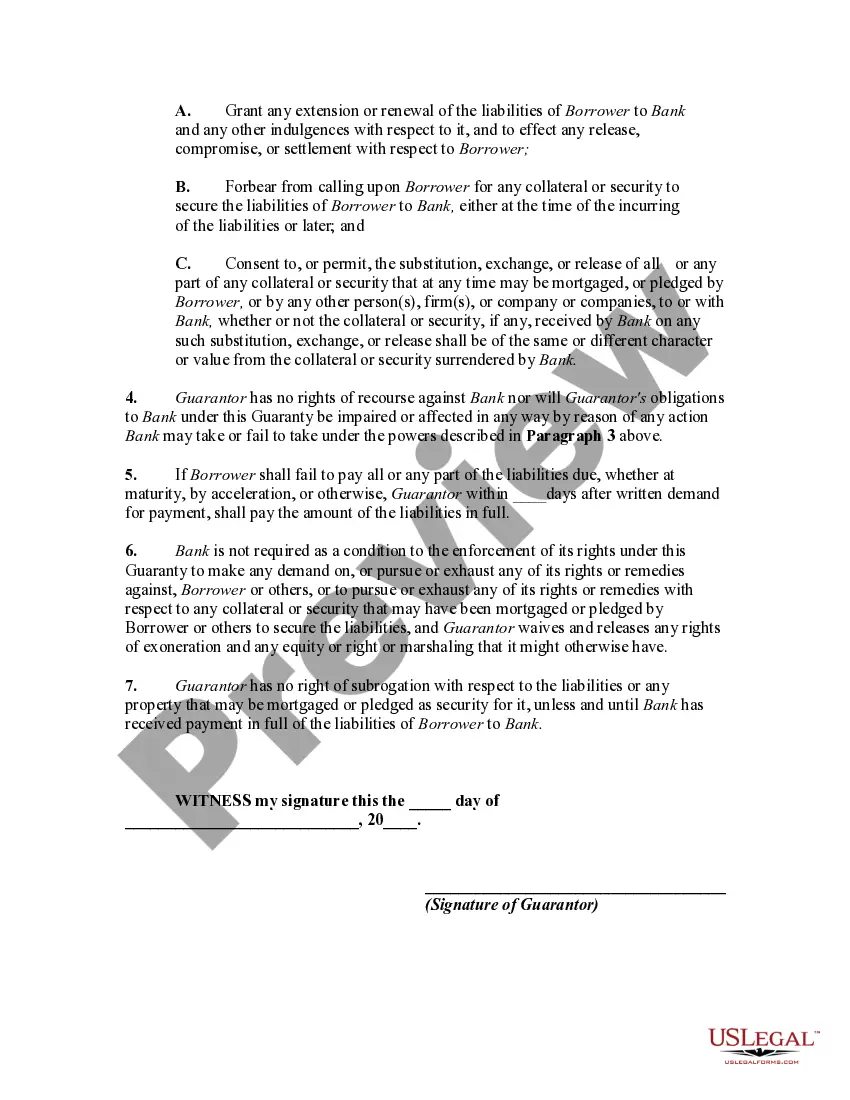

A guaranty is an undertaking on the part of one person (the guarantor) that is collateral to an obligation of another person (the debtor or obligor), and which binds the guarantor to performance of the obligation in the event of default by the debtor or obligor.

The contract of guaranty may be absolute or it may be conditional. An absolute guaranty is a contract by which the guarantor has promised that if the debtor does not perform the obligation or obligations, the guarantor will perform some act (such as the payment of money) to or for the benefit of the creditor.

A line of credit is an arrangement in which a lender extends a specified amount of credit to borrower for a specified time period.

Delaware Absolute Guaranty of Payment in Consideration of Extension of a Line of Credit is a legal document used in commercial transactions to provide assurance of payment for an extended line of credit. This type of guaranty acts as a binding contract between the guarantor and the creditor, ensuring that the guarantor will be held fully responsible for any outstanding debt if the primary borrower defaults on payment. Keywords: Delaware, absolute guaranty of payment, extension of a line of credit, legal document, commercial transactions, assurance of payment, guarantor, creditor, outstanding debt, default on payment. Types of Delaware Absolute Guaranty of Payment in Consideration of Extension of a Line of Credit: 1. Individual Guaranty: This is a type of guaranty where an individual person acts as the guarantor for the line of credit extension. The individual's assets and creditworthiness are evaluated, and they assume personal responsibility for the debt if the borrower fails to repay. 2. Corporate Guaranty: In this type of guaranty, a company or corporation acts as the guarantor for the extended line of credit. The company assumes the liability for the debt, providing an extra layer of security for the creditor. 3. Limited Guaranty: A limited guaranty places restrictions on the guarantor's liability, specifying a maximum limit for which they will be responsible. This type of guaranty protects the guarantor from excessive liability in case of borrower defaults. 4. Continuing Guaranty: A continuing guaranty remains in effect for a specified period, typically until the line of credit is fully repaid or terminated. It provides ongoing protection for the creditor, ensuring payment even if the line of credit is extended or renewed. 5. Joint and Several guaranties: This type of guaranty involves multiple guarantors assuming joint responsibility for the debt. Each guarantor can be held fully liable for the entire debt if the borrower fails to repay, offering additional security to the creditor. 6. Unconditional Guaranty: An unconditional guaranty provides absolute assurance to the creditor that the guarantor will pay the debt in full, regardless of any circumstances. It eliminates any contingency or condition that might excuse the guarantor from fulfilling their obligation. In conclusion, the Delaware Absolute Guaranty of Payment in Consideration of Extension of a Line of Credit is a vital legal document that ensures payment for a line of credit extension. Understanding the different types of guaranties available can help borrowers, guarantors, and creditors establish the appropriate level of protection and responsibility in their credit arrangements.Delaware Absolute Guaranty of Payment in Consideration of Extension of a Line of Credit is a legal document used in commercial transactions to provide assurance of payment for an extended line of credit. This type of guaranty acts as a binding contract between the guarantor and the creditor, ensuring that the guarantor will be held fully responsible for any outstanding debt if the primary borrower defaults on payment. Keywords: Delaware, absolute guaranty of payment, extension of a line of credit, legal document, commercial transactions, assurance of payment, guarantor, creditor, outstanding debt, default on payment. Types of Delaware Absolute Guaranty of Payment in Consideration of Extension of a Line of Credit: 1. Individual Guaranty: This is a type of guaranty where an individual person acts as the guarantor for the line of credit extension. The individual's assets and creditworthiness are evaluated, and they assume personal responsibility for the debt if the borrower fails to repay. 2. Corporate Guaranty: In this type of guaranty, a company or corporation acts as the guarantor for the extended line of credit. The company assumes the liability for the debt, providing an extra layer of security for the creditor. 3. Limited Guaranty: A limited guaranty places restrictions on the guarantor's liability, specifying a maximum limit for which they will be responsible. This type of guaranty protects the guarantor from excessive liability in case of borrower defaults. 4. Continuing Guaranty: A continuing guaranty remains in effect for a specified period, typically until the line of credit is fully repaid or terminated. It provides ongoing protection for the creditor, ensuring payment even if the line of credit is extended or renewed. 5. Joint and Several guaranties: This type of guaranty involves multiple guarantors assuming joint responsibility for the debt. Each guarantor can be held fully liable for the entire debt if the borrower fails to repay, offering additional security to the creditor. 6. Unconditional Guaranty: An unconditional guaranty provides absolute assurance to the creditor that the guarantor will pay the debt in full, regardless of any circumstances. It eliminates any contingency or condition that might excuse the guarantor from fulfilling their obligation. In conclusion, the Delaware Absolute Guaranty of Payment in Consideration of Extension of a Line of Credit is a vital legal document that ensures payment for a line of credit extension. Understanding the different types of guaranties available can help borrowers, guarantors, and creditors establish the appropriate level of protection and responsibility in their credit arrangements.