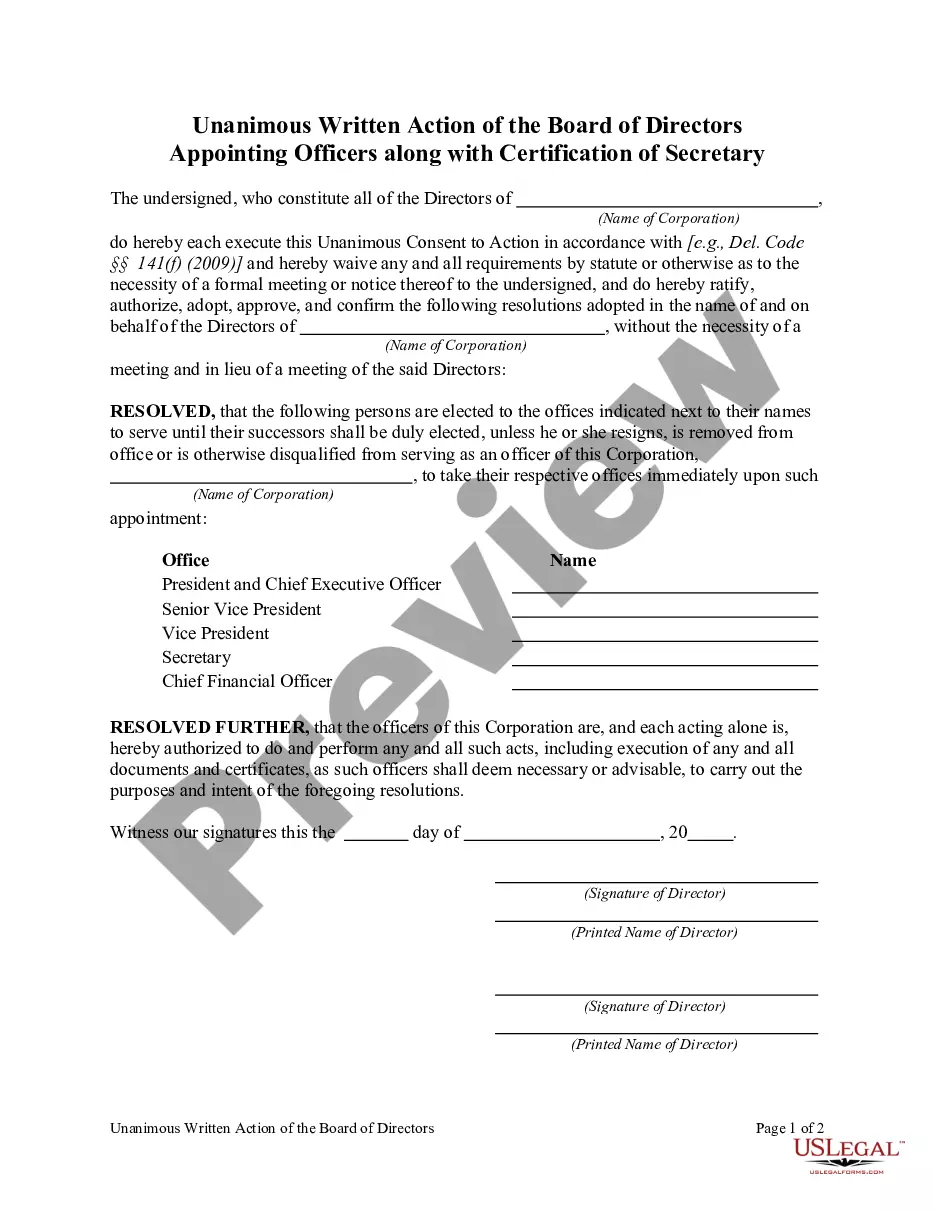

The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. TILA applies only to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use. This form was designed to cover an situation where the Seller is not a creditor as defined by the TILA.

Delaware Installment Sale Not Covered by Federal Consumer Credit Protection Act with Security Agreement: In Delaware, there are certain types of installment sales that are not covered by the Federal Consumer Credit Protection Act (FC CPA) when a security agreement is involved. These transactions may have specific considerations and regulations that potential buyers and sellers need to be aware of. Let's explore this further: 1. Delaware Real Estate Installment Sales: When purchasing real estate through an installment sale in Delaware, if the buyer defaults on their payments, the seller can acquire the property back without going through the foreclosure process. This type of transaction is not subject to the FC CPA but still requires a detailed security agreement outlining the terms and conditions of the sale. 2. Business Equipment or Machinery Installment Sales: Installment sales involving the purchase of business equipment or machinery in Delaware may not fall under the FC CPA if a security agreement is in place. It is important for both parties involved to establish clear terms and obligations within the security agreement, including any collateral. 3. Vehicle Installment Sales: While the FC CPA typically covers vehicle purchases, there are cases in Delaware where installment sales of vehicles with a security agreement are exempt. However, the Delaware Lemon Law may still provide certain protections to buyers if the vehicle turns out to be defective. 4. Personal Property Installment Sales: Delaware installment sales involving personal property, such as electronics or household appliances, may not be governed by the FC CPA if a security agreement is in effect. Buyers should exercise caution and thoroughly read the terms of the security agreement to understand their rights and obligations. In all of these Delaware installment sales not covered by the FC CPA with a security agreement, it is crucial for buyers and sellers to seek legal advice and ensure the terms are fair and transparent. The security agreement should outline the details of the transaction, including payment schedules, interest rates, collateral, default consequences, and the rights of both parties. It is important to note that even though these types of installment sales may not be covered by the FC CPA, other state laws and regulations may still offer certain protections to consumers. Therefore, it is always recommended to conduct thorough research and consult with legal professionals for specific guidance within Delaware when engaging in these types of transactions.