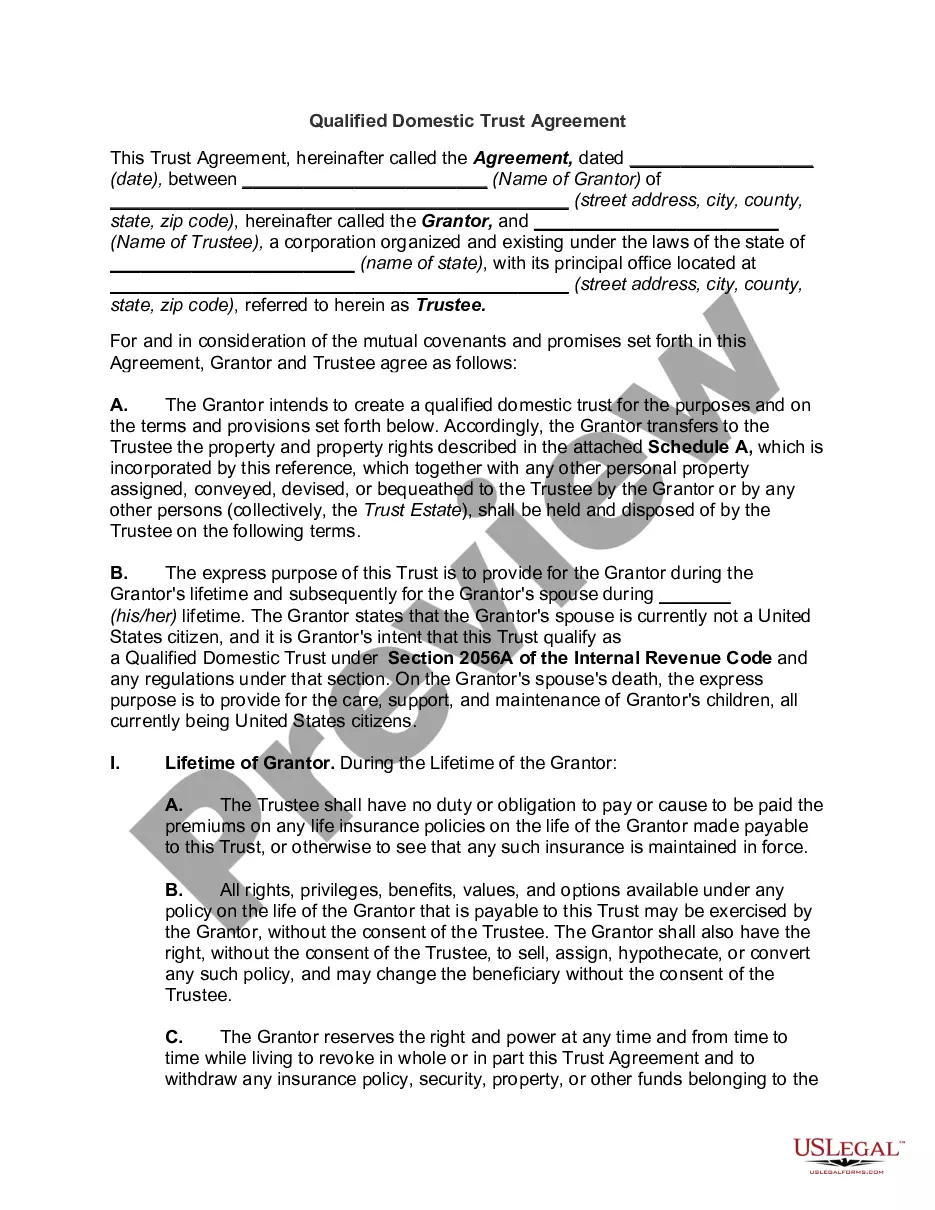

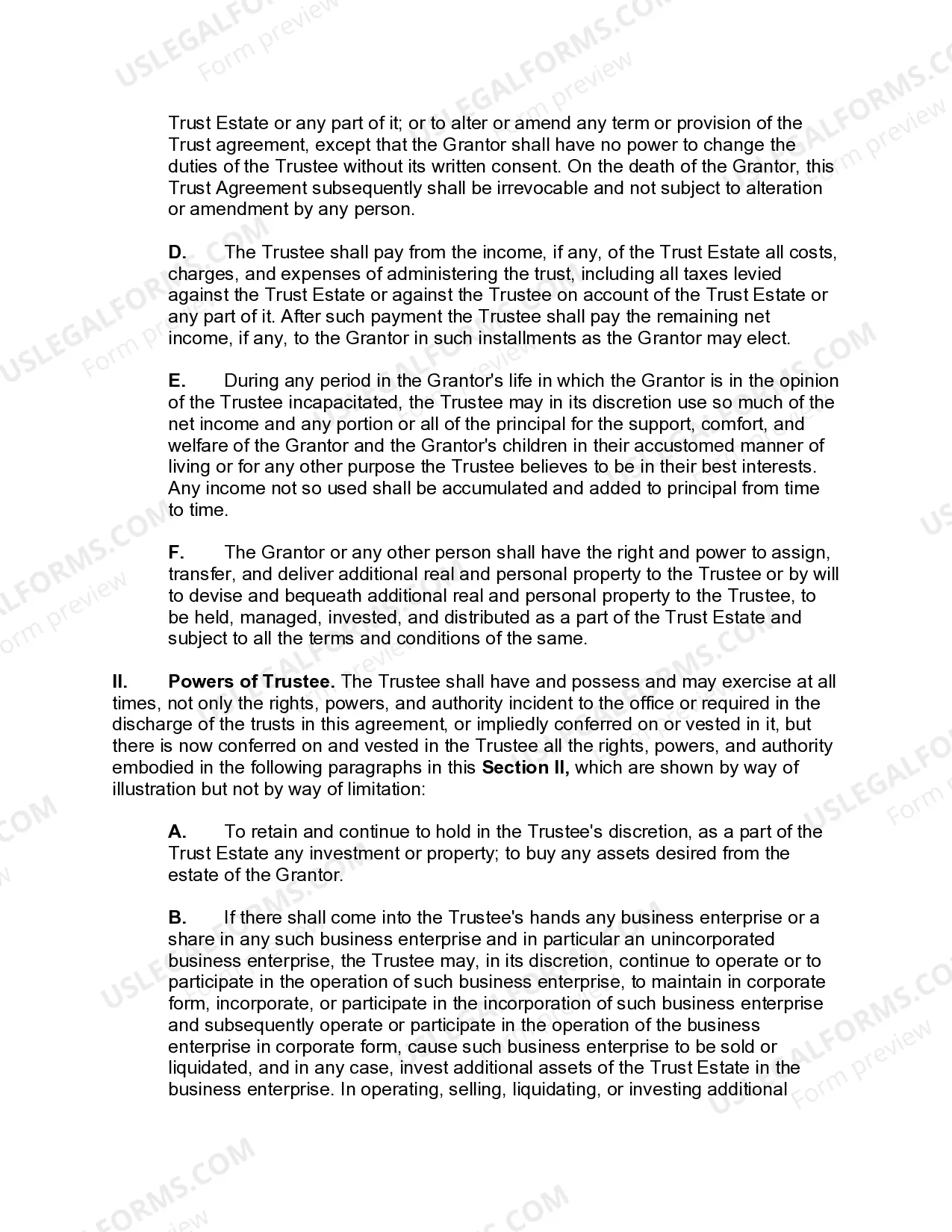

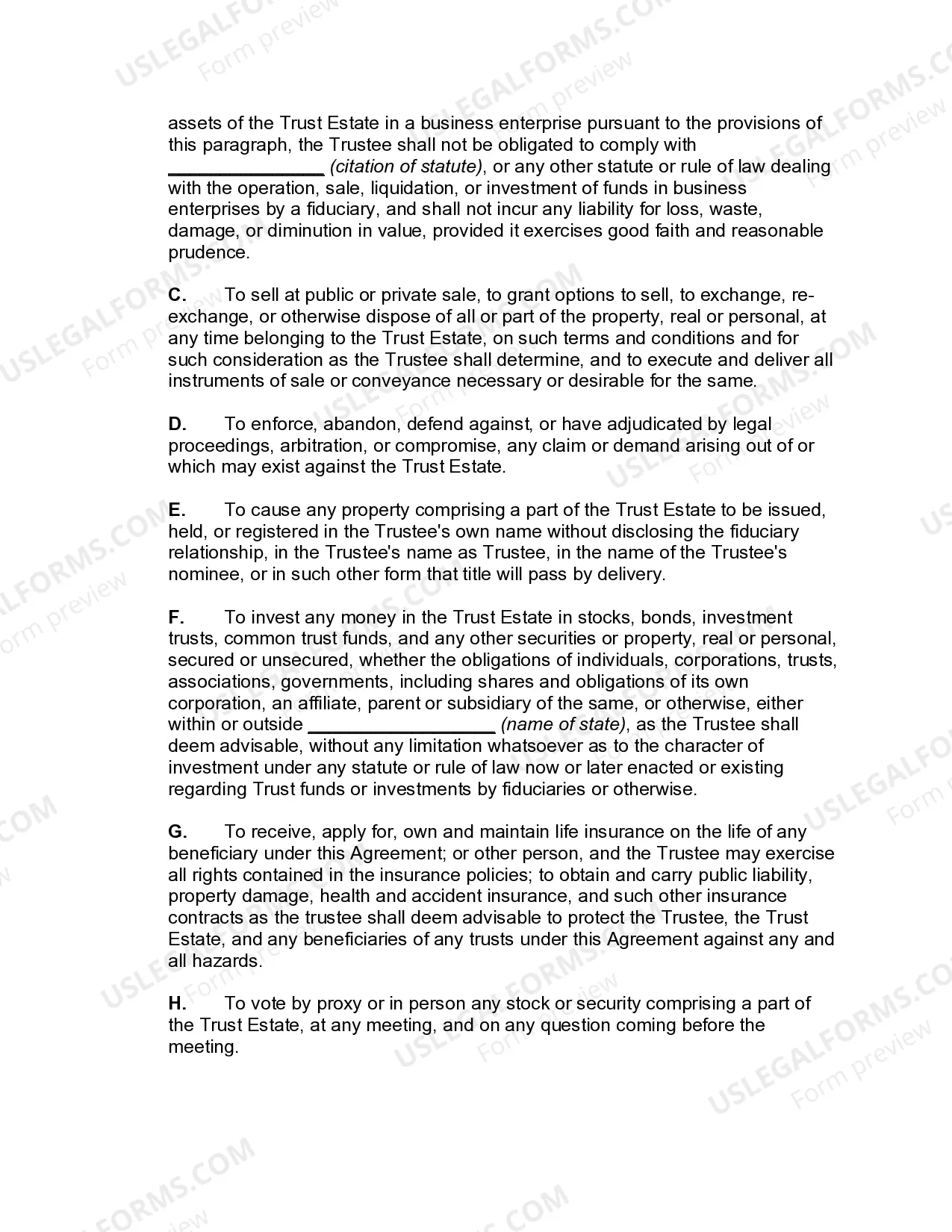

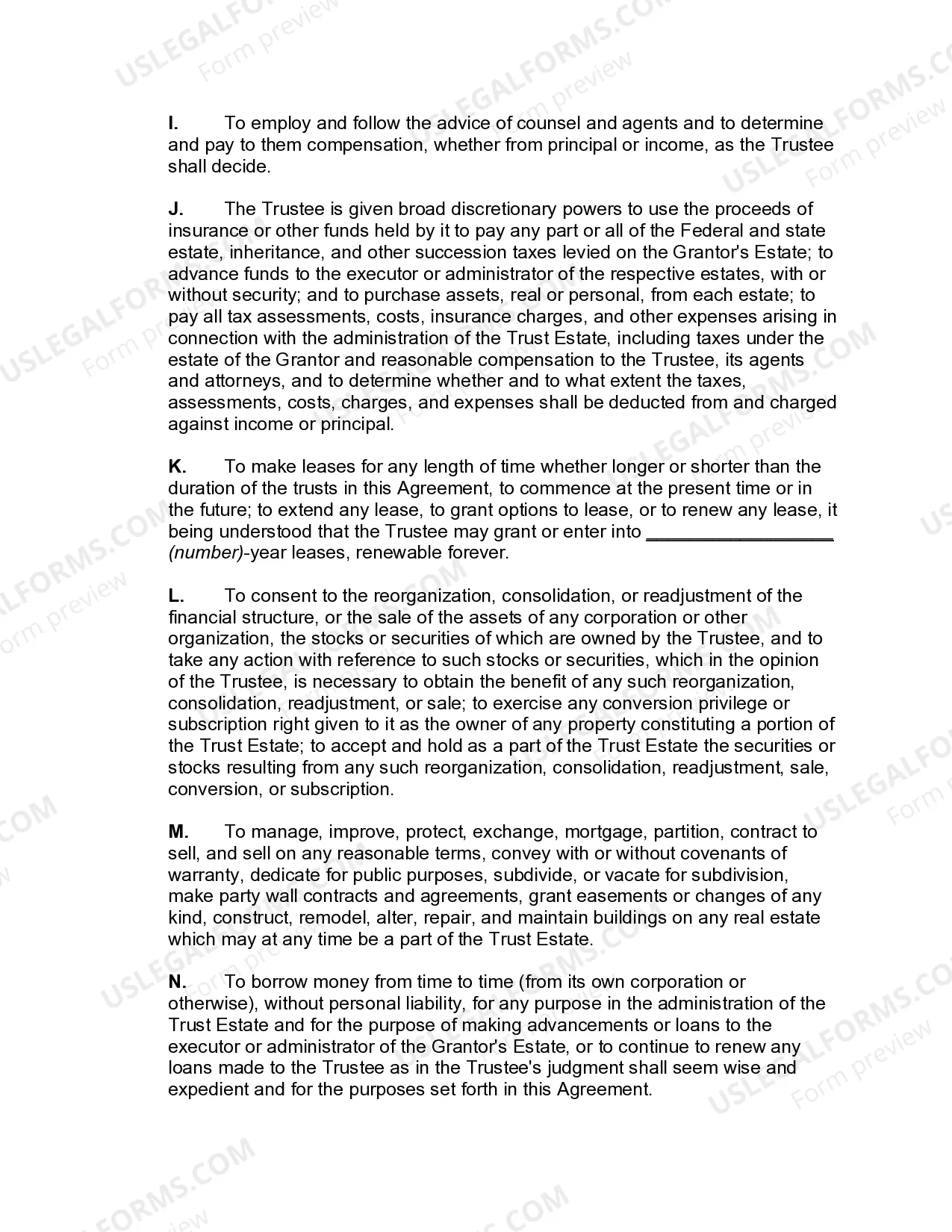

A Delaware Qualified Domestic Trust Agreement (DDT) is a legal document that allows non-U.S. citizen surviving spouses to benefit from the marital deduction for estate tax purposes. This agreement ensures that assets transferred to a trust for the benefit of the non-U.S. citizen spouse are eligible for the same estate tax treatment as a U.S. citizen spouse. A DDT is specifically designed to address the potential estate tax implications that arise when a non-U.S. citizen spouse inherits assets from a U.S. citizen spouse. Without a DDT, the unlimited marital deduction, which allows spouses to transfer assets to each other without incurring estate taxes, would not apply to non-U.S. citizen spouses. The DDT provides a mechanism to qualify the trust as a qualified domestic trust under Section 2056A of the Internal Revenue Code. This qualification ensures that the assets held in the trust, up to the estate tax exemption limit, are not subject to estate taxes upon the death of the U.S. citizen spouse. Instead, the trust is subject to estate taxes when distributions are made to the non-U.S. citizen spouse or upon the death of the non-U.S. citizen spouse. There are various types of DDT agreements available in Delaware, each tailored to meet specific needs and circumstances. Some common types of DDT agreements include: 1. General Power of Appointment Trust (GPA): This type of trust agreement allows the non-U.S. citizen spouse to have a broad "power of appointment" over the trust assets. This means that the spouse has the authority to determine how the trust assets will be distributed among beneficiaries upon their death. 2. Limited Power of Appointment Trust (PA): In an PA, the non-U.S. citizen spouse's power of appointment is restricted. They can only appoint the trust assets among a predetermined class of beneficiaries, such as their children or other family members. 3. Survivor's Trust (ST): This type of trust agreement is created upon the death of the U.S. citizen spouse and holds their share of marital assets. The non-U.S. citizen spouse is entitled to income generated by the trust during their lifetime, and the remaining assets are distributed to the designated beneficiaries upon their death. 4. Qualified Terminable Interest Property Trust (TIP): A TIP trust allows the U.S. citizen spouse to provide for their non-U.S. citizen spouse while maintaining control over the ultimate distribution of trust assets. The non-U.S. citizen spouse receives income from the trust during their lifetime, and upon their death, the remaining assets are distributed according to the U.S. citizen spouse's instructions. In conclusion, a Delaware Qualified Domestic Trust Agreement provides a tax-efficient solution for non-U.S. citizen surviving spouses to benefit from the marital deduction for estate tax purposes. Depending on the specific circumstances and desired control over asset distribution, different types of DDT agreements, such as GPA, PA, ST, and TIP, can be chosen. It is essential to consult with a qualified estate planning attorney or tax professional to determine the most suitable DDT agreement for individual needs.

Delaware Qualified Domestic Trust Agreement

Description

How to fill out Delaware Qualified Domestic Trust Agreement?

US Legal Forms - one of many greatest libraries of lawful types in America - gives a variety of lawful papers layouts it is possible to obtain or print out. While using web site, you can get a large number of types for company and individual purposes, categorized by categories, claims, or keywords and phrases.You can get the latest variations of types like the Delaware Qualified Domestic Trust Agreement in seconds.

If you currently have a membership, log in and obtain Delaware Qualified Domestic Trust Agreement from your US Legal Forms catalogue. The Obtain switch can look on each kind you see. You have access to all earlier downloaded types within the My Forms tab of your bank account.

If you wish to use US Legal Forms for the first time, listed below are easy recommendations to help you get began:

- Be sure to have picked the correct kind to your town/region. Click on the Review switch to check the form`s content. See the kind information to actually have selected the proper kind.

- In the event the kind doesn`t match your needs, utilize the Search discipline on top of the display to find the one that does.

- In case you are happy with the form, verify your option by clicking the Purchase now switch. Then, opt for the prices prepare you favor and provide your references to register to have an bank account.

- Process the transaction. Make use of charge card or PayPal bank account to complete the transaction.

- Choose the formatting and obtain the form on the gadget.

- Make changes. Fill up, change and print out and sign the downloaded Delaware Qualified Domestic Trust Agreement.

Each and every template you put into your money lacks an expiry particular date and it is your own permanently. So, if you would like obtain or print out an additional copy, just go to the My Forms section and click on on the kind you require.

Gain access to the Delaware Qualified Domestic Trust Agreement with US Legal Forms, by far the most substantial catalogue of lawful papers layouts. Use a large number of professional and status-certain layouts that meet your small business or individual requires and needs.