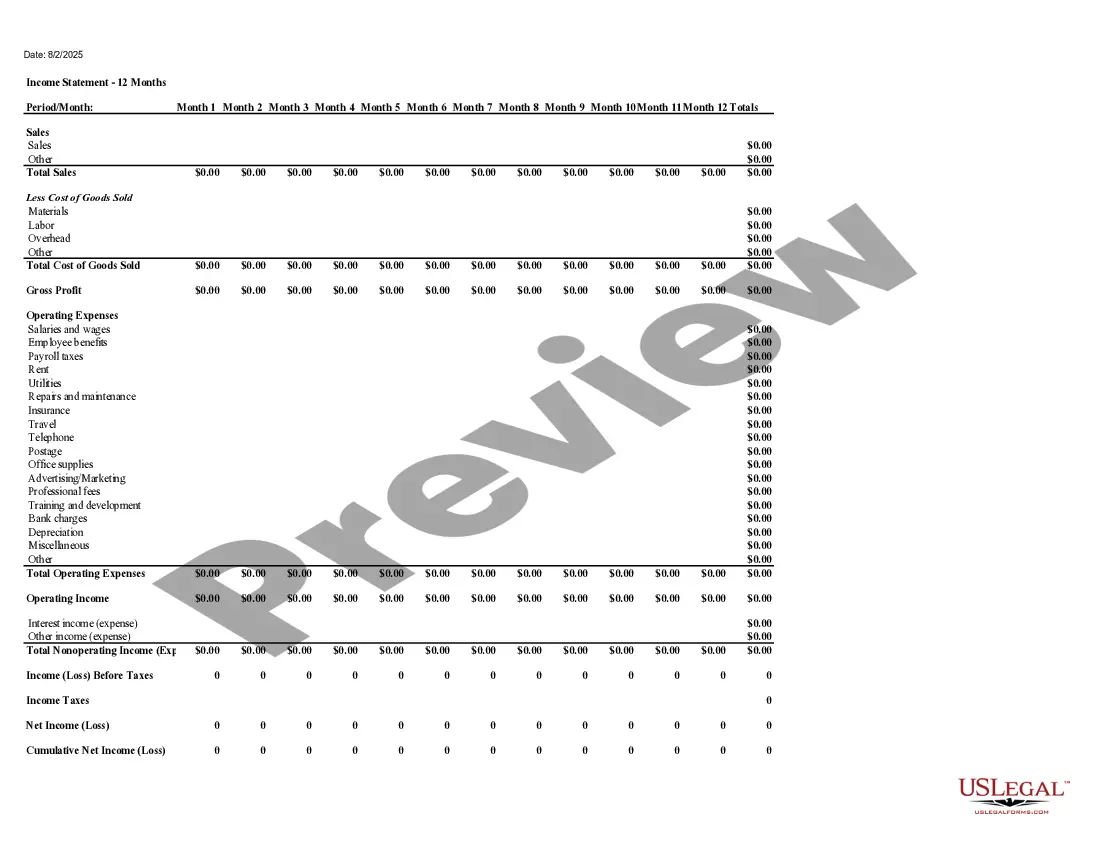

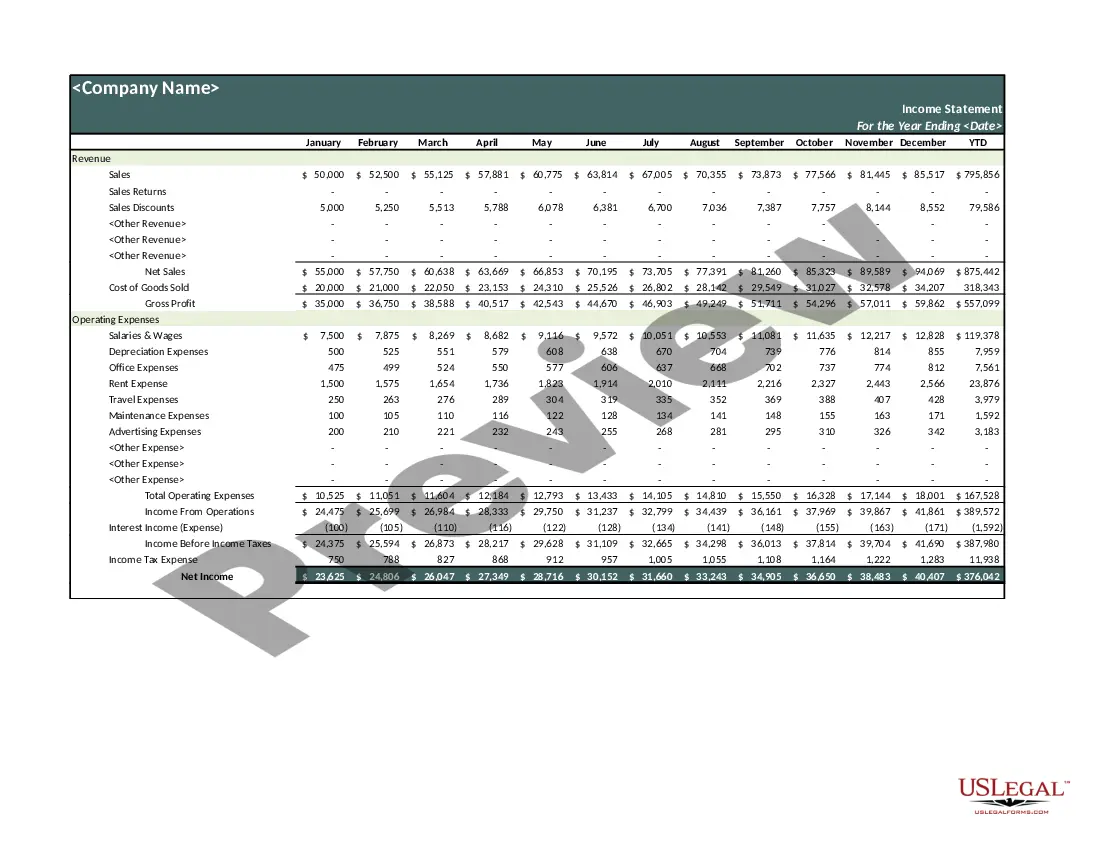

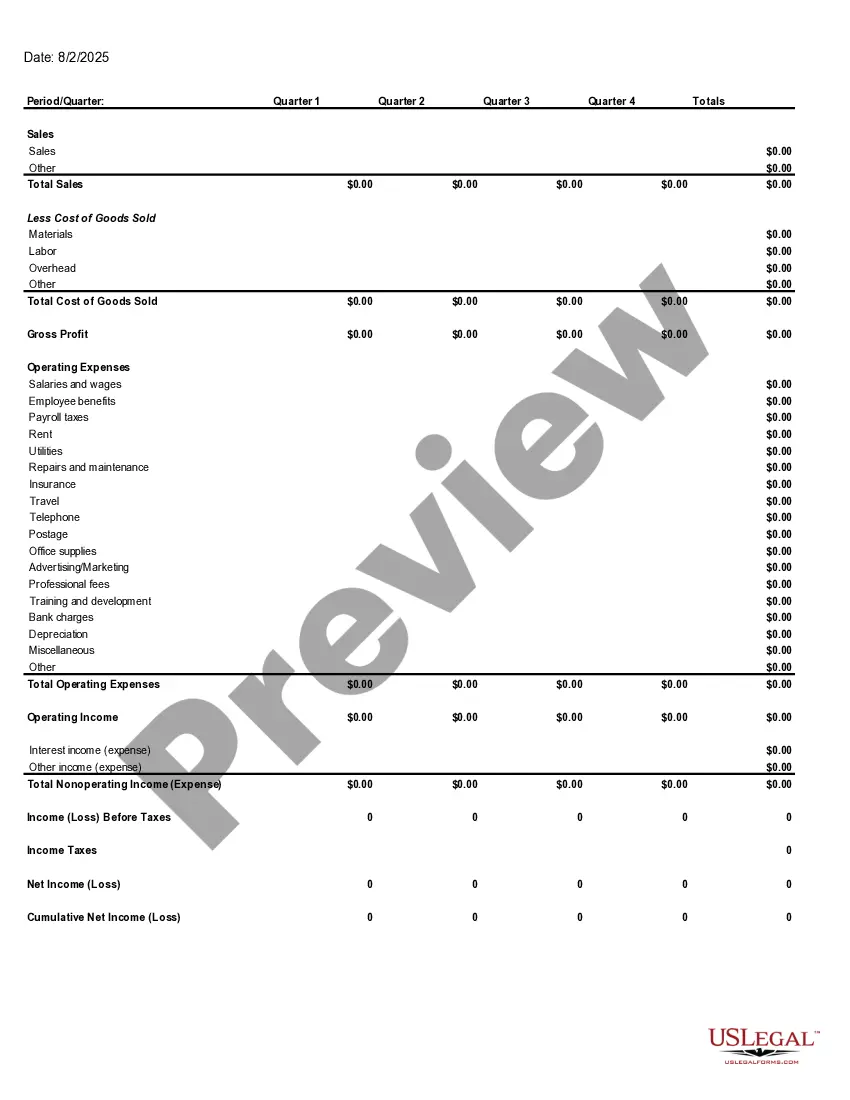

An income statement (sometimes called a profit and loss statement) lists your revenues and expenses, and tells you the profit or loss of your business for a given period of time. You can use this income statement form as a starting point to create one yourself.

Delaware Income Statement

Category:

State:

Multi-State

Control #:

US-03600BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Income Statement?

Are you in a situation where you frequently need documents for both business or personal reasons.

There are numerous legal document templates available online, but finding reliable ones is challenging.

US Legal Forms offers a vast collection of template forms, such as the Delaware Income Statement, which can be printed to satisfy state and federal requirements.

When you find the correct form, click Buy now.

Choose the payment plan you prefer, provide the necessary information to create your account, and pay for your order using PayPal or a credit card. Select a convenient document format and download your copy.

- If you are already familiar with the US Legal Forms website and possess an account, simply Log In.

- Once logged in, you can download the Delaware Income Statement template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Select the form you need and ensure it is suitable for your specific city/state.

- Use the Preview button to view the form.

- Review the description to confirm you have chosen the correct form.

- If the form does not meet your requirements, utilize the Search area to find one that suits your needs.

Form popularity

FAQ

Delaware income tax is calculated based on your taxable income after deducting the standard or itemized deductions. The rates apply progressively to different income brackets, so a higher income leads to a higher tax rate on the additional income. Having a comprehensive Delaware Income Statement will help you navigate this process efficiently and reduce any errors.

When filling out self-employment income, you need to report all earnings from your business activities on your tax return. Use Schedule C to detail your income and any expenses. It's crucial to accurately prepare your Delaware Income Statement to reflect your earnings and ensure you're compliant with Delaware tax laws.

Delaware sourced income includes all income earned within the state, such as wages from a job located in Delaware or profits from a business operating there. Even if you are not a resident, income generated in Delaware is taxable. Understanding what qualifies as sourced income is important when preparing your Delaware Income Statement.

To file a Delaware annual report, you need to complete the report form online or via mail, depending on your business type. Most businesses use the Delaware Division of Corporations' website. Remember to include any necessary financial details from your Delaware Income Statement, as this information is crucial for the report's accuracy.

Delaware state tax on a paycheck generally varies based on your earnings and withholding allowances. As an employee, you'll notice that around 6.6% may be deducted from your income. This percentage could change based on any additional local taxes or personal exemptions on your Delaware Income Statement, so keeping track of your withholdings is essential.

Calculating Delaware state income tax involves determining your taxable income and applying the appropriate tax rates. Delaware's income tax rates range from 2.2% to 6.6%, depending on your income bracket. For accuracy, using a detailed Delaware Income Statement can help you account for deductions and credits, making the calculation clearer.

For Delaware state income tax, the standard deduction is $3,250 for single filers and $6,500 for married couples filing jointly. This deduction can help reduce your taxable income, which may reflect positively on your Delaware Income Statement. It is important to consider your specific tax situation to ensure you claim the correct amount.

If you earn $100,000 in Delaware, the amount you take home after taxes depends on various factors, including your filing status and deductions. The average effective tax rate can be around 6.6% for state taxes. Thus, you might expect to see approximately $93,400 after state taxes are deducted. To get a precise figure, reviewing your Delaware Income Statement would be beneficial.

Yes, Delaware requires certain businesses to file a statement of information, which may include key financial details. This requirement helps maintain transparency and ensures that your Delaware Income Statement, along with other necessary details, is up to date. Businesses must adhere to these regulations to avoid penalties, while using resources like US Legal Forms can simplify the process of compliance and filing.

To obtain a company's income statement, you can visit the company's website and check under their investor relations section. Publicly traded companies are required to publish their financial reports, including Delaware Income Statements, regularly. Alternative options include databases like the SEC's EDGAR system or using services like US Legal Forms that can guide you in obtaining these statements with ease and efficiency.