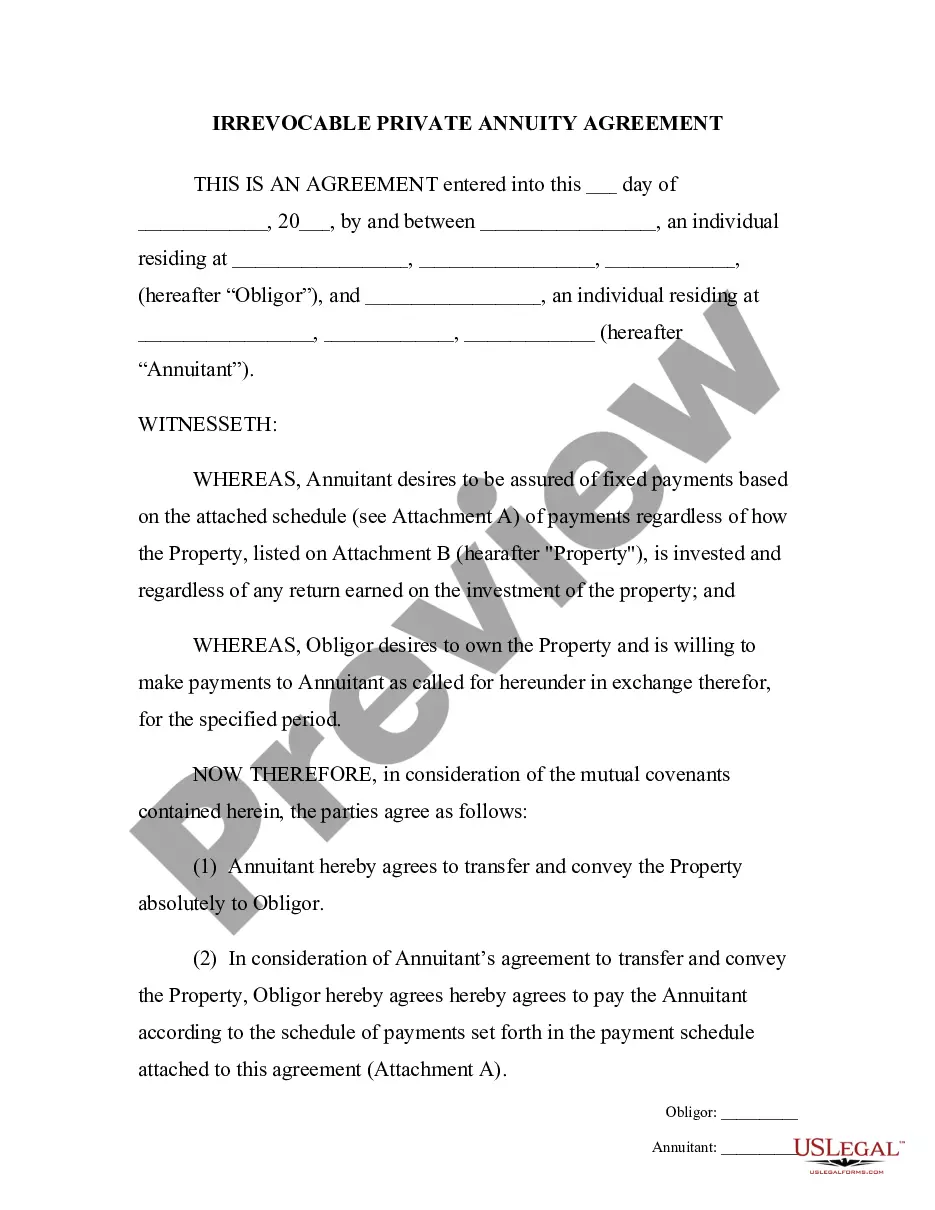

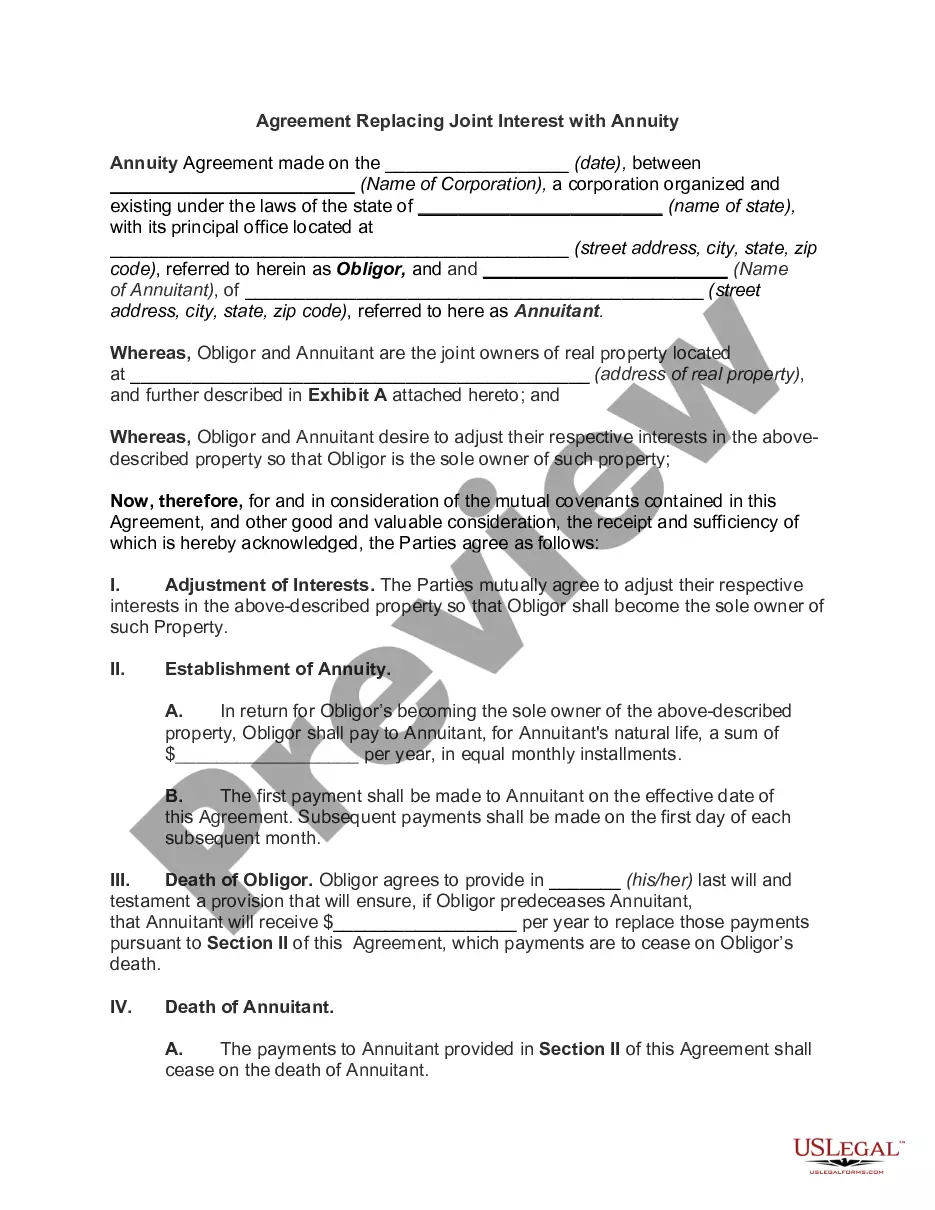

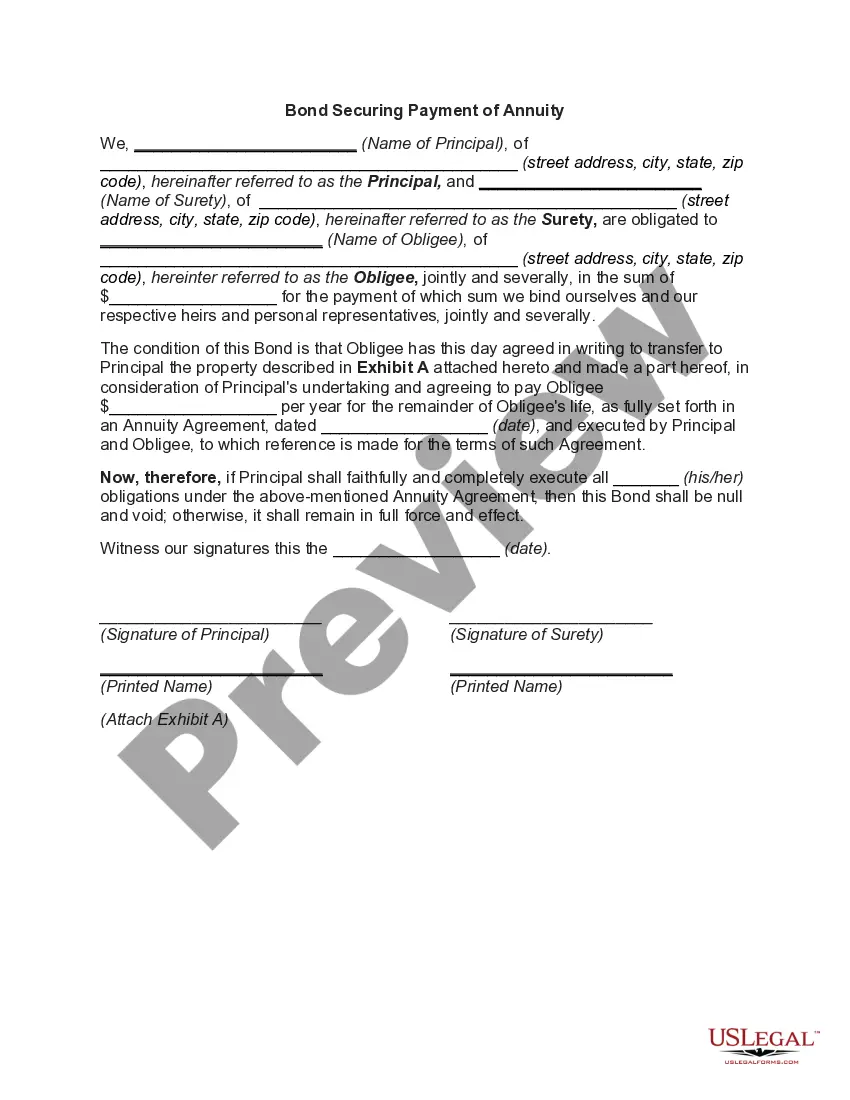

Delaware Private Annuity Agreement with Payments to Last for Life of Annuitant

Description

How to fill out Private Annuity Agreement With Payments To Last For Life Of Annuitant?

If you wish to finalize, obtain, or print authorized document templates, utilize US Legal Forms, the finest collection of legal forms accessible online.

Employ the site’s straightforward and user-friendly search function to find the documents you require.

Various templates for business and personal use are categorized by type and topic, or keywords.

Step 4. Once you have located the form you need, click the Get now button. Select the pricing plan you prefer and provide your details to register for an account.

Step 5. Complete the transaction. You can use your credit card or PayPal account to finalize the purchase.

- Utilize US Legal Forms to acquire the Delaware Private Annuity Agreement with Payments to Last for Life of Annuitant in just a few clicks.

- If you are already a US Legal Forms user, Log In to your account and click the Obtain button to acquire the Delaware Private Annuity Agreement with Payments to Last for Life of Annuitant.

- You can also access forms you previously downloaded under the My documents section of your account.

- If you are using US Legal Forms for the first time, follow the instructions below.

- Step 1. Ensure you have chosen the form for your appropriate city/state.

- Step 2. Utilize the Review feature to evaluate the form’s details. Don’t forget to read the description.

- Step 3. If you are dissatisfied with the form, use the Search section at the top of the screen to find alternative forms in the legal form format.

Form popularity

FAQ

The option that provides for lifetime payments while guaranteeing a minimum term is known as a 'guaranteed minimum payout annuity'. This annuity guarantees that you will receive payments for a specified duration, even if you pass away before that period concludes. This feature combines the benefits of lifelong income with the security of ensuring that your beneficiaries receive some financial support through a Delaware Private Annuity Agreement with Payments to Last for Life of Annuitant.

The life only annuity payout option is a financial arrangement where payments are made only to the annuitant for their lifetime. With this option, you receive the maximum monthly payments since no benefits extend to beneficiaries after your passing. This choice can be particularly appealing for those who prioritize maximizing their income during their retirement years through a Delaware Private Annuity Agreement with Payments to Last for Life of Annuitant.

A lifetime payout annuity, especially in the context of a Delaware Private Annuity Agreement with Payments to Last for Life of Annuitant, offers steady income for the rest of the annuitant's life. This type of annuity ensures that you can enjoy consistent financial support, regardless of how long you live. It is an effective strategy for retirement planning, allowing you to focus on enjoying life rather than worrying about your financial situation.

The Delaware Private Annuity Agreement with Payments to Last for Life of Annuitant typically includes an option known as the 'life and period certain annuity.' This option guarantees that the annuitant receives payments for their entire life while also ensuring payments continue for a specified term to the beneficiary. This structure provides flexibility and security, allowing you to plan effectively for both your financial needs and those of your loved ones.

The most common option for lifetime payments to the annuitant is the life annuity, which is a key feature of the Delaware Private Annuity Agreement with Payments to Last for Life of Annuitant. This option guarantees regular payments for the entire lifetime of the annuitant, providing financial security and peace of mind. You may also explore other options that may offer additional flexibility, such as joint and survivor annuities. For complete guidance, visit uslegalforms to find tailored solutions that meet your needs.

With a Delaware Private Annuity Agreement with Payments to Last for Life of Annuitant, the payments continue until the death of the annuitant. However, once the annuitant passes away, the payments typically cease, as the agreement is structured to benefit only the annuitant. Different terms may apply if you have designated a beneficiary or if the agreement includes specific conditions. To ensure clarity and explore options, consider discussing your situation with a professional or accessing informative resources on the uslegalforms platform.

Delaware Life is often considered a reliable option for individuals seeking a stable retirement income. Their offerings, including the Delaware Private Annuity Agreement with Payments to Last for Life of Annuitant, cater to diverse financial goals. However, it is important to assess personal circumstances and objectives to determine if this is the right match for your needs.

Payments stop at the annuitant's death in a life-only settlement option. The Delaware Private Annuity Agreement with Payments to Last for Life of Annuitant often outlines this specific condition, which is essential for understanding payout structures. Evaluating this choice helps ensure that you secure the most beneficial plan for your retirement needs.

Upon the death of the annuitant, the tax implications of private annuities, including those covered by a Delaware Private Annuity Agreement with Payments to Last for Life of Annuitant, can vary. Generally, the remaining contract value may be included in the estate for tax purposes. Additionally, beneficiaries may face specific tax obligations regarding any inherited amounts, making it wise to consult a tax professional for personalized advice.

The life-only annuity is a common type that stops payment when the annuitant dies. This means that once the annuitant passes away, no further payments are made, aligning with the terms of the Delaware Private Annuity Agreement with Payments to Last for Life of Annuitant. It's vital to weigh this option against one's financial needs and goals for retirement.