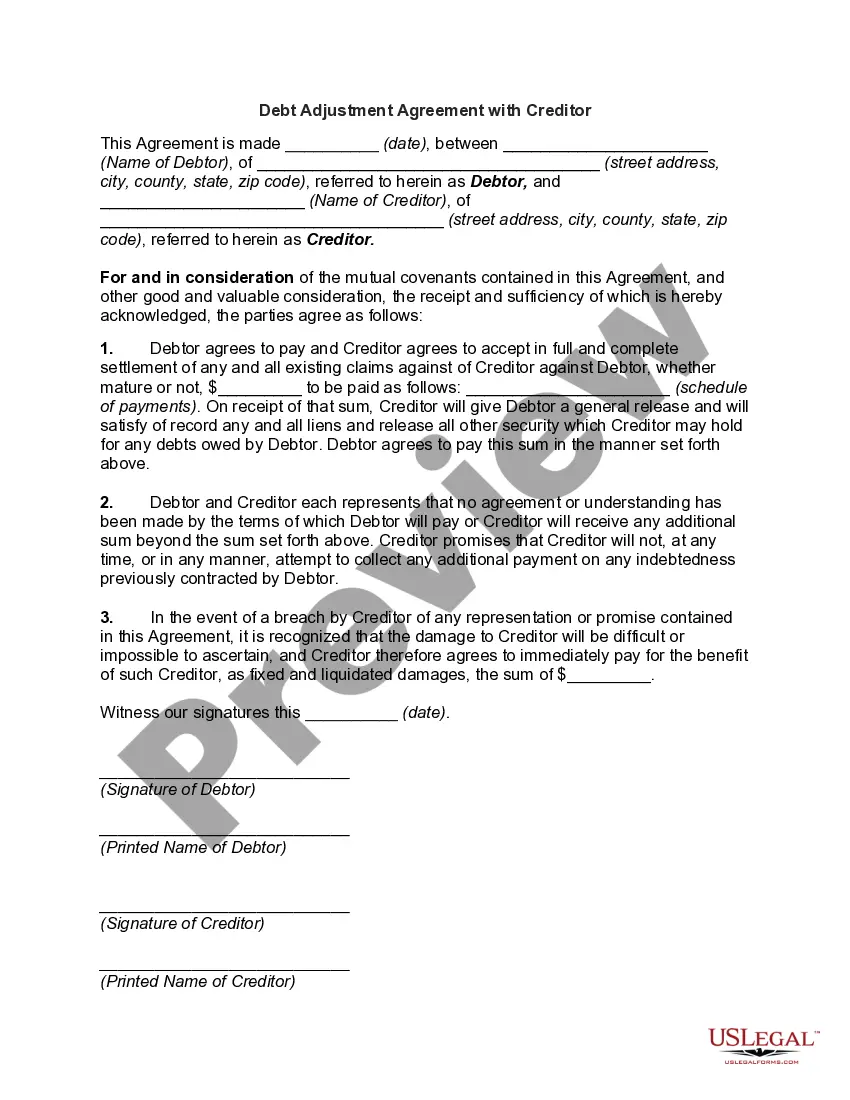

A Delaware Debt Adjustment Agreement with a Creditor is a legally binding agreement between a debtor and a creditor in the state of Delaware. This agreement aims to provide a structured repayment plan for the debtor to repay their outstanding debts over a predetermined period, typically in a more manageable and affordable manner. The primary purpose of a Delaware Debt Adjustment Agreement with a Creditor is to assist debtors who are struggling financially but have a sincere intention to repay their debts. By entering into this agreement, debtors can avoid filing for bankruptcy and maintain a certain level of control over their financial obligations. Under this agreement, the debtor and the creditor work together to establish an affordable repayment plan that takes into account the debtor's income, essential living expenses, and the total amount of outstanding debt. The debtor initiates the process by contacting the creditor or a debt management agency to express their willingness to enter into a Debt Adjustment Agreement. The creditor, in turn, conducts a thorough evaluation of the debtor's financial situation to determine the feasibility of the proposed repayment plan. Different types of Delaware Debt Adjustment Agreements may exist depending on the specific circumstances of the debtor and the creditor. These can include: 1. Unsecured Debt Adjustment Agreement: This type of agreement pertains to debts that are not backed by collateral, such as credit card debt, medical bills, personal loans, or utility bills. It establishes a structured repayment plan for the debtor to gradually repay the outstanding debt amount. 2. Secured Debt Adjustment Agreement: Contrary to unsecured debts, secured debts are backed by collateral, such as a mortgage or a car loan. This type of agreement may involve renegotiating the repayment terms, interest rates, or the amount to be paid in order to prevent the creditor from repossessing the collateral. 3. Business Debt Adjustment Agreement: Designed specifically for businesses facing financial difficulties, this agreement enables businesses to reorganize their debts and establish a repayment plan that aligns with their revenue streams. It could involve negotiating with multiple creditors and possibly reducing or extending the payment terms. 4. Student Loan Debt Adjustment Agreement: This type of agreement applies to individuals burdened with student loan debt. It may involve negotiating with the lender to establish a more manageable repayment plan, potentially adjusting the interest rate, or exploring alternative repayment options, such as income-driven repayment plans. It is important to note that the specifics of a Delaware Debt Adjustment Agreement may vary depending on the terms agreed upon by both parties. These agreements are typically overseen by debt management agencies or credit counseling services that provide guidance and support throughout the repayment process to ensure its successful completion.

Delaware Debt Adjustment Agreement with Creditor

Description

How to fill out Delaware Debt Adjustment Agreement With Creditor?

You can spend hrs on the web trying to find the lawful papers design that suits the federal and state demands you will need. US Legal Forms provides 1000s of lawful types which can be examined by professionals. It is possible to acquire or produce the Delaware Debt Adjustment Agreement with Creditor from the service.

If you already have a US Legal Forms accounts, you can log in and then click the Down load button. Afterward, you can complete, change, produce, or indicator the Delaware Debt Adjustment Agreement with Creditor. Every single lawful papers design you acquire is your own property for a long time. To have another backup for any bought type, check out the My Forms tab and then click the related button.

Should you use the US Legal Forms site the very first time, keep to the straightforward directions under:

- Initial, be sure that you have selected the proper papers design for the county/city of your choice. See the type outline to make sure you have picked out the appropriate type. If readily available, use the Preview button to look with the papers design at the same time.

- If you would like get another model in the type, use the Lookup area to get the design that meets your needs and demands.

- After you have found the design you need, click Purchase now to move forward.

- Find the prices prepare you need, type in your qualifications, and register for an account on US Legal Forms.

- Full the purchase. You can utilize your credit card or PayPal accounts to fund the lawful type.

- Find the formatting in the papers and acquire it in your device.

- Make modifications in your papers if required. You can complete, change and indicator and produce Delaware Debt Adjustment Agreement with Creditor.

Down load and produce 1000s of papers templates utilizing the US Legal Forms web site, that offers the most important variety of lawful types. Use specialist and state-specific templates to deal with your small business or personal demands.