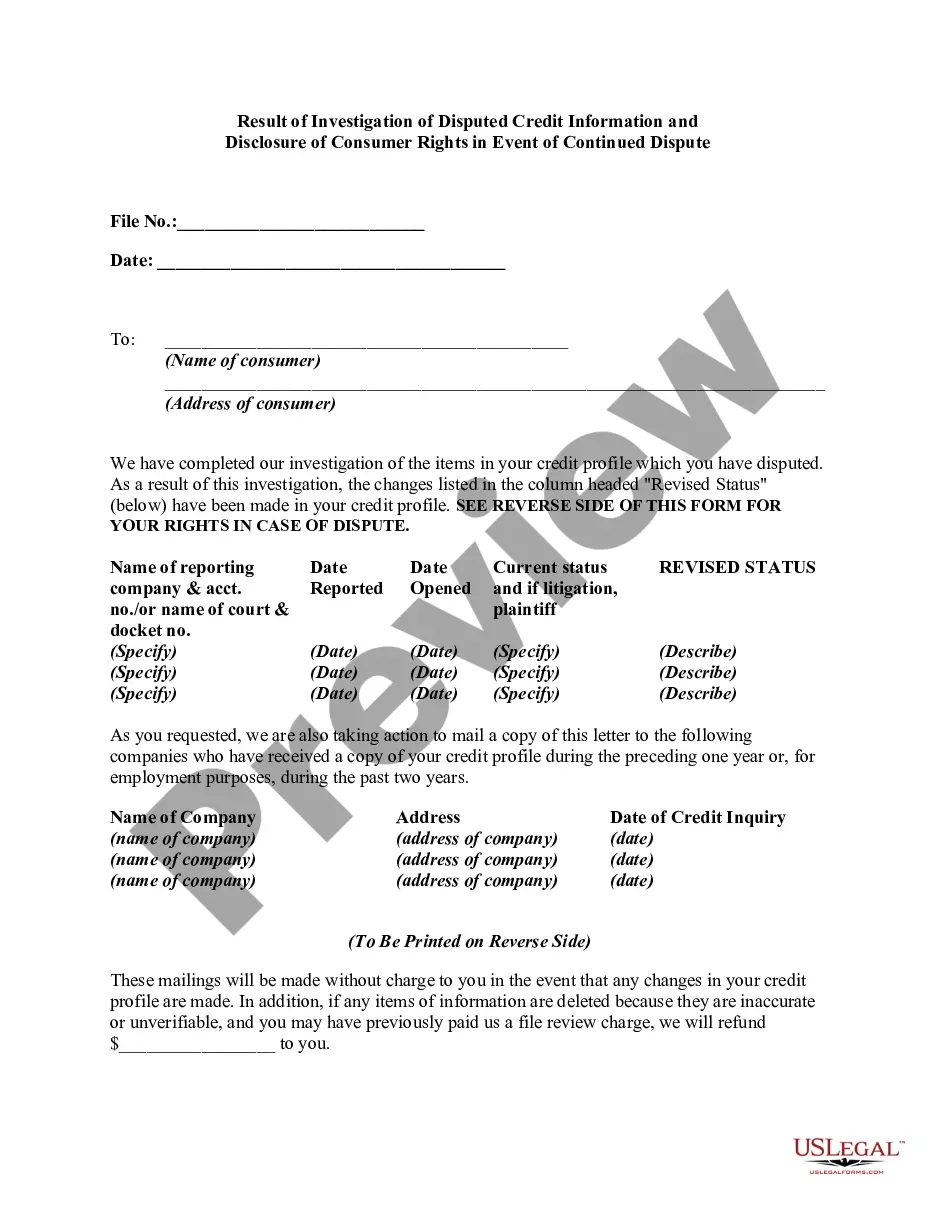

Under the Fair Credit Reporting Act, if a consumer disputes the completeness or accuracy of any item of information in the consumer's file, and the dispute is directly conveyed to the consumer reporting agency by the consumer, the reporting agency must, free of charge, conduct a reasonable reinvestigation to determine whether the disputed information is inaccurate, unless it has reasonable grounds to believe that the dispute is frivolous or irrelevant. If the information is erroneous, inaccurate, or can no longer be verified, the credit reporting agency must promptly correct or delete it and refrain from reporting the information in subsequent consumer reports.

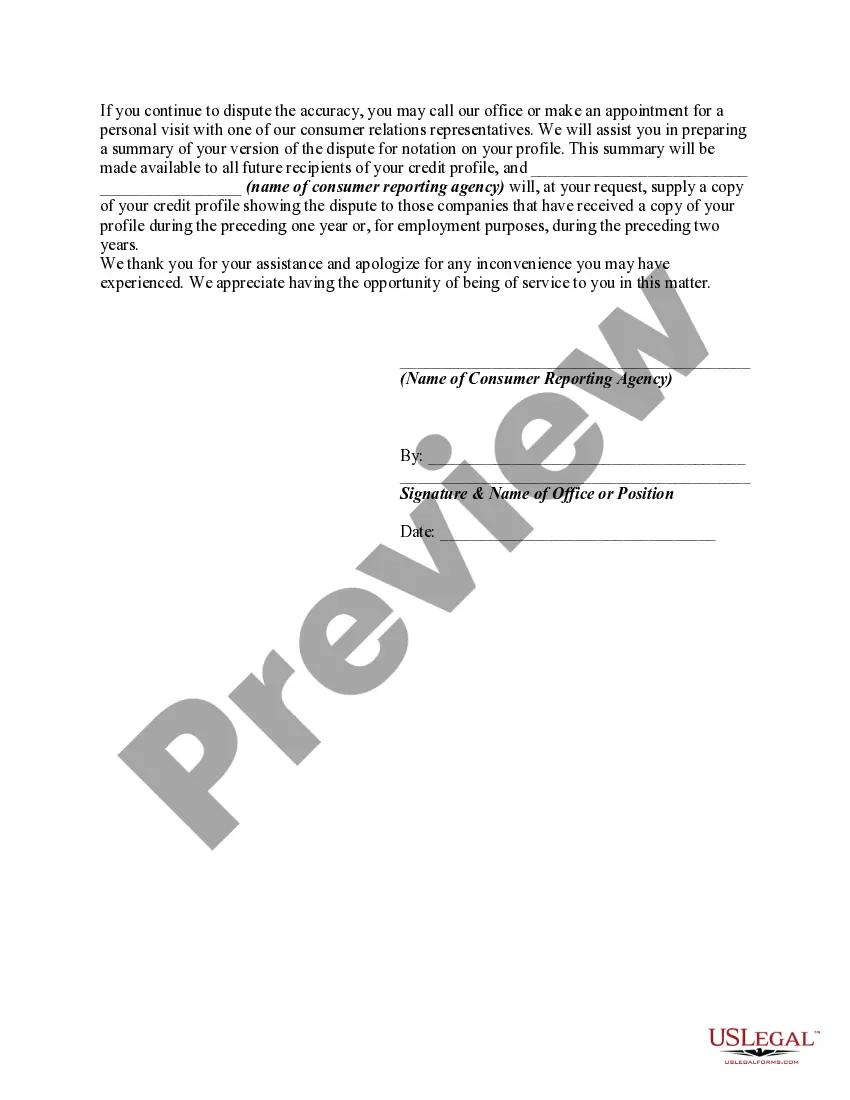

Following any deletion of information or notation as to disputed information, the agency, on request of the consumer, must furnish to certain persons either: (1) notification of the deletion; or (2) the consumer's statement of the dispute or the agency's summary of the statement. The consumer reporting agency must clearly and conspicuously disclose the consumer's rights to make such a request, such disclosure to be made at or prior to the time the information is deleted or the consumer's statement regarding the disputed information is received.

Title: Delaware Result of Investigation of Disputed Credit Information and Disclosure of Consumer Rights in Event of Continued Dispute: A Comprehensive Overview Introduction: Delaware's policies and procedures surrounding the investigation of disputed credit information and the disclosure of consumer rights in the event of a continued dispute play a fundamental role in protecting consumers' financial well-being. This article aims to provide a detailed description of Delaware's approach to resolving credit disputes, the results of investigations, and the rights consumers have in case the dispute persists. Keywords: Delaware, credit information, dispute investigation, consumer rights, continued dispute, results, disclosure I. Delaware's Credit Information Dispute Investigation Process: Delaware has established a structured process for examining disputed credit information. When a consumer submits a dispute, the following steps are typically followed: 1. Filing the Dispute: Consumers can initiate the process by filing a formal dispute with the Delaware credit reporting agencies or directly with the creditor holding the disputed information. 2. Investigation Initiation: The credit reporting agencies or creditors receiving the dispute will initiate an investigation promptly to verify the accuracy of the disputed credit information. 3. Verification and Communication: The agencies or creditors will contact relevant data providers, such as lenders or collection agencies, to cross-check the accuracy of the disputed information. They will communicate the results of their investigation in a timely manner. II. Results of Investigation: Based on the thorough investigation conducted by the credit reporting agencies or creditors, there are several potential outcomes: 1. Verified Accuracy: If the investigated information is deemed accurate, the disputed item will remain on the consumer's credit report. The consumer will be notified accordingly, along with the details of the investigation and the reasons for their decision. 2. Inaccurate Information: If the disputed item is found to be inaccurate, it will be removed or corrected from the consumer's credit report. Credit reporting agencies and creditors are responsible for informing the consumer and updating their credit records accordingly. 3. Incomplete or Unverifiable Information: In some cases, the investigation may lead to insufficient or unverifiable information. In such instances, the disputed item may be removed from the consumer's credit report due to the inability to validate its accuracy. III. Consumer Rights in Event of Continued Dispute: Delaware recognizes the significance of consumer rights during ongoing credit disputes. Should the consumer continue to disagree with the results of the investigation, the following rights may apply: 1. Reinvestigation Request: Consumers have the right to request a reinvestigation of the disputed credit information within certain time limits, typically within 30 days. This initiates a new examination of the disputed item. 2. Detailed Explanation: If the consumer continues to disagree after the reinvestigation, they have the right to receive a detailed explanation of the investigation's findings and the reasoning behind the decision. 3. File a Consumer Statement: If the consumer believes the disputed credit item should still not appear on their credit report, they can request to include a personal statement (up to 100 words) that will be visible to potential lenders or creditors. Conclusion: Delaware's commitment to resolving credit disputes thoroughly and protecting consumer rights ensures a fair and equitable process. By understanding the investigation results and the avenues available for continued dispute, consumers in Delaware can take control of their financial reputation and ensure the accuracy of their credit information.Title: Delaware Result of Investigation of Disputed Credit Information and Disclosure of Consumer Rights in Event of Continued Dispute: A Comprehensive Overview Introduction: Delaware's policies and procedures surrounding the investigation of disputed credit information and the disclosure of consumer rights in the event of a continued dispute play a fundamental role in protecting consumers' financial well-being. This article aims to provide a detailed description of Delaware's approach to resolving credit disputes, the results of investigations, and the rights consumers have in case the dispute persists. Keywords: Delaware, credit information, dispute investigation, consumer rights, continued dispute, results, disclosure I. Delaware's Credit Information Dispute Investigation Process: Delaware has established a structured process for examining disputed credit information. When a consumer submits a dispute, the following steps are typically followed: 1. Filing the Dispute: Consumers can initiate the process by filing a formal dispute with the Delaware credit reporting agencies or directly with the creditor holding the disputed information. 2. Investigation Initiation: The credit reporting agencies or creditors receiving the dispute will initiate an investigation promptly to verify the accuracy of the disputed credit information. 3. Verification and Communication: The agencies or creditors will contact relevant data providers, such as lenders or collection agencies, to cross-check the accuracy of the disputed information. They will communicate the results of their investigation in a timely manner. II. Results of Investigation: Based on the thorough investigation conducted by the credit reporting agencies or creditors, there are several potential outcomes: 1. Verified Accuracy: If the investigated information is deemed accurate, the disputed item will remain on the consumer's credit report. The consumer will be notified accordingly, along with the details of the investigation and the reasons for their decision. 2. Inaccurate Information: If the disputed item is found to be inaccurate, it will be removed or corrected from the consumer's credit report. Credit reporting agencies and creditors are responsible for informing the consumer and updating their credit records accordingly. 3. Incomplete or Unverifiable Information: In some cases, the investigation may lead to insufficient or unverifiable information. In such instances, the disputed item may be removed from the consumer's credit report due to the inability to validate its accuracy. III. Consumer Rights in Event of Continued Dispute: Delaware recognizes the significance of consumer rights during ongoing credit disputes. Should the consumer continue to disagree with the results of the investigation, the following rights may apply: 1. Reinvestigation Request: Consumers have the right to request a reinvestigation of the disputed credit information within certain time limits, typically within 30 days. This initiates a new examination of the disputed item. 2. Detailed Explanation: If the consumer continues to disagree after the reinvestigation, they have the right to receive a detailed explanation of the investigation's findings and the reasoning behind the decision. 3. File a Consumer Statement: If the consumer believes the disputed credit item should still not appear on their credit report, they can request to include a personal statement (up to 100 words) that will be visible to potential lenders or creditors. Conclusion: Delaware's commitment to resolving credit disputes thoroughly and protecting consumer rights ensures a fair and equitable process. By understanding the investigation results and the avenues available for continued dispute, consumers in Delaware can take control of their financial reputation and ensure the accuracy of their credit information.