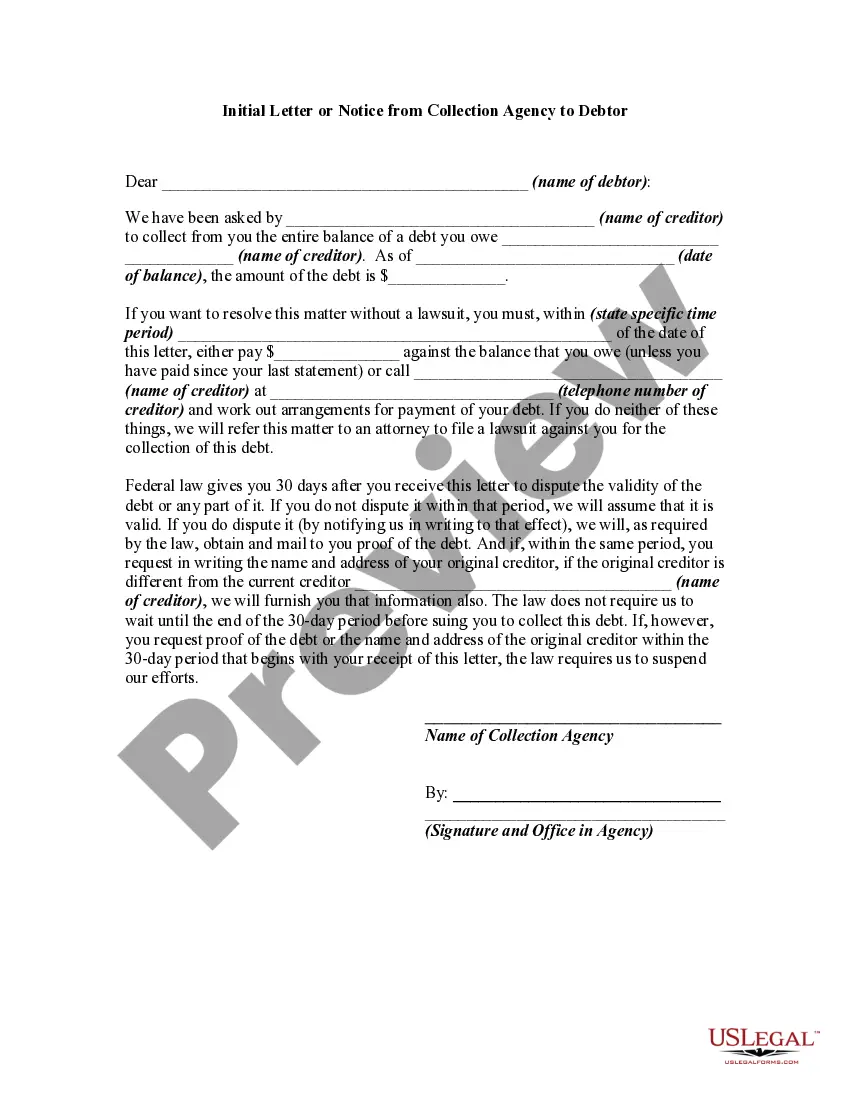

The Fair Debt Collection Practices Act (FDCPA) prohibits harassment or abuse in collecting a debt such as threatening violence, use of obscene or profane language, publishing lists of debtors who refuse to pay debts, or even harassing a debtor by repeatedly calling the debtor on the phone. Also, certain false or misleading representa?¬tions are forbidden, such as representing that the debt collector is associated with the state or federal government, or stating that the debtor will go to jail if he does not pay the debt. This Act also sets out strict rules regarding communicating with the debtor.

The FDCPA applies only to those who regularly engage in the business of collecting debts for others -- primarily to collection agencies. The Act does not apply when a creditor attempts to collect debts owed to it by directly contacting the debtors. It applies only to the collection of consumer debts and does not apply to the collection of commercial debts. Consumer debts are debts for personal, home, or family purposes.

Title: Delaware Initial Letter or Notice from Collection Agency to Debtor — A Comprehensive Guide Introduction: In Delaware, when a debtor falls behind on their payments, a collection agency may initiate the debt recovery process by sending an initial letter or notice. This letter serves as an important communication tool between the collection agency and the debtor. In this article, we will delve into the details of what a Delaware initial letter or notice entails, its purpose, and highlight any variations that may exist. Key Points: 1. Purpose of the Delaware Initial Letter or Notice: The primary objective of a Delaware initial letter or notice from a collection agency is to inform and educate the debtor about their outstanding debt. It serves as a formal communication, acting as the initial attempt to contact the debtor, providing essential details about the debt, the collection agency, and the debtor's rights. 2. Contents of the Letter: A typical initial letter or notice in Delaware includes the following key elements: a. Introduction: An introductory section stating the purpose of the letter and the collection agency's contact information. b. Debt Information: A clear and concise description of the debt, including the account number, original creditor, outstanding balance, and details of any interest or additional fees. c. Verification Rights: A statement informing the debtor about their rights to request verification of the debt within a specific timeframe, usually 30 days. d. Contact Information: The collection agency's contact details, including phone numbers, mailing address, and any instructions to contact them regarding the debt. e. Dispute Process: Informing the debtor of their right to dispute the debt in writing, along with instructions on how to do so. f. Consequences of Non-Payment: A section outlining the potential consequences of not taking immediate action, such as legal action or credit reporting. 3. Types of Delaware Initial Letters or Notices: While the content mentioned above forms the foundation of any initial letter or notice, there may be slight variations depending on the specific circumstances or the collection agency. Some examples of Delaware initial letters or notices include: a. Personal Debt Notice: This type of initial letter or notice is directed towards individuals who owe debts, whether from credit cards, loans, medical bills, or other personal obligations. b. Business Debt Notice: When a delinquent debt involves a business entity, the initial letter or notice may include additional details specific to commercial transactions or contracts. c. Student Loan Notice: In cases involving overdue student loan payments, the initial letter or notice could address the unique aspects of student loan debt and provide specific resources for assistance. Conclusion: A Delaware initial letter or notice from a collection agency serves as a crucial communication tool in the debt recovery process. It informs debtors about their outstanding obligations, provides opportunity to verify or dispute the debt, and outlines the potential consequences of non-payment. Understanding the contents and variations of these initial letters or notices can equip debtors with the necessary knowledge to address their financial obligations effectively.