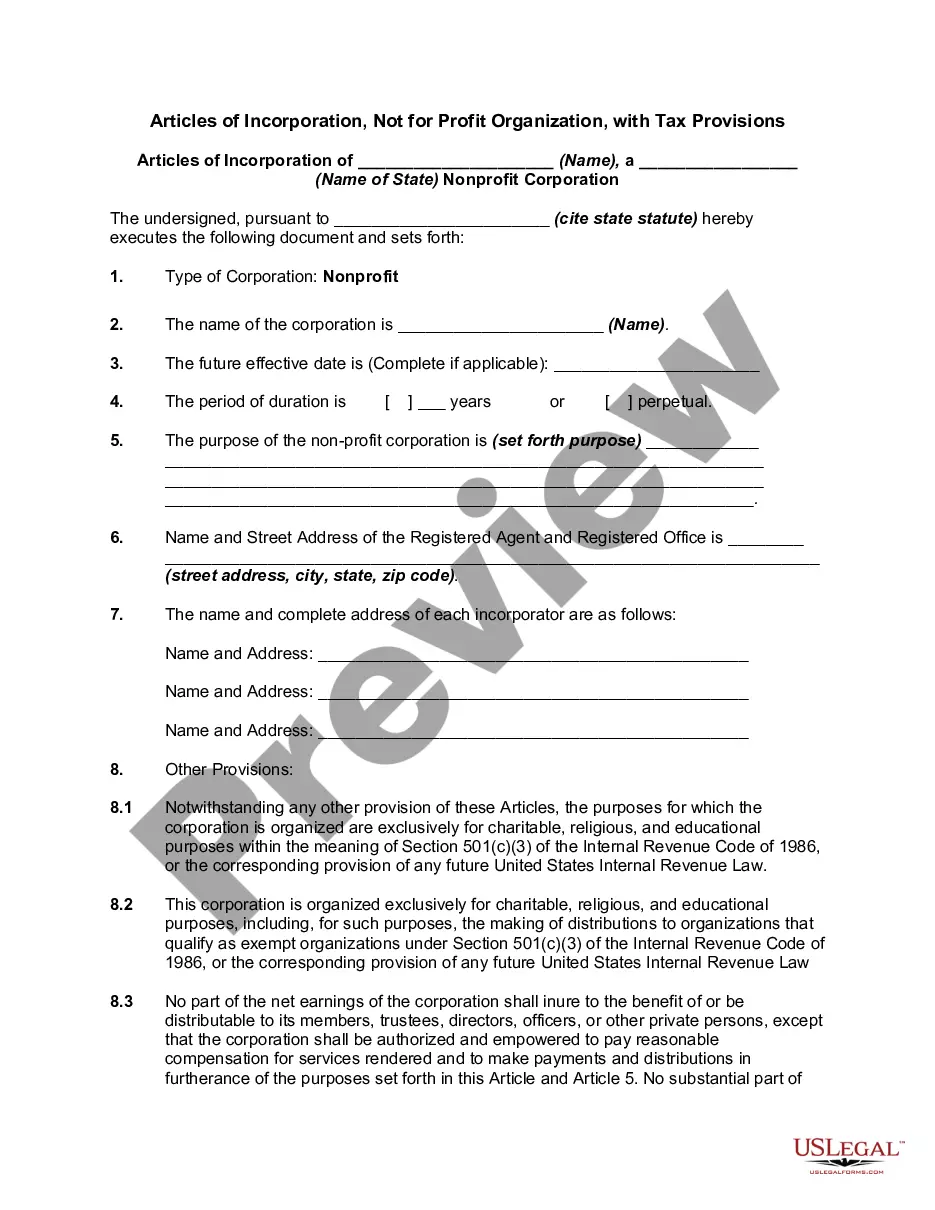

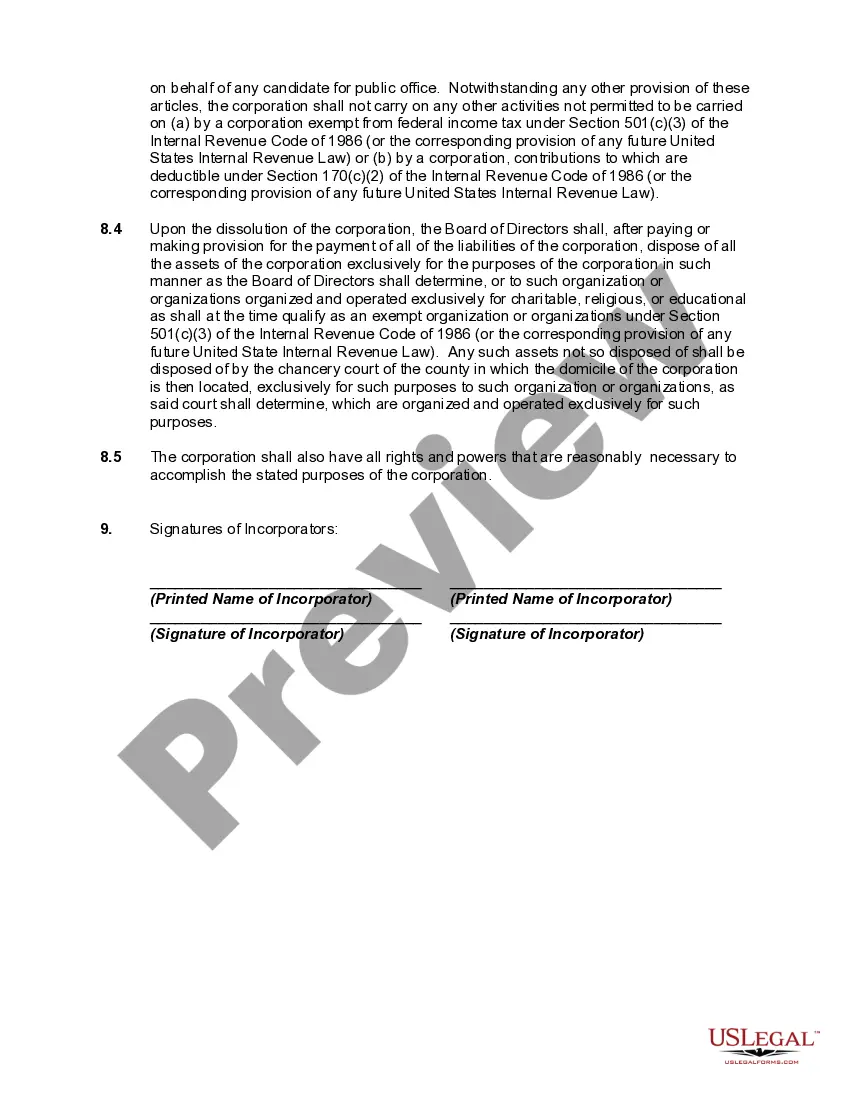

The proper form and necessary content of articles or certificates of incorporation for a nonprofit corporation depend largely on the requirements of the state nonprofit corporation act in the state of incorporation. Typically nonprofit corporations have no capital stock and therefore have members, not stockholders. Because federal tax-exempt status will be sought for most nonprofit corporations, the articles or certificate of incorporation must be carefully drafted to include specific language designed to ensure qualification for tax-exempt status.

Title: Delaware Articles of Incorporation for Not-for-Profit Organizations with Tax Provisions Introduction: Delaware Articles of Incorporation for Not-for-Profit Organizations with Tax Provisions are legal documents that establish and define the structure, purpose, and governance of a non-profit organization operating in the state of Delaware. These articles are specifically designed to ensure compliance with tax laws and regulations. This article will provide a detailed description of what Delaware Articles of Incorporation for Not-for-Profit Organizations with Tax Provisions entail, including relevant keywords essential for understanding this process. 1. Overview of Delaware Articles of Incorporation: The Delaware Articles of Incorporation serve as the foundational document for a not-for-profit organization, formally creating it as a legal entity within the state. These articles encompass important information such as the organization's name, purpose, registered agent details, members or directors, and other critical provisions. The articles must also include specific tax provisions to ensure compliance with federal and state tax guidelines. 2. Tax Provisions in Delaware Articles of Incorporation: a) 501(c)(3) Status: Not-for-profit organizations frequently seek tax-exempt status under section 501(c)(3) of the Internal Revenue Code. Delaware articles of incorporation must include necessary language stating the purpose and activities of the organization align with the requirements for obtaining and maintaining tax-exempt status. b) Non-Distribution Clause: To qualify for tax-exempt status, not-for-profit organizations must include a non-distribution clause within their articles of incorporation. This provision restricts the organization from distributing profits or assets to its members, directors, officers, or any other private individuals. c) Dissolution Clause: The articles of incorporation must outline the procedures for the organization's dissolution, including the distribution of assets in accordance with applicable tax regulations. d) Unrelated Business Income: If the organization engages in activities generating unrelated business income, specific provisions must be included in the articles of incorporation to ensure compliance with tax laws regarding reporting and payment of taxes on such income. 3. Variations of Delaware Articles of Incorporation for Not-for-Profit Organizations with Tax Provisions: a) Basic Articles of Incorporation: These are standard documents meeting the minimum requirements of Delaware law for incorporating a not-for-profit organization. They provide the essential information regarding the organization's name, purpose, registered agent, and basic tax provisions necessary to establish tax-exempt status. b) Advanced Articles of Incorporation: Some organizations may require additional provisions in their articles to comply with specific state or federal regulations or meet the requirements of grant-making organizations or potential donors. These provisions may include restrictions on activities, grant-making authorities, or certain governance structures. c) Amended Articles of Incorporation: Organizations may need to update or modify their articles of incorporation to reflect changes in their purpose, governance, or tax provisions. Amended articles of incorporation are filed to officially document these alterations. Conclusion: Delaware Articles of Incorporation for Not-for-Profit Organizations with Tax Provisions are critical legal documents that establish the foundation of a non-profit organization while ensuring compliance with tax laws. Including relevant keywords like "Delaware," "Articles of Incorporation," "Not-for-Profit Organization," and "Tax Provisions" enhances the understanding of this topic. Understanding the various types, such as basic, advanced, and amended articles, helps organizations tailor their incorporation documents to their specific needs and requirements.

Title: Delaware Articles of Incorporation for Not-for-Profit Organizations with Tax Provisions Introduction: Delaware Articles of Incorporation for Not-for-Profit Organizations with Tax Provisions are legal documents that establish and define the structure, purpose, and governance of a non-profit organization operating in the state of Delaware. These articles are specifically designed to ensure compliance with tax laws and regulations. This article will provide a detailed description of what Delaware Articles of Incorporation for Not-for-Profit Organizations with Tax Provisions entail, including relevant keywords essential for understanding this process. 1. Overview of Delaware Articles of Incorporation: The Delaware Articles of Incorporation serve as the foundational document for a not-for-profit organization, formally creating it as a legal entity within the state. These articles encompass important information such as the organization's name, purpose, registered agent details, members or directors, and other critical provisions. The articles must also include specific tax provisions to ensure compliance with federal and state tax guidelines. 2. Tax Provisions in Delaware Articles of Incorporation: a) 501(c)(3) Status: Not-for-profit organizations frequently seek tax-exempt status under section 501(c)(3) of the Internal Revenue Code. Delaware articles of incorporation must include necessary language stating the purpose and activities of the organization align with the requirements for obtaining and maintaining tax-exempt status. b) Non-Distribution Clause: To qualify for tax-exempt status, not-for-profit organizations must include a non-distribution clause within their articles of incorporation. This provision restricts the organization from distributing profits or assets to its members, directors, officers, or any other private individuals. c) Dissolution Clause: The articles of incorporation must outline the procedures for the organization's dissolution, including the distribution of assets in accordance with applicable tax regulations. d) Unrelated Business Income: If the organization engages in activities generating unrelated business income, specific provisions must be included in the articles of incorporation to ensure compliance with tax laws regarding reporting and payment of taxes on such income. 3. Variations of Delaware Articles of Incorporation for Not-for-Profit Organizations with Tax Provisions: a) Basic Articles of Incorporation: These are standard documents meeting the minimum requirements of Delaware law for incorporating a not-for-profit organization. They provide the essential information regarding the organization's name, purpose, registered agent, and basic tax provisions necessary to establish tax-exempt status. b) Advanced Articles of Incorporation: Some organizations may require additional provisions in their articles to comply with specific state or federal regulations or meet the requirements of grant-making organizations or potential donors. These provisions may include restrictions on activities, grant-making authorities, or certain governance structures. c) Amended Articles of Incorporation: Organizations may need to update or modify their articles of incorporation to reflect changes in their purpose, governance, or tax provisions. Amended articles of incorporation are filed to officially document these alterations. Conclusion: Delaware Articles of Incorporation for Not-for-Profit Organizations with Tax Provisions are critical legal documents that establish the foundation of a non-profit organization while ensuring compliance with tax laws. Including relevant keywords like "Delaware," "Articles of Incorporation," "Not-for-Profit Organization," and "Tax Provisions" enhances the understanding of this topic. Understanding the various types, such as basic, advanced, and amended articles, helps organizations tailor their incorporation documents to their specific needs and requirements.