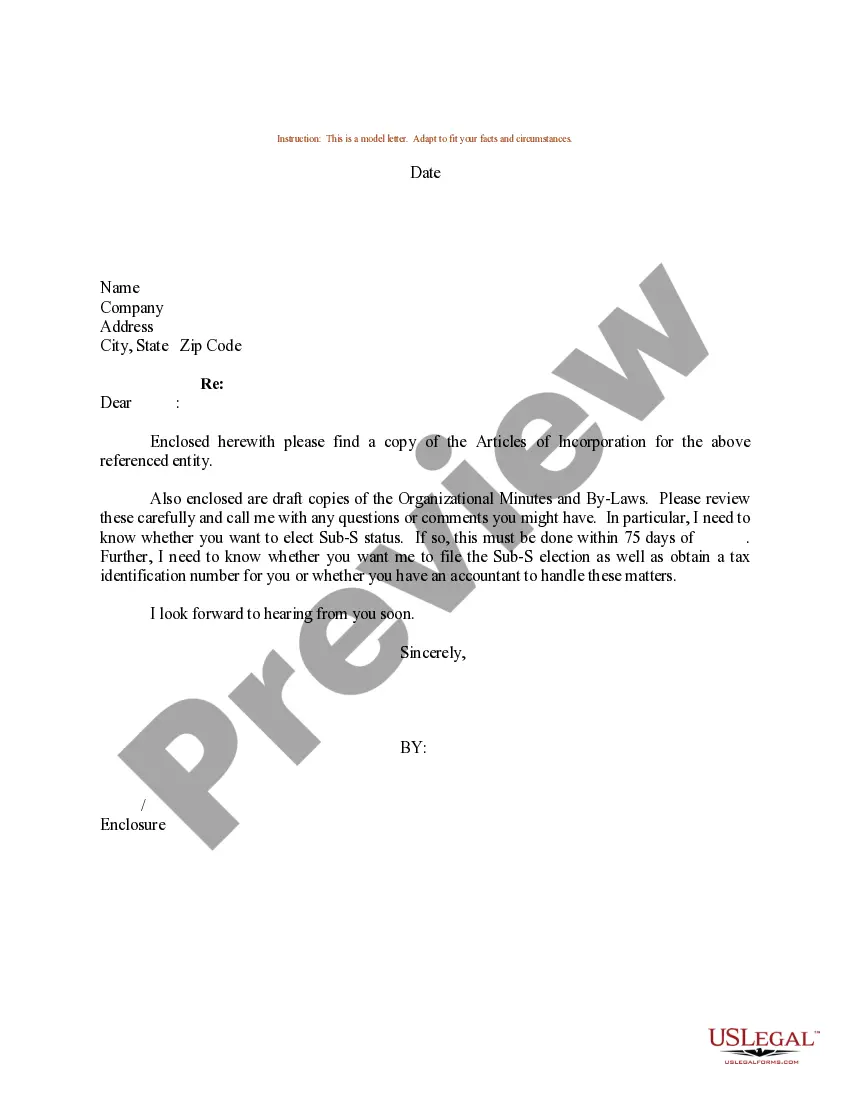

Title: Delaware Sample Letter regarding Articles of Incorporation — Election of Sub-S Status Introduction: In Delaware, a Sample Letter regarding Articles of Incorporation — Election of Sub-S Status is a formal document used by corporations to pursue Subchapter S (Sub-S) corporation tax status. This classification allows corporations to pass income, losses, deductions, and credits through to their shareholders' personal tax returns, thus avoiding double taxation on corporate profits. This article will provide a detailed description of the purpose, key sections, and different types of Sample Letters regarding Articles of Incorporation — Election of Sub-S Status in Delaware. 1. Purpose of the Delaware Sample Letter regarding Articles of Incorporation — Election of Sub-S Status: By electing Sub-S status, corporations aim to gain tax advantages, shield personal assets, and maximize flexibility in tax planning. The Sample Letter acts as a formal request to the Internal Revenue Service (IRS), informing them of the corporation's intent to be taxed as a Sub-S corporation. 2. Key Sections of the Delaware Sample Letter regarding Articles of Incorporation — Election of Sub-S Status: a. Corporation Details: Provide the corporation's legal name, date of incorporation, principal address, and taxpayer identification number (TIN). b. Election Statement: Clearly state the corporation's election to be taxed as a Sub-S corporation under Subchapter S of the Internal Revenue Code. c. Shareholder Consent: Attach a list of shareholders, their respective addresses, shares owned, and Tins. Include a statement expressing the consent of each shareholder to the Sub-S election. d. Effective Date: Specify the effective date of the Sub-S election and indicate whether it is for the current or future tax year. e. Signature and Date: The Sample Letter must be signed by an authorized officer of the corporation and include the date of signing. 3. Types of Delaware Sample Letters regarding Articles of Incorporation — Election of Sub-S Status: a. Initial Sub-S Election: This letter is used when a newly incorporated corporation wishes to elect Sub-S status from its inception. It is filed within 75 days of incorporation. b. Retroactive Sub-S Election: If a corporation missed the deadline for the initial Sub-S election, but still wants to elect Sub-S status, this letter is used. It includes a statement justifying the reason for the missed deadline. c. Late Sub-S Election: This letter is utilized when an existing corporation decides to convert its tax status to Sub-S after the initial 75-day period. It requires detailing the circumstances leading to the late election and requesting the IRS's approval. Conclusion: The Delaware Sample Letter regarding Articles of Incorporation — Election of Sub-S Status is a crucial document for corporations seeking the tax benefits associated with Sub-S status. By accurately completing the key sections and choosing the appropriate type of letter, corporations can properly request the IRS to recognize their election.

Delaware Sample Letter regarding Articles of Incorporation - Election of Sub-S Status

Description

How to fill out Delaware Sample Letter Regarding Articles Of Incorporation - Election Of Sub-S Status?

It is possible to invest hours on the Internet attempting to find the authorized papers web template that fits the state and federal needs you want. US Legal Forms supplies a huge number of authorized kinds which are evaluated by pros. You can actually obtain or produce the Delaware Sample Letter regarding Articles of Incorporation - Election of Sub-S Status from my support.

If you have a US Legal Forms bank account, you are able to log in and click the Obtain button. Following that, you are able to full, change, produce, or signal the Delaware Sample Letter regarding Articles of Incorporation - Election of Sub-S Status. Every authorized papers web template you purchase is your own property forever. To obtain an additional duplicate associated with a obtained form, proceed to the My Forms tab and click the related button.

Should you use the US Legal Forms internet site initially, adhere to the basic directions beneath:

- Initial, make sure that you have selected the correct papers web template for the region/town of your liking. Read the form outline to ensure you have picked out the correct form. If available, use the Preview button to appear through the papers web template at the same time.

- If you would like find an additional version from the form, use the Look for field to find the web template that fits your needs and needs.

- Once you have located the web template you need, simply click Purchase now to carry on.

- Find the rates program you need, key in your references, and sign up for an account on US Legal Forms.

- Complete the deal. You can use your Visa or Mastercard or PayPal bank account to pay for the authorized form.

- Find the format from the papers and obtain it to the device.

- Make modifications to the papers if possible. It is possible to full, change and signal and produce Delaware Sample Letter regarding Articles of Incorporation - Election of Sub-S Status.

Obtain and produce a huge number of papers web templates utilizing the US Legal Forms website, that provides the biggest selection of authorized kinds. Use professional and state-distinct web templates to tackle your small business or individual needs.