Delaware Review of Loan Application

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Review Of Loan Application?

US Legal Forms - one of several biggest libraries of lawful kinds in the United States - offers an array of lawful papers web templates you can down load or print out. While using site, you can get 1000s of kinds for enterprise and specific functions, sorted by categories, says, or key phrases.You will find the most up-to-date variations of kinds like the Delaware Review of Loan Application in seconds.

If you currently have a registration, log in and down load Delaware Review of Loan Application through the US Legal Forms collection. The Acquire option can look on each type you see. You have access to all earlier saved kinds inside the My Forms tab of your profile.

If you wish to use US Legal Forms the very first time, here are easy instructions to obtain started out:

- Make sure you have selected the proper type for the metropolis/region. Go through the Review option to review the form`s articles. Look at the type outline to ensure that you have chosen the appropriate type.

- In case the type doesn`t satisfy your demands, make use of the Look for area on top of the display screen to obtain the one who does.

- Should you be satisfied with the shape, affirm your decision by simply clicking the Buy now option. Then, pick the rates prepare you prefer and provide your qualifications to sign up to have an profile.

- Procedure the transaction. Utilize your credit card or PayPal profile to perform the transaction.

- Find the formatting and down load the shape on the device.

- Make adjustments. Fill up, edit and print out and sign the saved Delaware Review of Loan Application.

Each web template you added to your bank account lacks an expiry particular date and is the one you have for a long time. So, if you would like down load or print out one more duplicate, just proceed to the My Forms section and then click around the type you need.

Obtain access to the Delaware Review of Loan Application with US Legal Forms, by far the most extensive collection of lawful papers web templates. Use 1000s of specialist and state-distinct web templates that meet your company or specific requires and demands.

Form popularity

FAQ

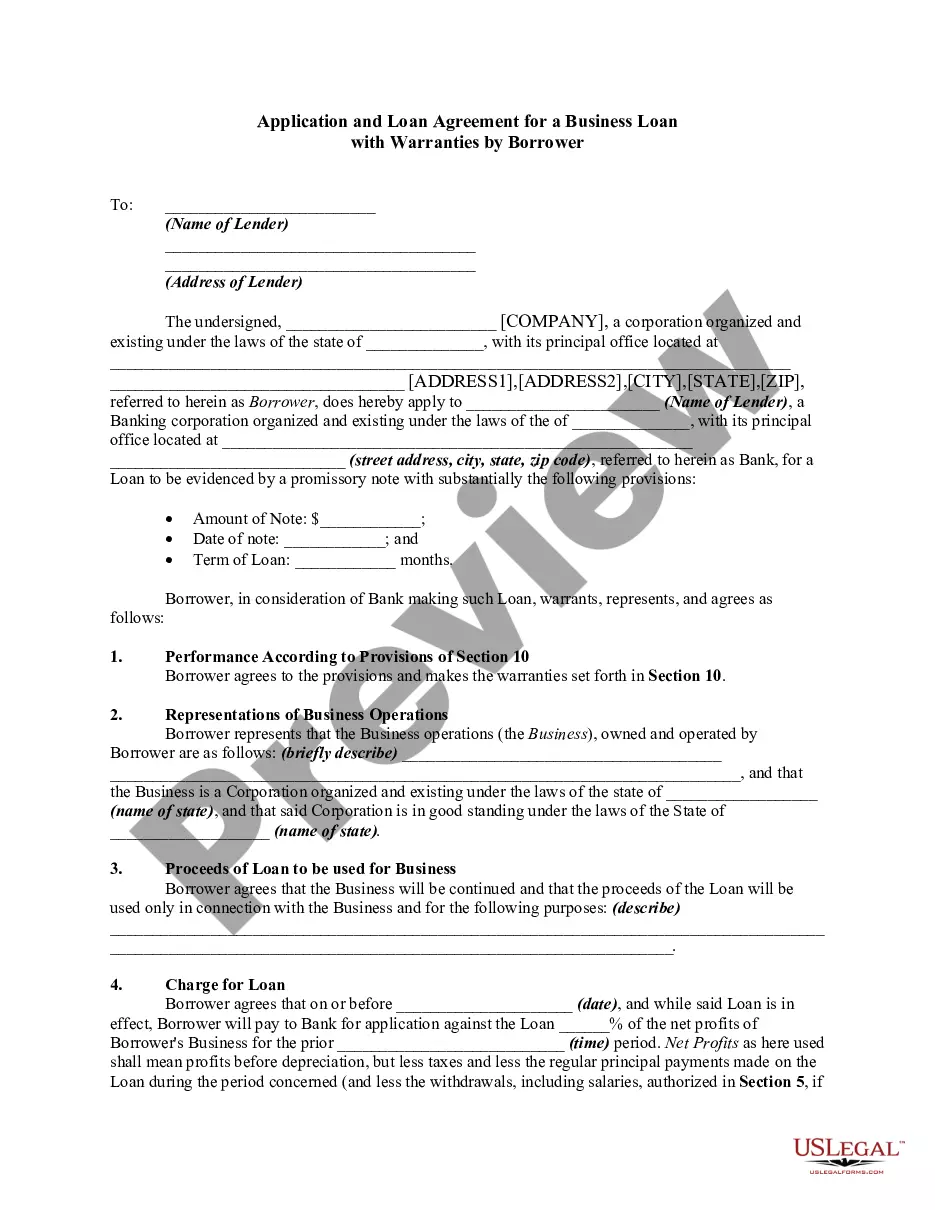

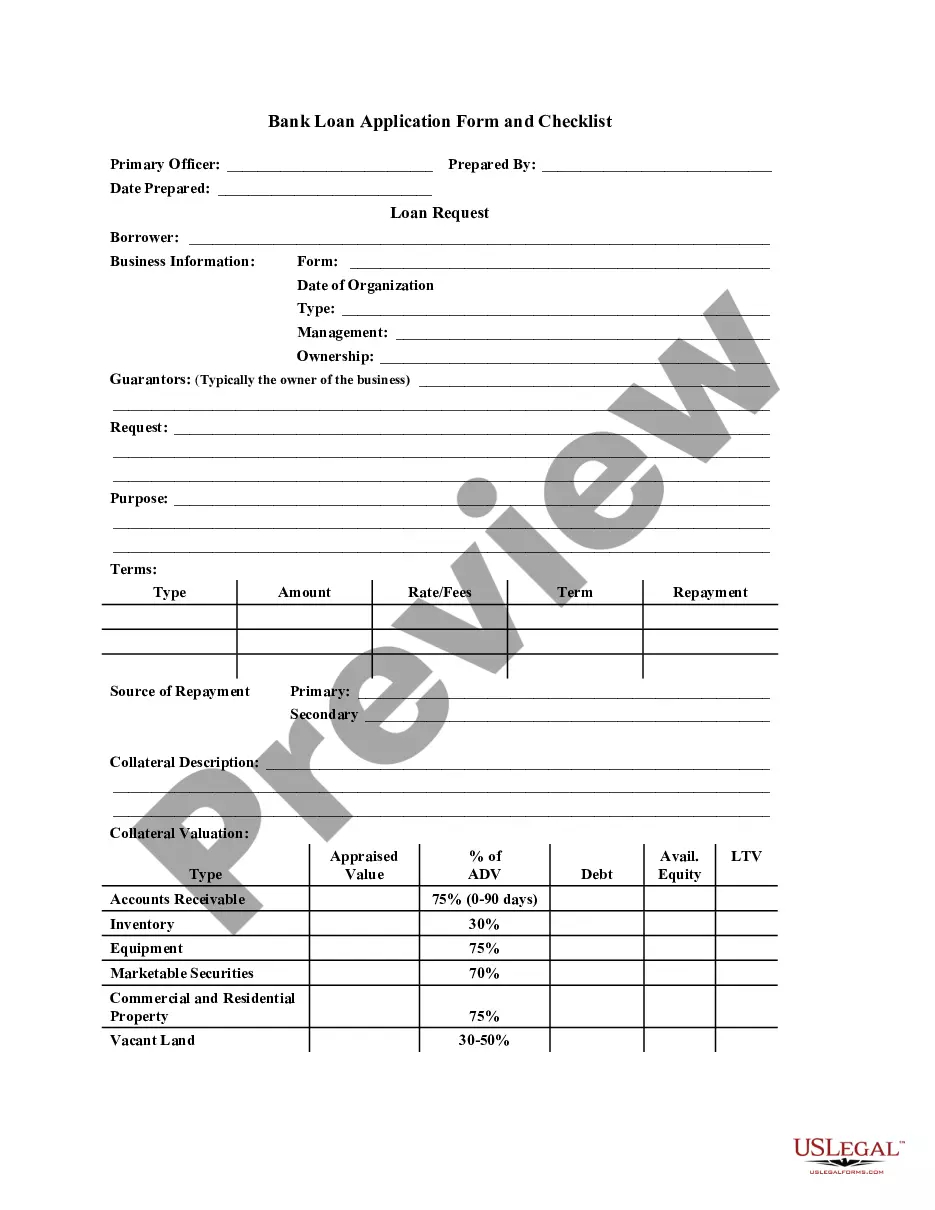

When reviewing a bank loan, there are several factors you need to consider to ensure that the loan is suitable for you. Interest Rates - The interest rate is the amount of money the lender charges for borrowing the funds. ... Repayment Terms - The repayment term is the length of time you have to repay the loan.

What Should I Look for When Reviewing Loan Documents? Principal loan Amount. ... Loan duration. ... Interest rate. ... Repayment terms : Every loan agreement should have a repayment schedule that provides the borrower with clear instructions on how to repay the loan. ... Fees and charges. ... Collateral. ... Default. ... Collection procedures.

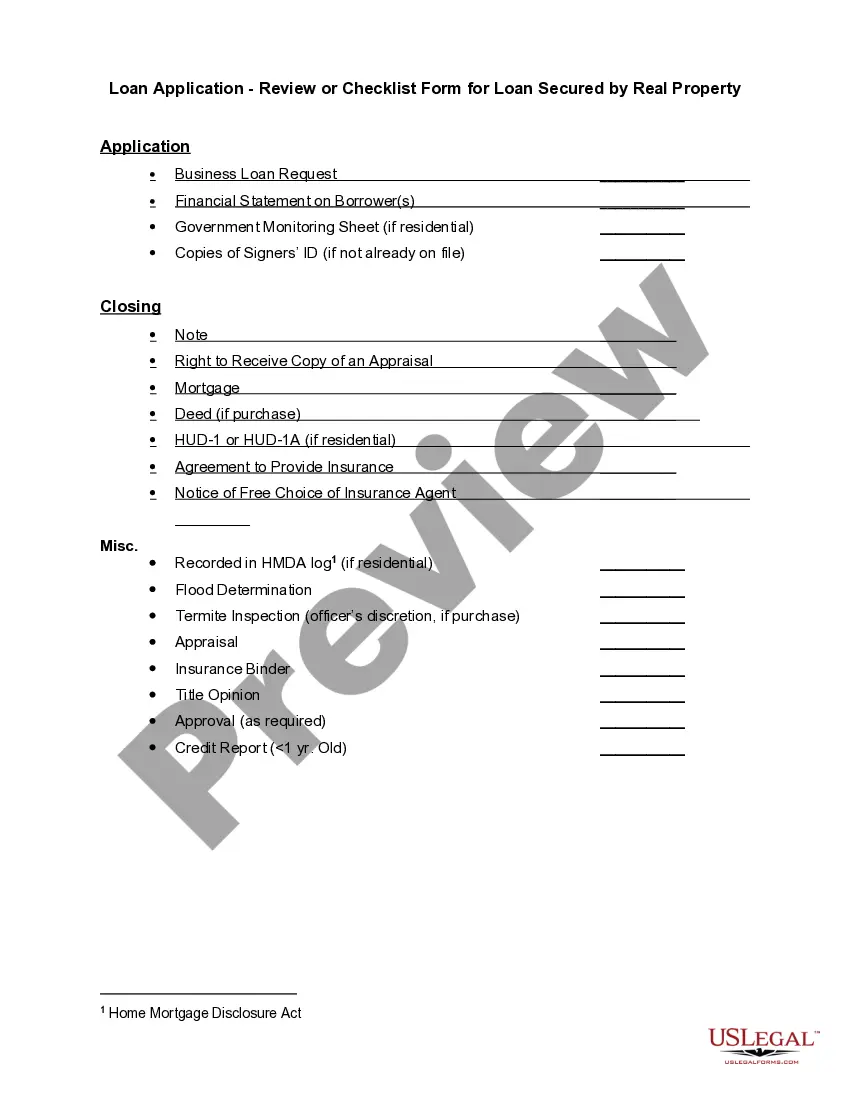

A loan review provides an assessment of the overall quality of a loan portfolio. Specifically, a loan review: ? Assesses individual loans, including repayment risks.

The loan review will consist of meetings with lending staff including loan administration to understand the lending process and procedures from intake to closing. The loan review team will also be reviewing underwriting and collateral files to ascertain the underwriting, monitoring, and documentation practices.

By understanding the different types of loans available, reviewing the loan terms and conditions, and working with a financial advisor, you can ensure that you're getting the best loan for your needs. Remember to review your credit report and prepare the necessary documents before applying for a loan.

5 Key Factors to Consider When Evaluating Your Loan Offer Loan amount. ... Loan Type. ... Interest rate and APR. ... Prepayment. ... Terms. ... Does the loan amount meet your needs? ... Can you afford the monthly payment? ... Is the interest rate reasonable, and how will you know?

A credit review?also known as account monitoring or account review inquiry?is a periodic assessment of an individual's or business's credit profile. Creditors?such as banks, financial services institutions, credit bureaus, settlement companies, and credit counselors?may conduct credit reviews.