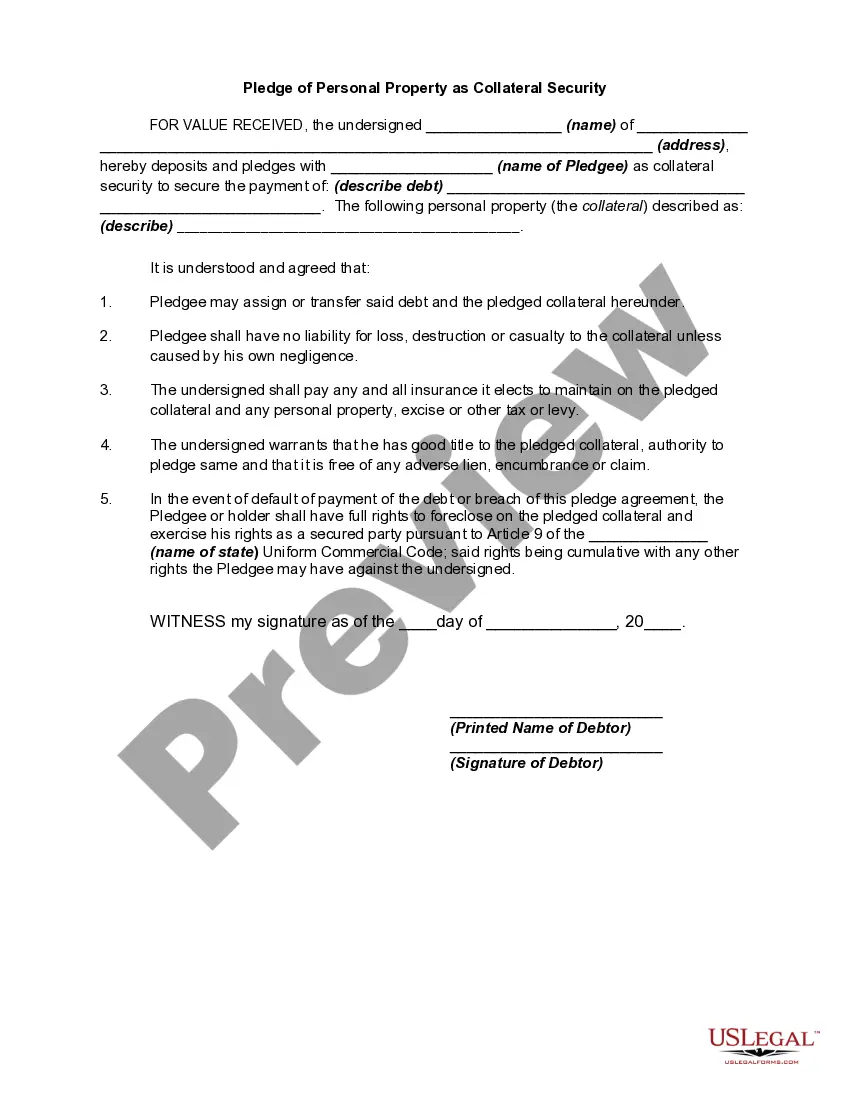

Title: Delaware Pledge of Personal Property as Collateral Security: A Comprehensive Explanation Introduction: Delaware Pledge of Personal Property as Collateral Security is a legal arrangement where a borrower pledges their personal property to secure a loan or debt. This agreement provides the lender with a security interest in the borrower's personal property, acting as collateral for the loan. It serves as a way to mitigate risks associated with lending and enable lenders to recover their funds in case of default by the borrower. This article will delve into the details of the Delaware Pledge of Personal Property as Collateral Security, exploring its types and significance. Keywords: Delaware Pledge, Personal Property, Collateral Security, Loan, Borrower, Lender, Security Interest, Default, Debt Types of Delaware Pledge of Personal Property as Collateral Security: 1. Floating Lien: This type of pledge agreement covers a broad range of personal property, including inventory, equipment, receivables, and other tangible assets of the borrower. A floating lien allows the borrower to continue using and disposing of the pledged property in the normal course of business unless default occurs. 2. Specific Lien: In contrast to a floating lien, a specific lien pertains to a particular asset or group of assets specified in the agreement. It restricts the borrower from disposing of or transferring the pledged property without the lender's consent until the debt is repaid. 3. Intellectual Property Lien: This type of pledge primarily involves intangible assets such as patents, trademarks, copyrights, and trade secrets. Lenders may require intellectual property as collateral for loans, particularly in technology-based industries. 4. Securities Pledge: Securities, including stocks, bonds, and other investment instruments, can be pledged as collateral. The borrower transfers physical possession or control over the securities to the lender, who holds them until the debt is settled. 5. Accounts Receivable Pledge: Borrowers can pledge their accounts receivable (unpaid customer invoices) as collateral. Lenders secure their interests in the borrower's future receivables, giving them recourse if the borrower fails to repay the loan. Significance and Benefits: 1. Risk Mitigation: Delaware Pledge of Personal Property as Collateral Security mitigates risks for lenders by providing a tangible asset, ensuring repayment even in default scenarios. 2. Enhanced Borrowing Capacity: Borrowers can leverage their personal property to secure larger loans or better loan terms due to the reduced risk for lenders. 3. Flexibility: Depending on the type of pledge agreement, borrowers may be able to continue using and disposing of their personal property, allowing them to conduct business as usual. 4. Access to Capital: Delaware Pledge enables borrowers to unlock the value of their personal property, providing them with access to much-needed funds for business expansion, investment, or debt consolidation. 5. Lower Interest Rates: By offering collateral, borrowers demonstrate their commitment to repayment, which may result in lower interest rates compared to unsecured loans. Conclusion: Delaware Pledge of Personal Property as Collateral Security is a valuable tool for both lenders and borrowers. It provides lenders with security and assurance of loan repayment, while borrowers can secure the funds they need to meet their financial objectives. By understanding the various types of pledges and their significance, borrowers can make informed decisions, maximize their borrowing capacity, and unlock new opportunities.

Delaware Pledge of Personal Property as Collateral Security

Description

How to fill out Delaware Pledge Of Personal Property As Collateral Security?

US Legal Forms - one of the most significant libraries of authorized forms in the States - offers a wide array of authorized document web templates you can down load or produce. While using site, you can get 1000s of forms for business and personal uses, categorized by categories, suggests, or search phrases.You can get the newest variations of forms much like the Delaware Pledge of Personal Property as Collateral Security in seconds.

If you currently have a registration, log in and down load Delaware Pledge of Personal Property as Collateral Security from the US Legal Forms collection. The Acquire option will appear on every type you see. You have access to all previously delivered electronically forms inside the My Forms tab of your respective bank account.

In order to use US Legal Forms for the first time, listed below are basic recommendations to get you started off:

- Be sure to have picked the right type for the metropolis/state. Click on the Review option to review the form`s articles. Look at the type outline to ensure that you have chosen the right type.

- If the type doesn`t satisfy your needs, use the Search field towards the top of the monitor to obtain the the one that does.

- Should you be satisfied with the form, verify your option by clicking the Get now option. Then, opt for the prices plan you favor and offer your credentials to sign up on an bank account.

- Process the transaction. Utilize your Visa or Mastercard or PayPal bank account to complete the transaction.

- Choose the structure and down load the form on your product.

- Make alterations. Fill out, edit and produce and signal the delivered electronically Delaware Pledge of Personal Property as Collateral Security.

Every design you added to your bank account does not have an expiry day and it is your own property eternally. So, if you wish to down load or produce another duplicate, just visit the My Forms portion and then click in the type you require.

Gain access to the Delaware Pledge of Personal Property as Collateral Security with US Legal Forms, one of the most comprehensive collection of authorized document web templates. Use 1000s of specialist and state-particular web templates that meet your organization or personal requirements and needs.